Summary:

- Legalization of cannabis in the US has been pushed back, indefinitely.

- Tilray’s revenues were down 7% y/y. Not the worst result. But this figure includes acquisitions.

- Tilray makes the bulk of its cash by diluting shareholders.

- This is a risky stock. So investors passionate to invest in this name should appropriately size this stock in their portfolio.

ArtistGNDphotography

Investment Thesis

Tilray’s (NASDAQ:TLRY) prospects have receded as cannabis legalization in the US has faded.

Consequently, what’s left at play is a company that is rapidly attempting to diversify away from cannabis and putting on itself a label of lifestyle consumer packaged goods.

Meanwhile, revenues are negative, and the company gets the bulk of its cash from diluting shareholders. That’s the core of what’s at play.

Legalization? Not on the Cards, For Now

Late last year, the cannabis sector got a boost as President Joe Biden sought to legalize cannabis. This saw the sector get a boost. However, that positive dynamic has now faded away and investors have moved on to other areas of the market.

Along these lines, management’s quote from its earnings call yesterday succinctly surmises the dynamic at play,

[…] during the quarter, we opt[ed] to build cash by temporarily slowing down production in our cannabis facilities because of the longer-than-anticipated march toward legalization in key markets.

This included cutting headcount and reducing other operational costs.

Tilray is having to move its business beyond the hope of the US legalizing cannabis.

TLRY Q2 2023 Results

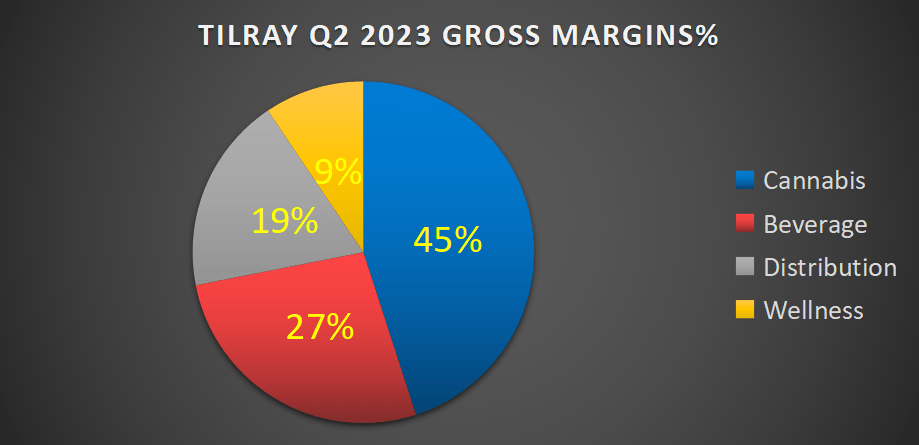

Before getting stuck into Tilray’s prospects, I believe that the graphic that follows sheds light on the company’s prospects.

TLRY Q2 2023 adjusted gross margins

As you can see above, despite Tilray being recognized as a cannabis stock, less than half of its gross margins come from cannabis.

Tilray describes itself as a diversified cannabis lifestyle consumer packaged goods. And this is my point, this is a business with a narrative focused on cannabis, but under the hood, there’s quite a different business.

Next, compounding matters, despite including revenues from recent acquisitions, Tilray’s Q2 2023 revenues were down 7% y/y.

Put another way, this isn’t a smoking-hot business. But a wilting business.

More Equity Raises Coming?

Tilray holds a net cash and equivalents position of approximately $250 million. This is up from approximately $220 million six months earlier. A portion of the increase in cash on Tilray’s balance sheet came from Tilray’s $25 million of free cash flow.

That being said, recall that back in Q1 2023 Tilray raised $130 million worth of cash by diluting investors in that quarter.

Hence, this means that Tilray’s total number of shares is up 33% y/y to approximately 612 million, versus 460 million in the same period a year ago.

Accordingly, while Tilray’s substantial improvement in free cash flow should be applauded, keep in mind that this figure remains a small sum compared with the cash raised from diluting shareholders.

On the other hand, note that on top of its debt, Tilray also has a large amount of convertible notes due in 2024.

TLRY 10-K

More specifically, Tilray has just over $200 million worth of convertibles due in 2024. In practical terms, given that Tilray is unlikely to make $200 million of free cash flow between now and maturity, I suspect that investors should brace themselves for more equity raises.

And this leads me to the crucial point, a discussion of Tilray’s valuation.

TLRY Stock Valuation — Very Difficult to Ascertain Fair Value

In the past few weeks, we’ve seen investors’ interest in Tilray dramatically sell-off.

Consequently, unless in some way investors’ appetite towards the cannabis sector was to dramatically improve and do so quickly when Tilray next raises funds from shareholders it could be in a position to dilute investors by a further 15% to 20%.

The Bottom Line

In sum, Tilray is incredibly risky. And backed by a frail balance sheet. Further, Tilray’s ability to grow its revenues, despite acquiring new businesses is struggling.

This is little more than a story stock. Investors seeking a “speculation” may do well to consider this name. But investors should keep in mind that this is a speculative position, and should appropriately size Tilray in their portfolio.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities – stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

-

- Deep Value Returns’ Marketplace continues to rapidly grow.

- Check out members’ reviews.

- High-quality, actionable insightful stock picks.

- The place where value is everything.