Summary:

- Rivian Automotive’s shares have seen some gains recently, trading around 20% above recent lows, due to positive news.

- Factors contributing to the gains include declining interest rates, the underwhelming reveal of Tesla’s Cybertruck, and positive gross margin guidance from Rivian’s management.

- Despite the positive news, Rivian is still unprofitable and will generate substantial net losses next year, making it a risky investment in a competitive industry.

Justin Sullivan/Getty Images News

Article Thesis

Rivian Automotive, Inc. (NASDAQ:RIVN) is an electric vehicle pure-play that has seen its shares decline considerably from the bubbly highs seen directly following the company’s IPO. Over the last couple of days, shares saw some buying pressure as there were a couple of positive news items that we will take a look at in this article.

Rivian Automotive: Some Good News

Over the last couple of days, Rivian Automotive saw some gains, and shares are now trading around 20% above the lows seen a couple of weeks ago. This was driven by several positive news stories, among them the fact that interest rates are declining, while Tesla’s Cybertruck looks like less of a competitive threat compared to what was previously thought. Last but not least, Rivian also had an investor presentation where the company’s management made some encouraging comments about the company’s margin outlook and potential cost savings in areas such as battery technology. Let’s delve into the details.

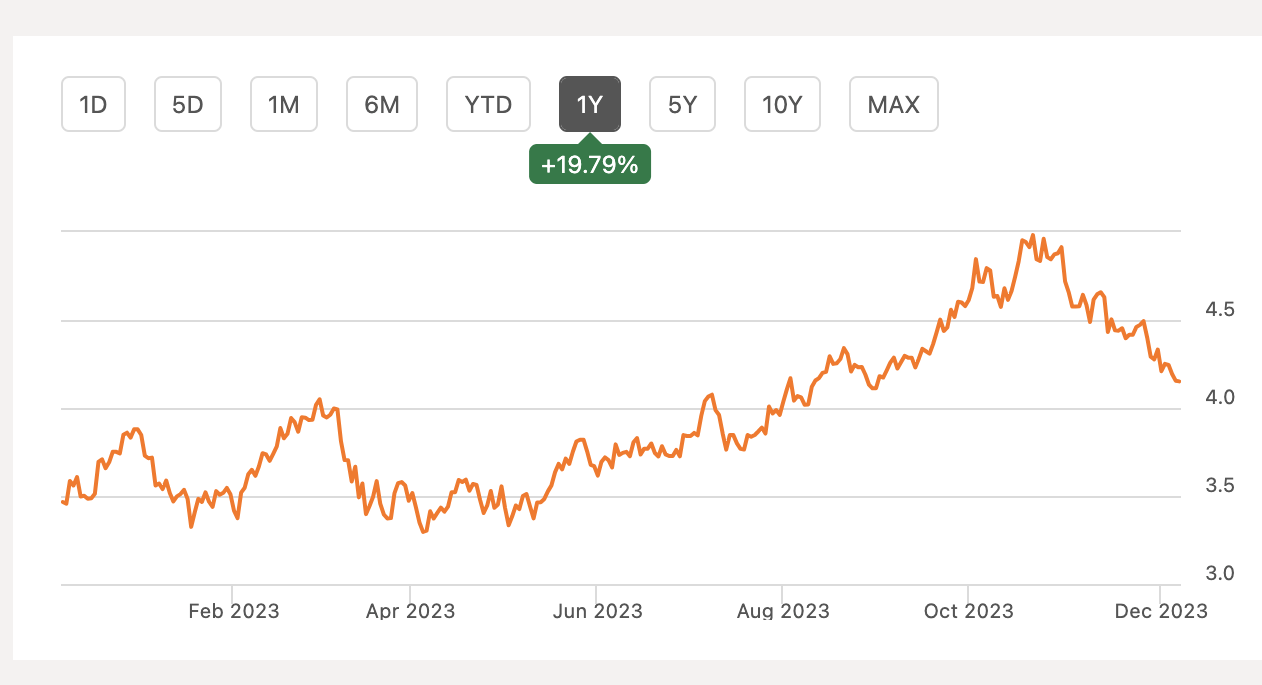

Lower interest rates

While interest rates are still up quite a bit compared to the pandemic lows, they have recently pulled back quite meaningfully from the highs seen this fall, as we can easily see in the following chart:

10-year treasury rate (Seeking Alpha)

With rates having pulled back from recent highs, there are two significant tailwinds from that for a company such as Rivian.

– The interest rate on auto loans should decline as well, all else equal, making new vehicles more achievable for the average consumer. Financing conditions still are harsher compared to the pandemic, however.

– Declining interest rates also reduce discount rates in equity valuation models such as the Discounted Cash Flow approach, all else equal. Higher-growth, higher-valuation stocks such as Rivian Automotive benefit from this effect of declining discount rates, as a large part of the company’s expected future profits are more or less in the distant future.

While declining interest rates are not a company-specific factor for Rivian, the company should benefit from this trend, along with other growth companies that are dependent on consumer spending and that could benefit from better financing conditions.

Cybertruck reveal

Tesla, Inc. (TSLA), the current EV king, has also very recently revealed the Cybertruck, delivering the first couple of vehicles and announcing pricing, range specs, and so on. Overall, the Cybertruck spec reveals and delivery ceremony was underwhelming — which is good news for competitor Rivian. If the Cybertruck was selling at a low price while offering a hefty range, that could have been a major problem for Rivian, as the company would have a very powerful competitor for its own truck in that scenario. But with the Cybertruck being rather pricey and the range not being especially strong, it does not look like the Cybertruck will be a huge threat to Rivian’s pick-up truck business. Of course, the Cybertruck will still sell reasonably well, as there are some customers who are loyal to Tesla and/or who like the truck’s design. But those who are not especially loyal to Tesla and who do not like the Cybertruck’s design particularly well will likely not be attracted by the revealed specs and pricing of the Cybertruck in a big way. Rivian, along with Ford Motor Company (F), could benefit from that as this is good news for the market potential of non-Cybertruck electric pick-ups such as the R1T and the F-150 Lightning.

Rivian’s presentation

Rivian presented at the Global Automotive and Mobility Tech Conference from Barclays PLC (BCS). There, the company’s management gave some positive notes. The company’s CFO, Claire McDonough, argued that Rivian was on track for a positive gross margin in 2024. That would be a major improvement versus the current year, during which Rivian is generating substantial losses even on a gross profit basis, i.e., before operating expenses are accounted for. Over the last four quarters, Rivian Automotive’s gross profit stood at a negative $2.4 billion, thus breaking even on a gross profit basis would be a huge step forward for the company and would get Rivian much closer to breaking even on a company-wide basis. If Rivian Automotive manages to become gross margin positive, which would go beyond breaking even on a gross margin basis, then actual results could be even better. Of course, there is no guarantee that this goal will be achieved, as Rivian has not always hit its guidance in the past. But its track record isn’t bad either, thus I believe that there is a solid chance that this goal will be achieved next year.

Gross margin improvement will be possible thanks to several contributing factors, among them declining prices for commodities such as lithium, but Rivian will also improve for scale advantages as its production and delivery numbers are rising — this results in cost savings over time, as manufacturing crews become more experienced and since purchasing conditions, etc. improve. Last but not least, Rivian also plans to reduce the costs of its batteries via a simpler and more cost-efficient battery pack structure. A simpler battery pack structure will result in lower manufacturing costs and could also result in lower costs per vehicle for items that are bought from suppliers.

It is worth noting, however, that Rivian will likely still generate a sizeable net loss next year, despite big gross margin improvements being expected. After all, operating expenses and interest expenses still make up billions of dollars per year — over the last four quarters, those two lines totaled $3.7 billion, and with the operation scaling up, Rivian’s operating expenses might be higher next year, compared to the current year. Thus, if Rivian were to generate a positive gross profit of $1 billion next year, the company’s net loss could still total $3 billion or so. So while things are improving and moving in the right direction, Rivian is by far not profitable, and it is very likely that the company will burn billions of cash next year. This, in turn, means that the company could be forced to take on more debt or issue more equity in the future — not necessarily in 2024, but even that can’t be ruled out.

Is Rivian A Buy?

Rivian’s shares have been punished greatly during the last year, and even more so compared to the highs seen directly after the company’s IPO. But very recently, shares saw some gains, and that can be explained by several positive news items, including declining interest rates, a not-very-overwhelming Cybertruck reveal, and the fact that Rivian gave some positive gross margin guidance.

But even despite this positive news, Rivian will generate substantial net losses next year, while the company will also continue to burn cash at a hefty pace. The electric vehicle industry remains highly competitive, and the ongoing price war is hurting the profitability outlook across the entire industry.

With Rivian not being profitable yet while the company is active in a cyclical and competitive industry, I do not see Rivian as a low-risk stock. Things are progressing reasonably well, but the company is still an unprofitable player, and that should not be forgotten by investors.

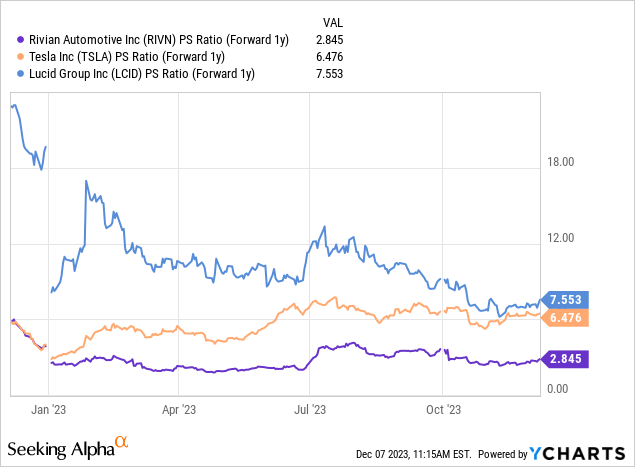

Rivian is currently trading at a valuation that is lower compared to its peers:

At around 3x forward (2024) sales, Rivian trades at less than half the valuation of peers Lucid Group, Inc. (LCID) and Tesla trade. Rivian looks better than Lucid for sure, based on its valuation and growth trajectory, but the comparison to Tesla is difficult, as Tesla is profitable, unlike Rivian, which warrants a valuation premium.

One can make a case for Rivian being the better investment among these two, but one can also decide that neither is especially attractive today, especially with macroeconomic uncertainties around a potential recession, which would likely hurt all automobile companies.

Rivian does not look bad, but it does not look attractive enough for me to buy shares at current prices. For someone looking for EV exposure who is not concerned by the lack of profits, Rivian could be a reasonable investment, however.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Is This an Income Stream Which Induces Fear?

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% – 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio’s price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% – 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio’s price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!