Summary:

- Super Micro Computer faces compliance risks and potential Nasdaq delisting due to delayed financial reports; an independent review found no compliance risks related to the Ernst & Young letter.

- SMCI has multiple catalysts that can improve the stock price, including the release of its FY24 10-K, Q1’25 10-Q, and sales of its Blackwell rack system.

- The Company may be overbuilding with its Silicon Valley expansion and new Malaysia facility, given the current utilization rate of 50%. This could potentially create a margin headwind.

Vertigo3d/E+ via Getty Images

Super Micro Computer (NASDAQ:SMCI) continues to undergo significant risks associated with its financial reporting as the firm navigates its resolution of compliance concerns. Since reporting Q1’25 estimated results, SMCI has brought in BDO as its new auditor to review and sign off on the firm’s FY24 10-K and Q1’25 10-Q once financials are approved. As a result of the delayed release of its 10-K, SMCI has fallen out of compliance with Nasdaq’s listing requirements.

There is a silver lining in the matter as the Special Committee reported on December 2, 2024, that no restatements will be required based on its findings. Given the current risk profile of SMCI, I am upgrading my rating to a Buy with a price target of $50.32/share at 1.26x eFY26 price/sales.

Super Micro Computer Audit Update

SMCI’s woes continued through Q1’25 and into Q2’25 as the firm has yet to report its FY24 10-K and its Q1’25 10-Q. Since reporting its Q1’25 earnings call, SMCI issued a late notice for the quarter’s 10-Q as it has awaited its third-party financial audit. Just to recap, Ernst & Young resigned mid-audit of Super Micro’s FY24 results after voicing in July 2024 concerns relating to SMCI’s internal controls regarding financial reporting. This led EY to question SMCI’s integrity and ethical values, as well as its transparency and oversight.

We are resigning due to information that has recently come to our attention which has led us to no longer be able to rely on management’s and the Audit Committee’s representations and to be unwilling to be associated with the financial statements prepared by management, and after concluding we can no longer provide the Audit Services in accordance with applicable law or professional obligations.

The Special Committee reported on December 2, 2024, that there was no misconduct as it relates to Ernst & Young’s concern.

On November 5, 2024, as part of SMCI’s Q1’25 press release, management disclosed that the Board of Directors had formed an independent committee [Special Committee] to investigate the concerns raised by EY. Management released a statement that the Special Committee found that the Audit Committee has acted independently and that there is no evidence of fraud or misconduct. As part of the Special Committee’s report, SMCI was recommended to appoint a new CFO, Chief Compliance Officer, and general counsel

Accordingly, management noted in the press release that they cannot provide a date for the release of the company’s FY24 10-K. SMCI has also issued a compliance plan to The Nasdaq Stock Market to request an extension of its 10-K filing. On November 20, 2024, Nasdaq sent SMCI a letter of notification, making me believe that SMCI may face the possibility of delisting.

Consistent with prior announcements, and in accordance with Nasdaq marketplace rules, the Company today announced that the Company received a notification letter from Nasdaq (the “Letter”) stating that the Company is not in compliance with Nasdaq listing rule 5250(c)(1), which requires timely filing of reports with the U.S. Securities and Exchange Commission.”

On November 1, 2024, SMCI issued a press release on the SEC website stating that its loan agreement with Cathay Bank was amended to extend the date for the release of its FY24 10-K to December 31, 2024, in order to remain in compliance as well as to add a covenant that SMCI must maintain at least $150mm in unrestricted cash on the balance sheet at all times.

Given that the Special Committee found no misconduct, I believe that SMCI can fall back into compliance with its financing covenants and Nasdaq. This was clearly a major catalyst for SMCI as shares rose as high as 31% intraday on December 2, 2024.

Super Micro Computer Operations

SMCI began building full-scale liquid-cooled data centers as part of its Rack Scale Plug And Play Solutions, allowing customers to purchase the entire AI server stack for deployment. I believe that this feature will realize exceptional growth as more enterprises build out their internal AI factories as part of their AI initiatives. Accordingly, the Datacenter Building Blocks Solution can significantly reduce new buildouts from 2 years to a few quarters. Management anticipates that 15-30% of new data centers will leverage DLC infrastructure over the next 12 months. This can be seen with Digital Realty (DLR) as the data center REIT will be offering DLC at some of its facilities.

As part of this, SMCI released its Super Cloud Composer [SCC] for infrastructure orchestration at the data center level. This software will allow enterprises to simplify and automate IT administration tasks in order to improve data center operational efficiencies and potentially manage costs down.

As of Q1’25, SMCI is in the process of completing its new Malaysia campus, with the expectation of commencing operations in eQ2’25. SMCI continues to expand its Silicon Valley facilities to increase DLC rack-scale production capacity. As of Q1’25, these facilities have 15MW of power and are capable of producing over 1,500 DLC GPU racks per month. According to comments in the Q1’25 earnings call, SMCI shipped fewer DLC racks in Q1’25 when compared to Q4’24. Though the underlying rationale isn’t certain, there were hints that this was the result of both customers awaiting the release of Blackwell GPUs and SMCI’s delayed 10-K release.

As part of this, SMCI grew inventory levels to 85 days on hand in Q1’25, up from 83 days in Q4’24. Management noted that the firm’s utilization rate was also significantly down from previous quarters at around 50%.

Accordingly, SMCI has its Nvidia GB200 NVL72 rack ready for production with its 10U air-cooled and 4U liquid-cooled B200 rack system. One factor worth mentioning is that the DLC solution will be a hybrid solution with cooling fans as part of the system. For comparison purposes, Hewlett Packard Enterprise (HPE) announced at its AI Day that the firm will be releasing a pure direct liquid cooling rack that will not require any cooling fans, potentially improving power efficiency in the server rack. In addition to this, Dell Technologies (DELL) announced that the firm will be releasing the first enterprise-ready GB200 NVL72 rack in its recent Q3’25 earnings calls. This factor suggests that Dell may have the edge relating to the imminent ramp-up of GB200 GPUs.

In addition to the Nvidia (NVDA) Blackwell solutions, SMCI is offering Advanced Micro Devices (AMD) MI300 & MI325 platforms and Intel (INTC) Gaudi 3 solutions. Accordingly, AMD and Intel’s solutions are anticipated to primarily be utilized for AI inferencing as opposed to AI training.

Super Micro Computer Financial Position

Corporate Reports

Do note that the Q1’25 financial figures in my chart are estimates based on management’s statements and may not align with the firm’s actual reporting. These figures will be updated in a later report. Note that FY24 EPS is calculated pre-stock split and does not reflect the current shares outstanding.

Management reported that Q1’25 revenue is expected to come in at $5.9-6b, with a gross margin of 13.3%. Adjusted diluted EPS for Q1’25 is expected to come in close to the guidance midpoint at $0.75-0.76/share. This compares to their guidance range of $6-7b in revenue and $0.67-0.83/share for adjusted EPS.

Management noted that many of the headwinds experienced in Q1’25 were the result of customers holding off on purchases as they await Blackwell GPUs. It was also suggested that SMCI’s delayed 10-K may have some implications for customer sales.

Management reported that days inventory grew from 82 days to 85 days sequentially in Q1’25. I suspect the inventory build was the result of SMCI building out its GB200 server racks in anticipation of the release of the GPUs.

Looking ahead to eQ2’25, I’m forecasting revenue to come in at $5.57b, with an adjusted EPS of $0.63/share. My eFY25 forecast for SMCI is below consensus estimates of $24.98b at $23b. My rationale behind this is that the competing infrastructure integrators HPE and Dell are both expecting AI infrastructure to continue to grow at a slower pace. My forecast also takes into consideration SMCI estimating financials at the lower end of the previous guidance, potentially hinting at moderating growth. SMCI’s utilization rate may also indicate the possibility of slowing demand, especially when considering that the firm is expanding its Silicon Valley facilities and completing its Malaysia facility.

Risks Related To Super Micro Computer

Bull Case

SMCI remains well-positioned to cater to the growing demand for DLC server stacks with the release of Nvidia Grace Blackwell architecture in the coming months. The firm is also expanding its manufacturing footprint, allowing for higher capacity growth, in order to service the growing need for AI computing.

Given that the Special Committee found no misconduct as it relates to EY’s concerns, I believe the official release of the firm’s FY24 10-K and Q1’25 10-Q will be positive catalysts for the stock.

Bear Case

SMCI is finding itself in a challenging position with its delayed SEC reports, potentially placing its credit facilities at risk of falling out of compliance. The firm is also facing the risk of being delisted from the Nasdaq as a result of this, potentially providing for a less stable share price in the coming quarters.

From an operational perspective, SMCI’s utilization rate was suggested to be around 50% as it expands its Silicon Valley facilities and nears completion of its Malaysia facility. This may put the firm at risk of overbuilding capacity if the sales cadence doesn’t materialize as management anticipates, resulting in higher operating costs on the back of lower revenue generation.

Valuation & Shareholder Value

Corporate Reports

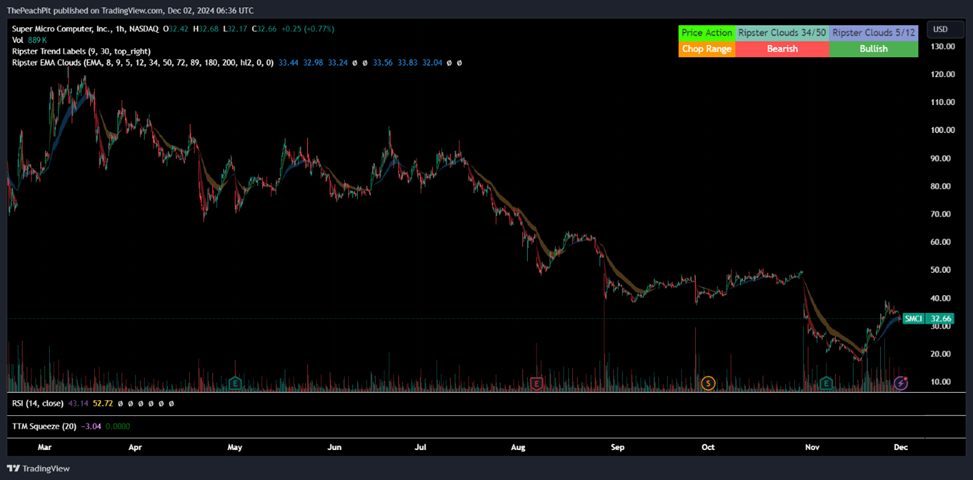

SMCI shares have been in near free-fall since the firm first delayed the release of its FY24 10-K following the Hindenburg Research short report, declining by -72%.

TradingView

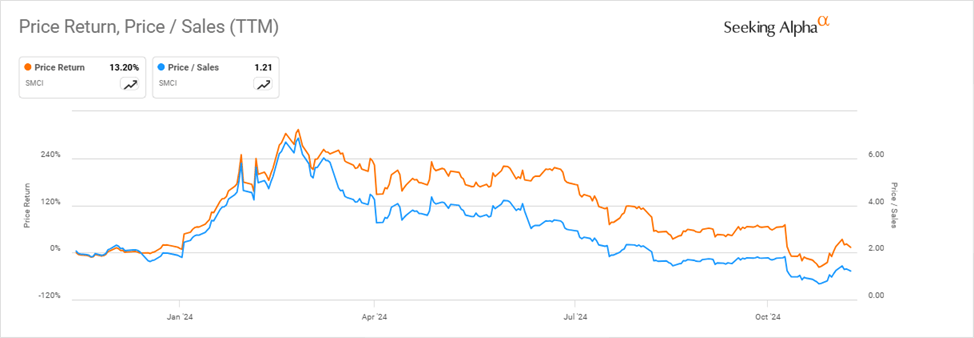

From a valuation perspective, this may make SMCI shares appear appealing given the high premium shares were trading at earlier this year in March. This decline in share price drove the valuation from ~6.85x price/sales down to 0.67x in mid-November.

Seeking Alpha

Looking at peer comps, SMCI trades at a significant discount at 1.45x price/sales, well below its peer average of 1.94x. Given this factor, I believe SMCI shares hold some upside potential as a result of the huge price run.

Seeking Alpha

Valuing SMCI using an internal model based on my eFY26 net sales forecast and the stock’s historical trading premiums, I believe shares may be pushed up as high as $50.32/share at 1.26x price/sales. I am upgrading my rating to a Buy.

Corporate Reports

The catalysts that will drive shares up include the release of the FY24 10-K and Q1’25 10-Q as well as improved growth as a result of shipments of GB200 server racks in e2h25. The first factor will bring confidence back to shareholders, and the second factor will solidify SMCI’s position in the market.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top 2025 Long/Short Idea investment competition, which runs through December 21. With cash prizes, this competition — open to all analysts — is one you don’t want to miss. If you are interested in becoming an analyst and taking part in the competition, click here to find out more and submit your article today!

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AMD, HPE, DELL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.