Summary:

- Micron’s earnings report appeared to be a massive blow to the bull case.

- However, it was the end of the bear case for this memory market downturn.

- Nearly everyone missed the critical piece that bits shipped bottomed in FQ1. Naturally, the rest of the financials follow suit when this happens.

- Even if Samsung isn’t “cutting production,” Micron is seeing bit demand bottom, which means the stock isn’t heading any lower.

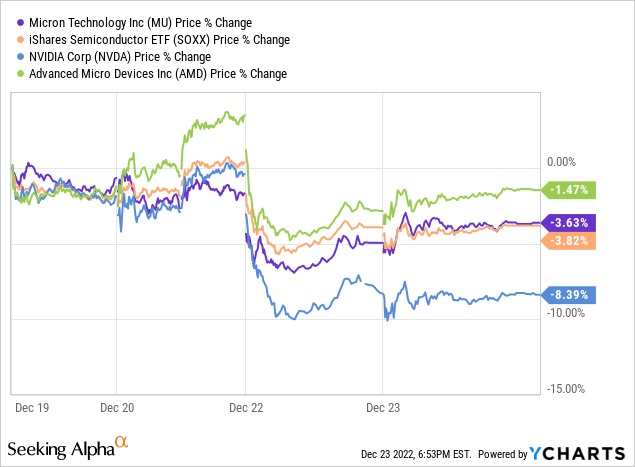

knowlesgallery

Am I a little excited by Micron’s (NASDAQ:MU) earnings report? You bet! To this point, all you’ve seen is the doom and gloom articles calling you to sell Micron, to look at just how bad it is! And those articles did an excellent job of pointing out how bad Micron’s guidance was for FQ2. The problem is the market had already been pricing this in, and those who follow Micron were not in the least bit surprised by the sequential declining nature of the FQ2 guide. The cyclical nature of Micron and its stock puts the market on watch well before a guide as dire as the one we saw on Wednesday afternoon gets published. The worst is now behind the company and its stock because of a few tiny but solid nuggets indicating a bottom. This means investors can look forward to the recovery because the market is also going to.

Understanding Bad Report From Bad Future Returns

Let me talk first to the more casual Micron investor or simply the Micron reading enthusiast for a moment before I get to my veterans.

Alarming reports are, for the most part, very well telegraphed going into Micron releases, and nearly always once a crack in the armor is found. This is why it was no surprise to me or my subscribers the company would see a sequential material decline in its financials from FQ1 to FQ2. It shouldn’t have been a surprise to anyone, really, because the CFO didn’t leave anything to the imagination in his conference with Wells Fargo, and neither did the company in its press release in November.

We also said that the second quarter would be challenged. And then as I just mentioned, the actual conditions have gotten worse.

Mark Murphy, CFO, Wells Fargo Conference, November ’22

I even wrote an article outlining what this information meant for Micron’s near-term and medium-term – five weeks ago. And, what it came down to was the bottom in terms of revenue and margins wouldn’t be FQ2, but likely FQ3 or FQ4. Therefore, all of the doom and gloom, the bottom isn’t in articles in the wake of Micron’s recent report have no factual basis for explaining why Micron has outperformed or was in line with its peers this past week. Surely, if the report were as bad as the fly-by analyst of Micron claims, the market would have set a deep new 52-week low.

That didn’t happen.

One also has to understand the market already knew about this report. Investing is about understanding market expectations, not seeing bad numbers and thinking to stay away. Of course, anyone can do that, and the market isn’t a cross-eyed doofus looking down its nose at what’s in front of it. But many people do this to the detriment of their portfolio. Therefore, you must read the room and understand where the market is looking.

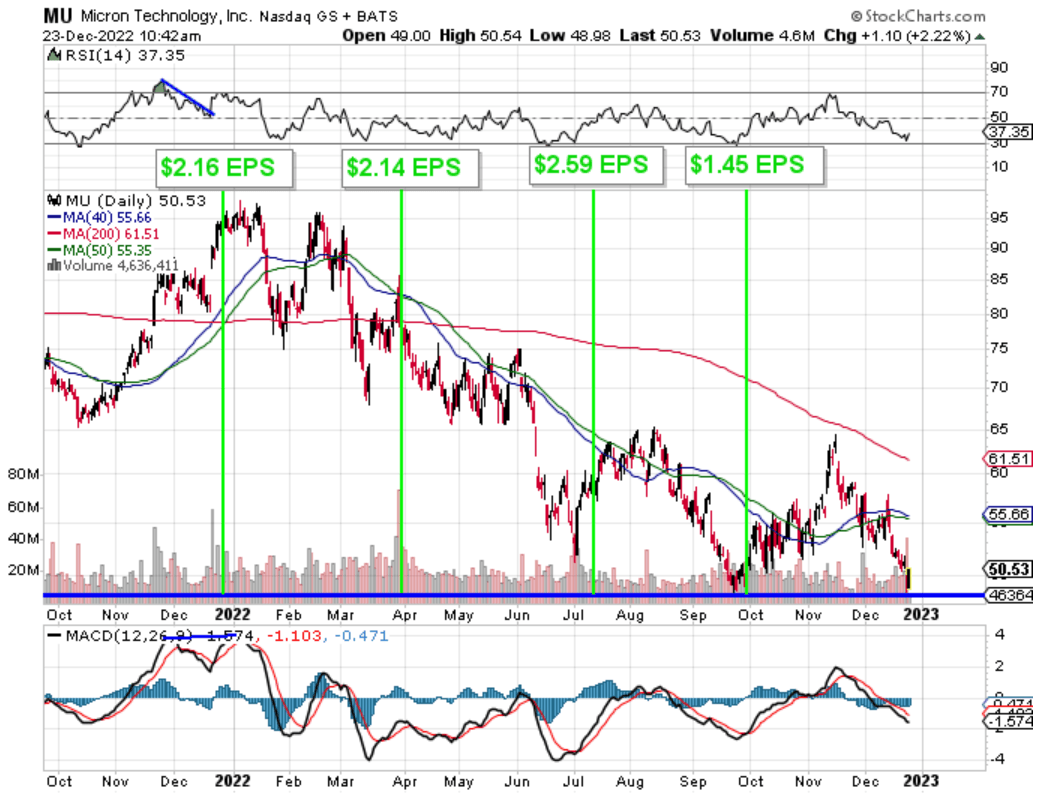

Micron isn’t about to drop the most it has this entire time with the terrible guide now delivered. No, it’s been pricing this in for months. The turn started well before there was any hint of weakness. In fact, the stock peaked almost seven-and-a-half months before EPS peaked.

Annotations mine, stockcharts.com

If someone is telling you the market is just realizing the breakdown in EPS and “how it will get so much worse,” they aren’t analyzing anything. The same way the market found the top is the same way it finds the bottom: looking ahead two or three quarters. Therefore, with the FQ2 guide and kitchen sink thrown at Wall Street, the market now looks for hints of recovery.

This is where I get into the deeper stuff my veterans are used to. So join the club (we have chips).

What The Report Said About A Recovery

Now, to my veterans following Micron – and me – for years. Notice the memory sales side of the business isn’t declining as much sequentially as the bottom line or margins would suggest. The company guided for a 7% quarter-over-quarter decline in revenue (after a 38% decline from FQ4 ’22 to FQ1 ’23). But gross margins will decline 63% sequentially, while EPS will decline 1,450%. How do you explain the discrepancy? To start, one must differentiate the memory business environment from the levers Micron is pulling to shorten the pain in the industry.

Revenue is higher in the funnel of understanding when demand is shifting. Gross margins and EPS are just telling you about the company’s actions; they don’t get you ahead of the market.

Revenue decreasing 12% requires looking at what it expects for DRAM ASPs (average selling prices) and bits shipped (the tug from customers on chip demand). Mark Murphy, Micron’s CFO, was asked a question about gross margins because the analyst was using the train of thought gross margins are a good tell on where the bottom is (hint: they’re not).

And you spoke about revenue and free cash flow being better in the second half. Do you believe that’s the case for gross margins as well? Do you think gross margins are bottoming here?

– Analyst Q&A, Micron’s FQ1 ’23 Earnings Call

Murphy answers by saying bits will be up but revenue down, and the levers it’s pulling will challenge gross margins.

We did say that Q1 would be the bottom for bits, and we expect bits to be up in the second quarter and revenue down.

…

But fiscal year ’23 is going to be challenging in the near term as these utilization effects and low volumes weigh on the cost per unit and weigh on margins.

…

…most visible has been our announcements to lower utilization on the front end. And that is a significant cost — and we have — most of those costs are going to be in inventories also versus period cost. And we said that $460 million of — which is over — just over half of the total fixed costs that will need to be applied will impact FY ’23.

He’s hinting at not judging the industry by gross margins or the revenue number alone. Due to the levers of a 20% reduction in wafer starts along with slowing the 1-beta ramp and higher near-term inventories, margins and the bottom line will be skewed while bits shipped start growing again.

But it’s bit shipments I want to focus on because it’s where the equity market is focusing. Stronger bit shipments are the key indicator of a bottom of a memory cycle, and growing bit shipments quarter-to-quarter always precedes the recovery in the memory market – this is the ground-level view of customers’ demand for bits.

But just because bits shipped increase doesn’t mean revenue or margins increase. If more bits are shipped, but each bit sells for less, you can wind up with lower revenue. But the key is the latter eventually follows. More demand for bits turns into more constructive pricing, and more constructive pricing leads to higher revenue and margins.

Currently, Micron is dealing with the lagging effects of lower pricing, as the lowest point hasn’t pervaded an entire quarter. So FQ2 will feel the entire pricing low, which is how you get incrementally higher demand but lower revenue.

Finding The Hints

Understanding where Micron is in the cycle requires piecing together what Micron said on its earnings call to determine what stage it’s in. The good news, and the reason why the market won’t continue selling off Micron’s shares, is because bits shipped bottomed in FQ1.

Reread Murphy’s answer:

We did say that Q1 would be the bottom for bits, and we expect bits to be up in the second quarter and revenue down.

He was driving home the point he made in the prepared remarks:

For both DRAM and NAND, we expect bit shipments to be up in fiscal Q2, but revenue to be down.

…

Beyond fiscal Q2, we expect revenue and free cash flow to improve in our fiscal second half as we anticipate a continued recovery in demand.

Bits shipped bottomed last quarter, and it’s only getting stronger for the rest of the fiscal year. While revenue will lag this increase, and profitability more so, as underutilization charges and higher-cost inventory is worked down, the market already has the confirmation of a bottom it needs.

Revenue will decrease in FQ2, but it’s due to the follow-on effects of the rapidly declining ASPs in FQ1 now fully in FQ2. So more bits at a lower price. But management did say revenue will tick up, starting in FQ3 through the end of the fiscal year.

…we expect the fiscal second half revenue to improve versus the first half of our fiscal year.

So bit demand bottomed in FQ1, revenue will bottom in FQ2 or early FQ3, and profitability will bottom likely in FQ3 or FQ4 as underutilization continues and higher-priced inventory is worked down. The rate at which this is happening is faster than past down cycles. Over the last decade, it usually takes six-to-eight quarters to arrive at the bottom financially, as EPS gradually works down from the peak. This peak-to-bottom will likely only take four quarters as the demand fall off was more abrupt, leading to Micron and the industry scrambling to pull levers which takes time to work through the system, thus the significant upfront impact to the business and margins.

A Piece Everyone Should Know

Some will say, “Well, management didn’t see this slowdown very well since it had to cut again after initially saying FQ2 would be in line sequentially with FQ1. How can we trust they’re right here?” And to that, I say, bits shipped don’t lie; you can’t fake demand. And with the early signs of demand has bottomed, the rest of the process is just a matter of time.

The market knows this; it’s how every cycle has ever worked, and it’s only gotten more anticipatory over the years so as not to miss the turn.

Others will say Samsung (OTCPK:SSNLF)(OTCPK:SSNNF) isn’t playing ball and will hurt Micron (and SK Hynix) further. The truth is Samsung hasn’t been a technology leader for years now, and it’s having serious yield trouble with EUV and transitioning nodes. Notice its wording when it was asked about utilization cuts (wafer starts):

““We are not considering an artificial production cut,” Han Jin-man, executive vice president of memory business at Samsung”

The key word is artificial. It doesn’t need help lowering production because it’s already struggling to maintain output as its yields have reportedly been horrendous as EUV has not been a well-managed transition. So much so it’s already showing up as a loss of market share, resulting in the company’s lowest market share since 2014.

Samsung Electronics’ DRAM sales fell 33.7 percent from US$11.121 billion in the second quarter to US$7.371 billion in the third quarter. The drop eclipsed the overall market decline. As a result, its market share in terms of sales also fell by 2.7 percentage points from 43.7 percent in the second quarter to 41.0 percent in the third quarter. This marked the lowest share in eight years since the third quarter of 2014 based on IDC data.

Even if Samsung wasn’t struggling, the fact bit demand for Micron is growing indicates its taking market share or the industry is bottoming, or both. I wouldn’t be surprised if it were both, but Micron is certainly bottoming.

It comes down to keying in on bit demand; it keeps you at the front of the market’s expectations. Now is the time to buy Micron; its stock has likely bottomed because it has signaled to the market the industry has already bottomed. Not only is the stock within spitting distance of 52-week lows, but the information from its earnings report confirms there’s no reason to go lower. This combines to create the best opportunity you may have in this cycle.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclosure: I/we have a beneficial long position in the shares of MU either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Tech Cache Is 25% Off For The Holidays!

Do two things to further your tech portfolio. First, click the ‘Follow’ button below next to my name. Second, become one of my subscribers risk-free with a free trial and the largest discount ever offered! Get my thoughts in real-time instead of reading my public articles weeks later containing only a subset of information. I provide four times more content (earnings, best ideas, etc.) each month than you read for free here. Plus, you’ll get ongoing discussions among intelligent investors in my chat room. Join now with 25% off your first year!