Summary:

- Transocean is benefiting from a record contract backlog, supporting a strong growth outlook.

- An expectation for climbing earnings and ongoing balance sheet deleveraging are key fundamental tailwinds for the stock.

- We expect shares to rally higher alongside a rebound in the broader energy sector through 2024.

pabst_ell

Transocean Ltd. (NYSE:RIG) is set to finish 2023 with an impressive gain, returning nearly 50%. Despite volatile conditions in the energy market, the understanding is that this segment of offshore drilling services remains in a “multi-year upcycle” as exploration and production giants add spending to replace hydrocarbon reserves.

The company is benefiting from a fleet transformation by focusing on its strengths in ultra-deepwater and “harsh environment” offshore drilling floaters. In many ways, the current trends reflect a decade-long restructuring to move past financial difficulties with a strong foundation for a positive long-term outlook.

We expect 2024 to be an important year for Transocean to gain operating and earnings momentum. We highlight 5 reasons to be bullish on RIG with room for shares to rally higher.

1) Strong Operating Outlook

RIG last reported its Q3 results in October with a negative EPS of -$0.32, and revenue of $713 million both missing expectations. The context here considers the timing of some major contracts and mobilization for pending deployments.

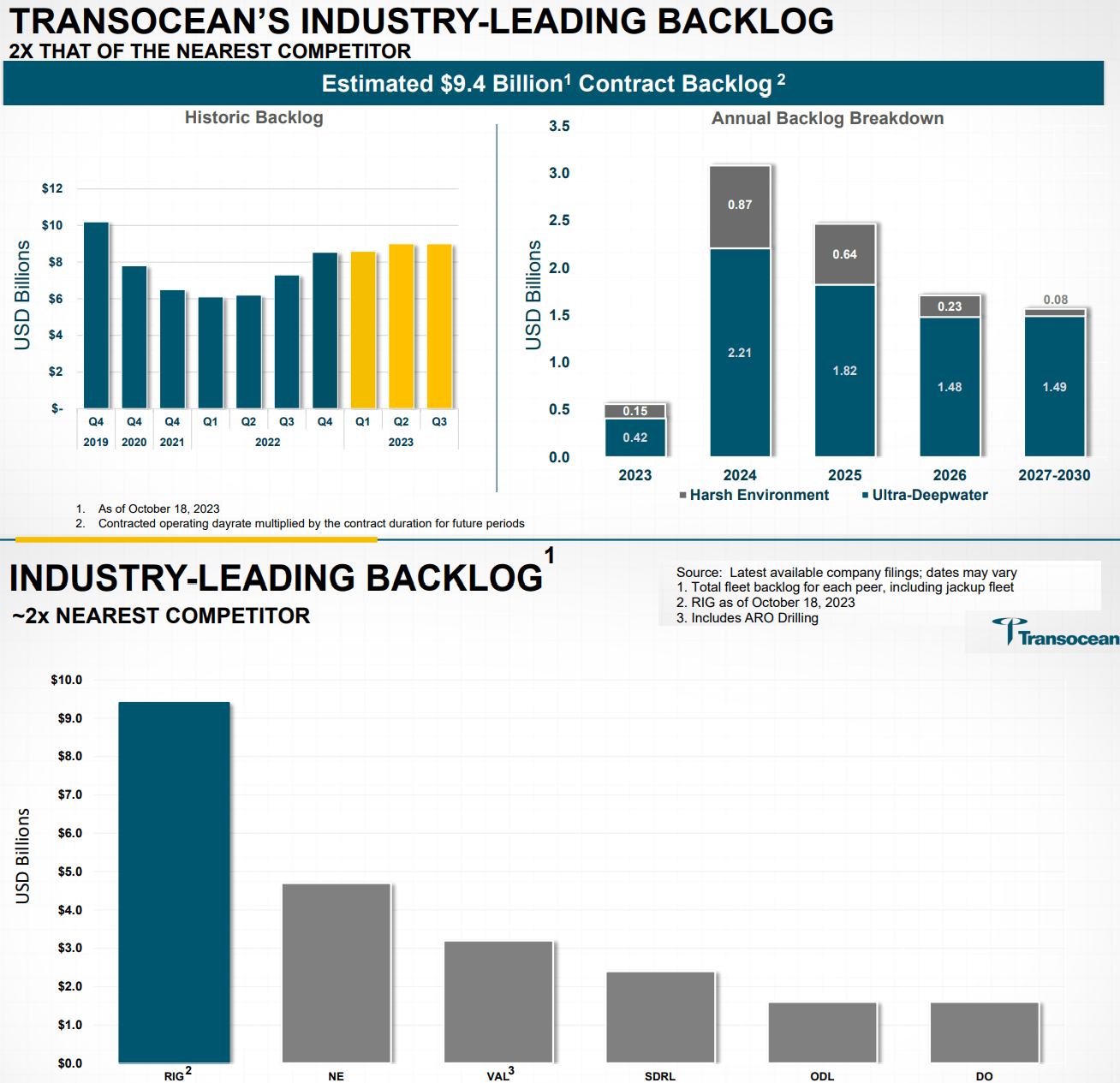

That being said, the big story was the ongoing increase in the operational backlog, ending the quarter at $9.4 billion. This was a major theme during the earnings conference call with management noting the company’s backlog is the largest in the industry and nearly 2x its nearest competitor.

Some of the recent customer wins include a three-year $486 million contract for “Deepwater Aquila” for operations offshore in Brazil. 2024 is set to drive a new wave of growth as both supportive to stronger financial performance and a rebound in earnings.

source: company IR

2) Free Cash Flow Supports Ongoing Deleveraging

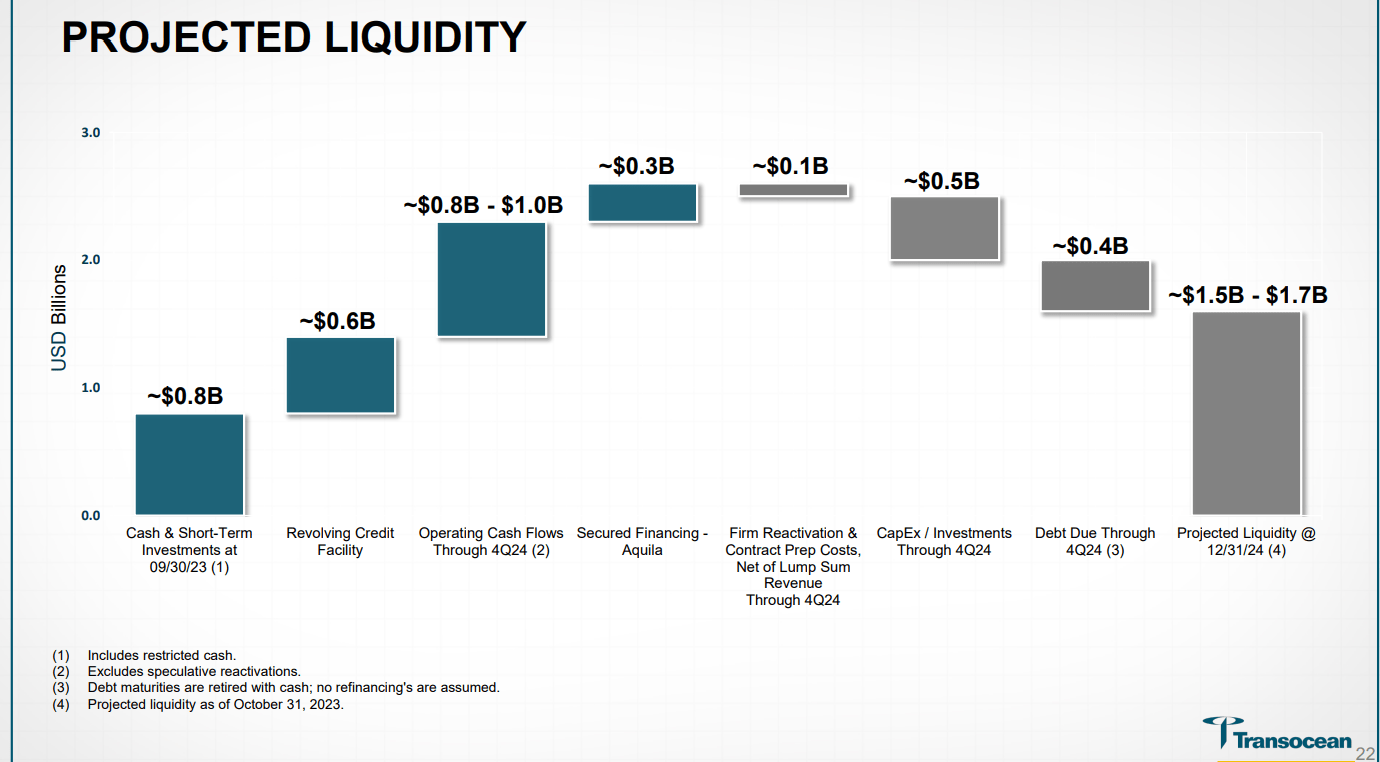

A priority for Transocean is deleveraging its balance sheet. Several steps have been taken to improve the liquidity profile, including an extension of credit facilities and moving forward with secured financing.

Following the recent delivery of several 7th and 8th-generation drillships, the expectation is for moderating capex needs while operating cash flows improve. From approximately $800 million in cash and cash equivalents at the end of last quarter, Transocean sees projected liquidity approaching $1.7 billion by the end of next year.

In our view, this forecast of a stronger balance sheet should ultimately translate into a higher equity value for shareholders as a tailwind for the stock.

source: Company IR

3) Profitability Expected To Ramp Up

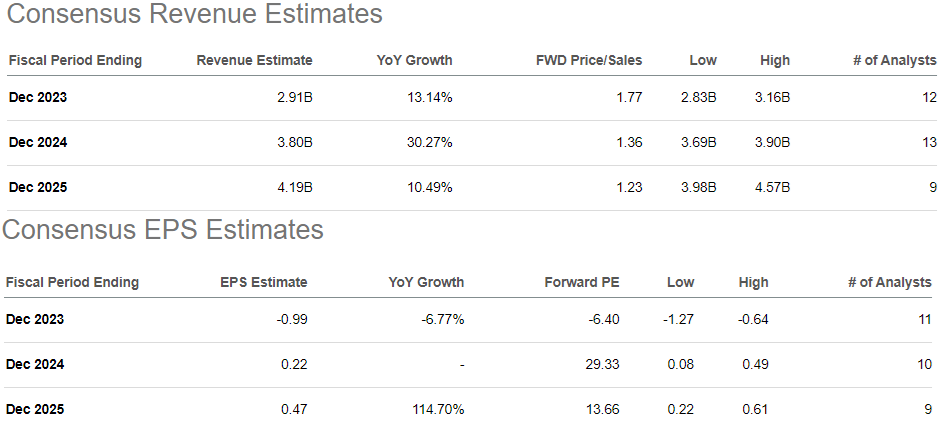

The market consensus is that from a forecasted negative EPS of -$0.99 this year, Transocean should turn profitable in 2024. Revenue growth should also accelerate based on the backlog visibility.

Seeking Alpha

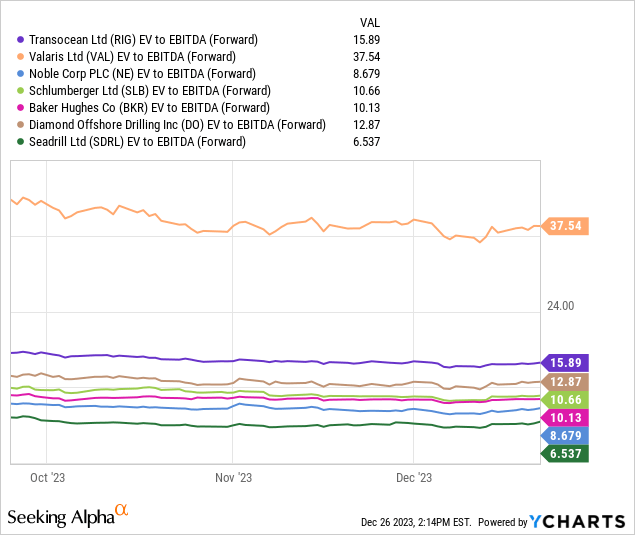

As it relates to valuation, RIG trading at a 16x EV to forward EBITDA multiples stands out at a premium to its peer group. Among major oil services and offshore drilling platform providers, names like Noble Corporation Plc (NE), Baker Hughes Co (BKR), and Diamond Offshore Drilling, Inc. (DO) trade with an average multiple closer to 10x.

That being said, it’s understood that RIG’s fleet transformation and strengthening balance sheet translate into stronger earnings growth going forward into next year. The consensus for 30% revenue growth in 2024 with EPS turning positive and even doubling again by fiscal 2025 suggests there is room to grow into its valuation spread. By this measure, we believe the current valuation is attractive considering the outlook relative to the industry.

4) Upside To Energy Prices

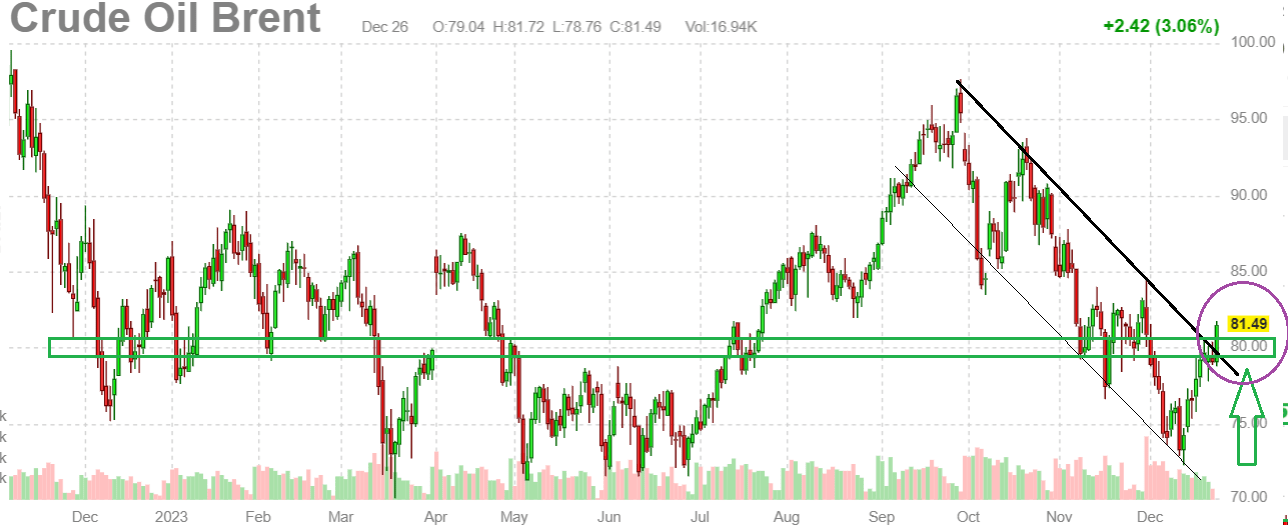

Despite a relatively wide trading range in oil prices this year, Brent crude oil is on track to end down just a few points from 2022. The story is the combination of factors with several moving parts pulling the market in multiple directions.

The story since late Q3 has data suggesting stronger global production and rising inventory levels against uncertainties over global growth. The Israel-Hamas war introduced a bullish element to the mix with some fears of Middle East supply chain disruptions.

In our view, oil should remain supported considering the outlook for a stronger macro backdrop into 2024 on the demand side. The expectation of Fed rate cuts has already put pressure on the U.S. Dollar, translating to some renewed momentum in commodity prices.

While the highs of 2022 are likely out of reach for oil in the foreseeable future, we sense that the market can support higher prices from here. Naturally, the energy sector and oil services stocks including Transocean are well-positioned to benefit from this dynamic.

Source: FINVIZ.com

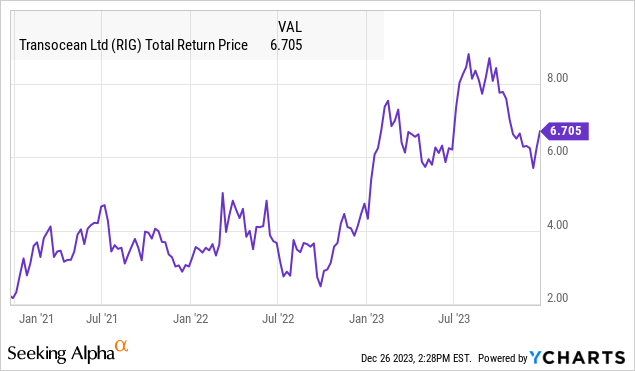

5) Compelling Technical Setup

From RIG’s stock price chart, we like the setup here at an important inflection point. Shares have bounced off a recent low of around $5.50, corresponding to the recent rebound in the price of crude oil. Curiously, this same level has represented a strong area of technical support going back over the past year.

With the ongoing rally, RIG has now broken out above a trend in place since late September as a strong signal for us that there is room for the momentum to continue. Ultimately, we see the highs above $8.50 as an upside target representing an attractive return potential of more than 25% over the next year.

Seeking Alpha

Final Thoughts

Transocean isn’t perfect but we see room for the stock rally to accelerate and even outperform the broader oil & gas equipment and services industry to the upside. The bullish case here is that stronger financial results over the next several quarters can support an expansion of valuation multiples.

In terms of risks, a deterioration in the macro growth outlook sending energy prices lower would undermine any earnings expectations for the year ahead. It will be important for Transocean to deliver on firming operating margins and climbing cash flows going forward.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of RIG either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Add some conviction to your trading! Take a look at our exclusive stock picks. Join a winning team that gets it right. Click for a two-week free trial.