Summary:

- 2U is one of the “Big 2” online education providers, along with Coursera; I will compare the two in this post.

- 2U has a $1 Trillion Market opportunity in E-Learning.

- 2U’s share price is down 79% from its highs in February 2021, despite growth in the Ed-Tech industry.

- A $1 Billion Buyout offer has recently been reported by Bloomberg from Tiger Global backed Byju’s; this values the stock at a significant premium.

- 2U stock is currently undervalued intrinsically.

Alistair Berg

The global lockdown of 2020 caused an acceleration in the adoption of digital technologies, especially those in the online education market. According to UNESCO, over 1.5 billion students globally were adversely affected by school shutdowns during the lockdown of 2020. This major shutdown highlighted the importance of online education not just as an optional extra, but as a necessity. Even prior to the pandemic, the number of students taking at least one E-learning college course has increased each consecutive year since 2002.

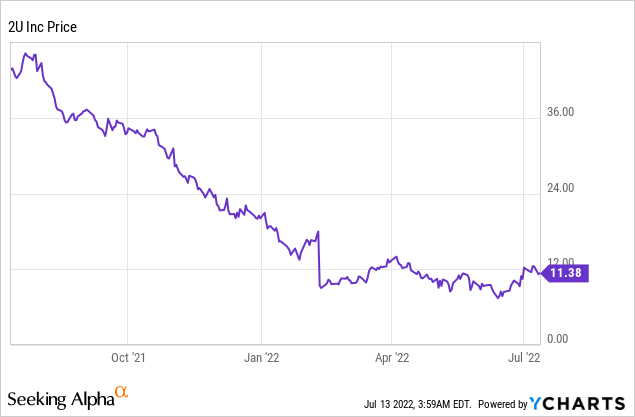

2U (NASDAQ:TWOU) is one of the “Big Two” Online course platforms in the US, along with Coursera (COUR). The platform has partnerships with leading universities which include MIT, Harvard and Berkeley, which I believe is it’s unique selling point. It’s share price has nosedived by 79% from its highs in February 2021, mainly due to the high inflation, rising interest rate environment and single digit growth in the first quarter.

I previously covered 2U stock in February 2022, when it traded at $9/share. I valued the company then at a conservative $13/share. Since that point the stock has experienced a gain 20% to ~$11/share. A $1 billion buyout offer has recently been reported which has acted as a catalyst to move the stock toward its intrinsic value. However, the stock is still undervalued intrinsically and offers at least 30% in upside potential. Let’s go back to school as we dive into the Market opportunity, Buyout, Financials and Valuation for the juicy details.

Data by YCharts

The $1 Trillion E-Learning TAM

Colleges and Universities now require a two pronged approach to education (classroom and online) after all, are old fashioned classrooms really necessary? A recent research study suggests that over 75% of academic leaders believe online education is equal or superior to in classroom learning. Almost 70% of these academic leaders believe online courses are going to be “critical” part of future education strategies. But of course this is not just about the lecturers and universities, which can use online education to better leverage their time and generate extra income.

One in every four students also believe they learn better via online classes. Now although I don’t believe online education should or will replace every physical classroom, due to the necessary social benefits of college. There are many benefits to those taking online classes, from lower costs to greater inclusion and increased autonomy. Working professionals who live far away from physical universities and even those will family obligations will find online education much more attuned with their lifestyle. After all, we live in the “ondemand” age so why not binge watch post graduate lectures like you would Netflix?

Thus it’s no surprise that according to a study by GM insights, the E-Learning market surpassed $315 billion in 2021 and is forecasted to grow at a blistering 20% CAGR up until 2028, reaching $1 trillion by the end of the period.

$1 Billion Buyout?

A recent report by Bloomberg suggests 2U could be bought out by India based Ed-tech company Byju’s. According to a person familiar with the matter, Byju’s has offered to acquire 2U for $1 billion in an all cash deal which equates to a $15/share price. The stock popped by ~20% on the news, but still has 30% upside potential from the $11.30/share price ($877m) at the time of writing.

Despite this offer not being confirmed as official yet and still requiring board approval by 2U, it would make a lot of sense. I did some digging into Byju’s and it turns out this company is backed by Legendary Hedge Fund Tiger Global, Chinese Tech Titan Tencent and even the Zuckerberg-Chan Foundation. In addition, the company has been very active with acquisitions in 2021. According to Global Data, Byju’s acquired 10 Ed-Tech companies in 2021, with a total value of $2.5 billion. I also discovered approximately 10% of the web traffic to the edX website (owned by 2U) comes from India, so this does offer great synergy.

Business Strategy

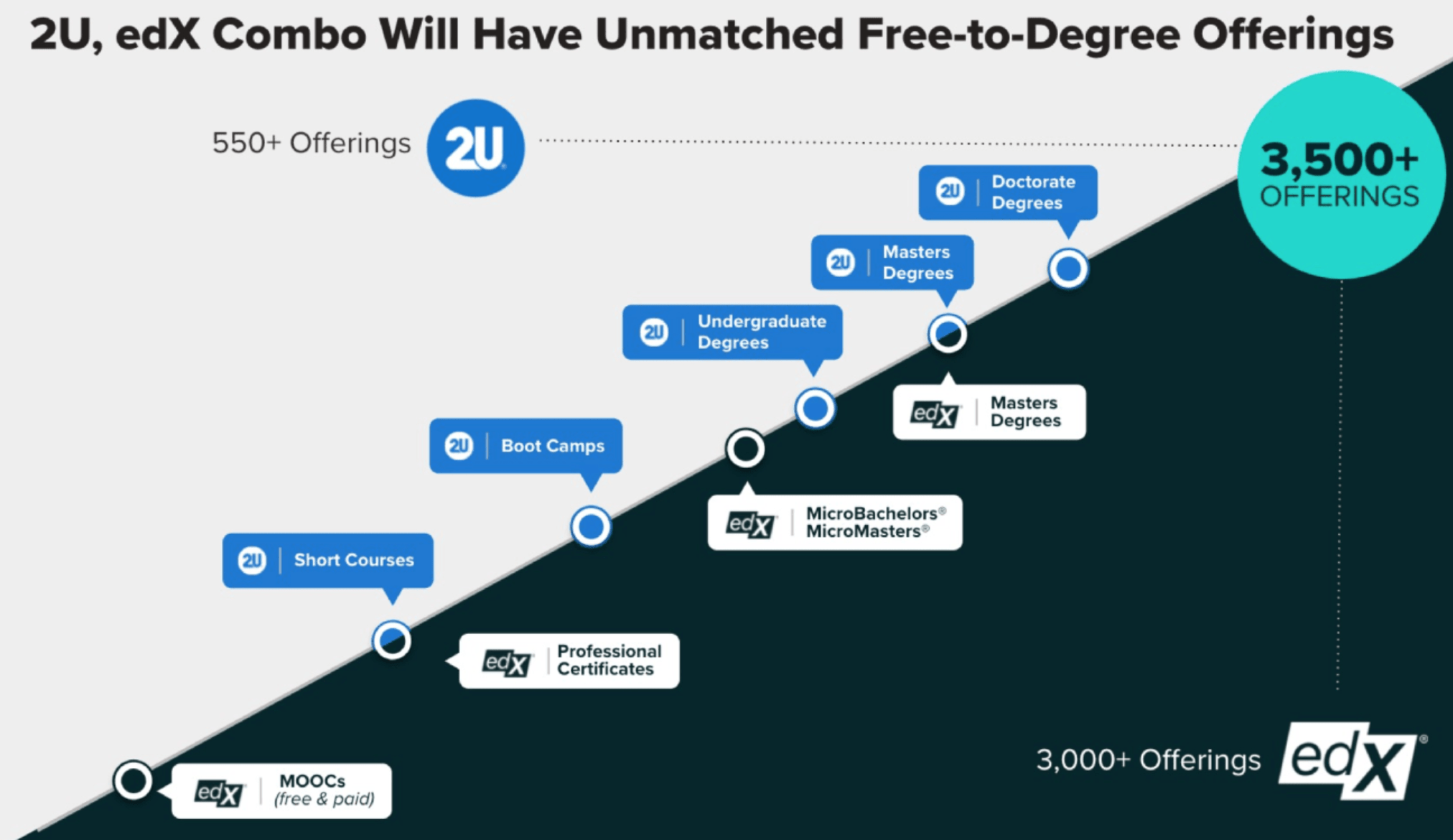

I previously covered 2U’s business model in a past post, but here is a short overview. 2U merged with edX in 2021 and now has over 44 million registered learners globally. It has valuable partnerships with 38 of the top 40 Universities, 1,200 enterprises and over 230 university and corporate partners.

The companies has over 4000 courses and uses a “Free to Degree” strategy, which offers short free courses first before up-selling students to premium degree programs. 2U accomplishes the up-sell via a controversial strategy of having salespeople call up students, I discuss more on this in the risks section.

2U free to degree (2U investor relations)

Managements plan is to try and convert just 0.03% of the 39 million registered edX learners to its premium degree offerings. The goal is to lower its cost of student acquisition from $3900 to $3500.

2U vs Coursera Comparison

Best Courses?

I have compared 2U to larger rival Coursera (COUR). In terms of courses 2U (and edX) offers a better selection of premium universities such as Harvard, MIT, Berkeley, Cambridge and Oxford. Whereas the most elite University Coursera has is Stanford (the company was founded by a Stanford professor). However, Coursera does have a much better selection of courses from both Google (GOOG) (GOOGL) and Meta (META), which are very popular among digital professionals who wish to learn (such as myself).

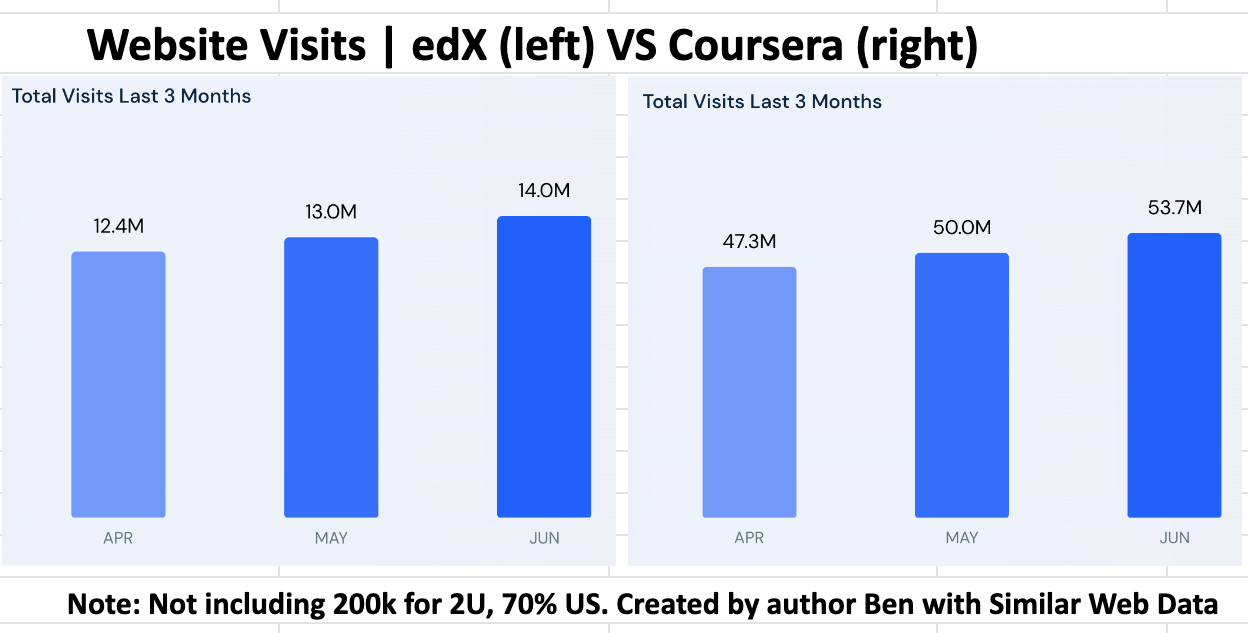

Website Traffic and Demographics

Coursera has a much larger amount of Website traffic with 53.7 million website visits in June 2022. edX on the other hand had “just” 14 million website visits in the same period. 2U’s official website has a much smaller amount of web traffic with just 200,000 visitors. However, it should be noted that 2U has a network of non branded websites and landing pages, which bring in an unknown number of leads. It also should be noted that for both websites, traffic has increased over the past three months, so could be an early sign of a great earnings report for the second quarter 2022.

Website Visits Coursera Vs 2U (created by author with SimilarWeb data)

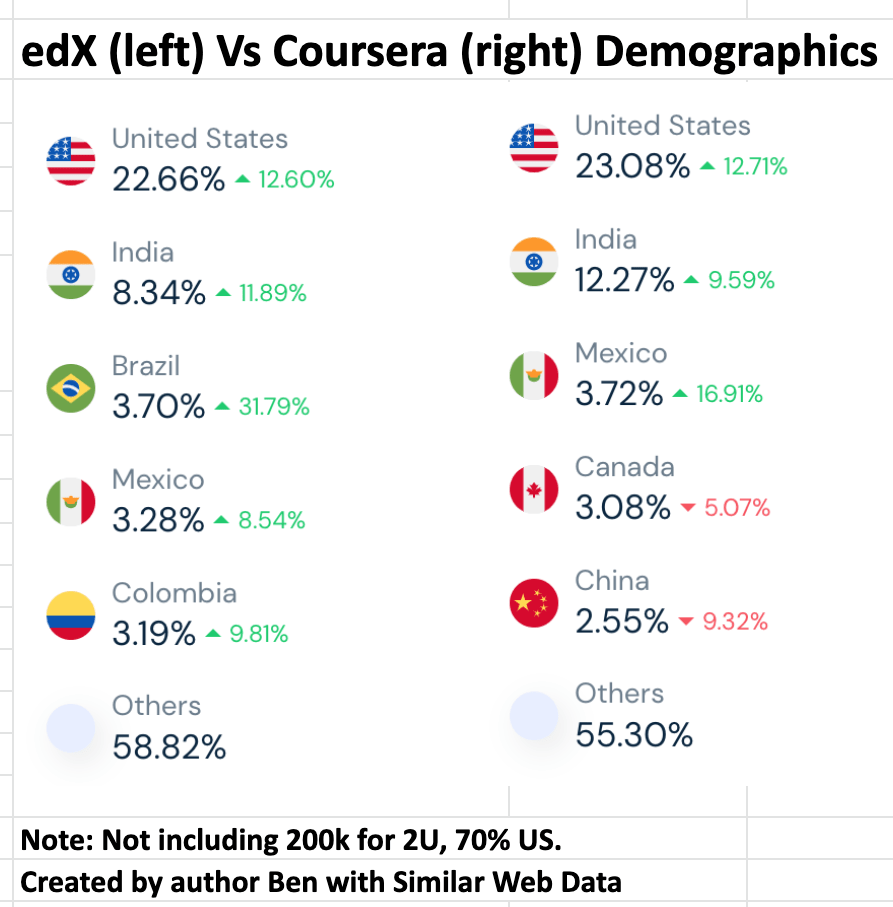

I have read some common misconceptions online which state edX’s primary web traffic is from India and thus may not be as valuable, due to income levels and the ability to afford 2U’s premium courses. However, the website traffic data I have compiled on the chart below reveals edX (owned by 2U) and Coursera have very similar demographics. Approximately 23% of website visitors are from the US, followed by India (8% vs 12%) and then Latin American countries such as Mexico (3%), Columbia (3%) and Brazil (4%).

2U vs Coursera Website Demographics (created by author Ben with SimilarWeb Data)

Financial Comparison

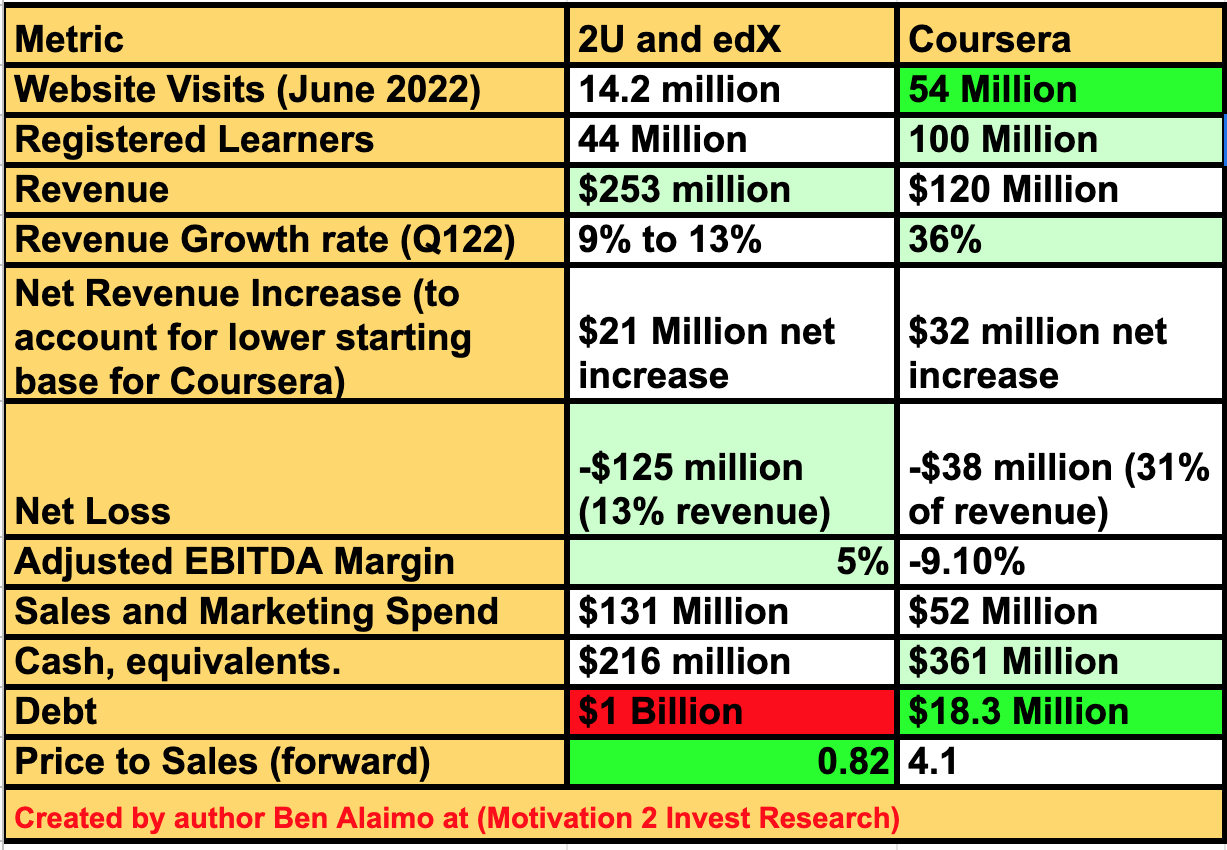

I have compared 2U (including edX) and Coursera across a variety of metrics on the table below, I will go through each line by line. As mentioned prior Coursera has a 3.7 times the amount of Web traffic, when compared to 2U (including edX). In addition, Coursera has over double the number of registered learners at 100 million, compared to 44 million at 2U. However, the financials show 2U brings in substantially more revenue. 2U generated $253 million in the first quarter of 2022, which $132 million more that Coursera at $120 million. At first glance, one may say but “Coursera is growing much faster” that is partly true but when we dive deeper, we see the difference is not as stark. Coursera generated 36% revenue growth year over year, compared to 9% for 2U over the same period. However, Coursera has a smaller revenue base to start with and thus the net revenue increase was just $32 million for Coursera compared to $21 million for 2U, which is just an $11 million difference.

Coursera vs 2U (created by author Ben at Motivation 2 Invest)

Next we will compare Net Losses (yes both companies operate at a loss). 2U generated a Net Loss of $125 million or 13% of revenue in the first quarter. Whereas Coursera generated a $38 million or 31% of revenue, thus it’s clear although Coursera’s losses are less as a net figure, they are more as a percentage of revenue.

2U also has a positive Adjusted EBITDA margin of 5%, which is greater than Coursera’s at -9.1%, although the company may calculate these slightly differently. 2U spent a staggering $131 million on Sales and Marketing in the first quarter of 2021, thus without this spend the company could be “profitable” in a traditional sense. It is clear Coursera, is seeing greater efficiency on its Sales and Marketing Spend as they spent “just” $52 million, but generated more revenue. Coursera also has a stronger balance sheet with $361 million in Cash and just $18.3 million in debt. This is much better than 2U which has an eye watering $1 billion in debt, with $216 million in cash.

Valuation

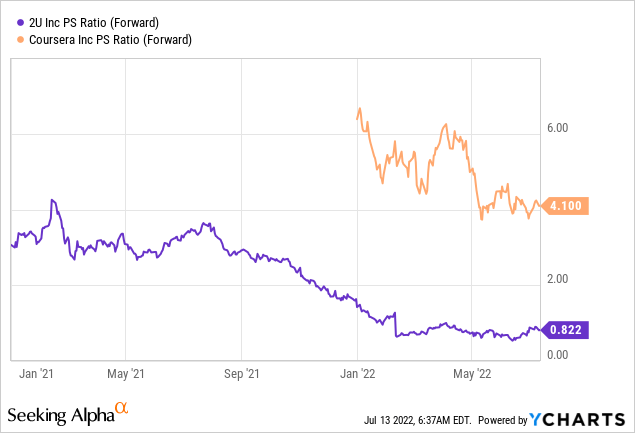

The valuation is where we see a real divergence between 2U and Coursera. 2U is much cheaper than Coursera and trades at a Price to Sales Ratio (forward) = 0.82, which is much cheaper than the Price to Sales Ratio (forward) = 4.1 for Coursera. In terms of Market cap, Coursera has a $2.23 billion vs $877 million for 2U.

Data by YCharts

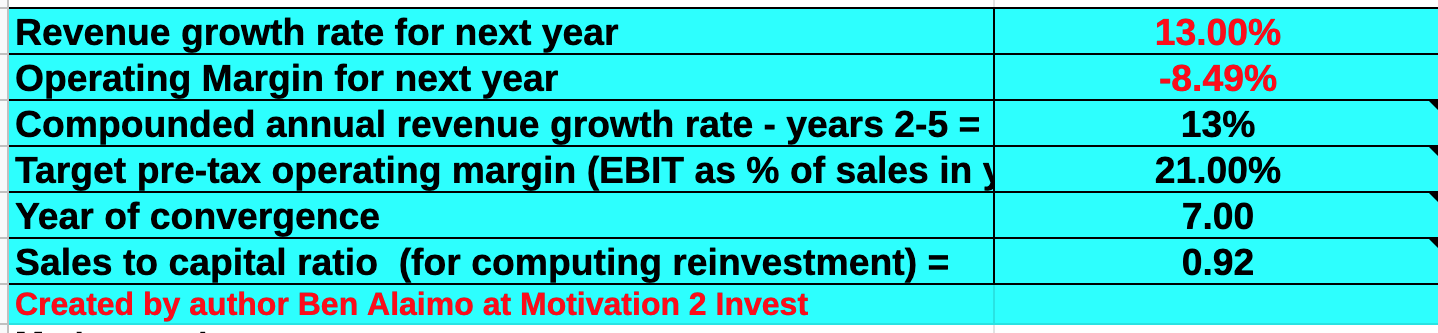

In order to value 2U intrinsically, I have plugged the latest financials in my advanced valuation model which uses the discounted cash flow method of valuation. I have forecasted 13% revenue growth for next year (in line with company’s own estimates). In addition, I have forecasted a very conservative 13% revenue growth for the next 2 to 5 years, some analyst reports are predicting 20% growth per year.

2U stock valuation (created by author Ben at Motivation 2 Invest)

In addition, I have forecasted the companies margins to steadily increase to 21% in the next 7 years as the company scales and needs to spend less on Sales and Marketing.

2U stock valuation (created by author Ben at Motivation 2 Invest)

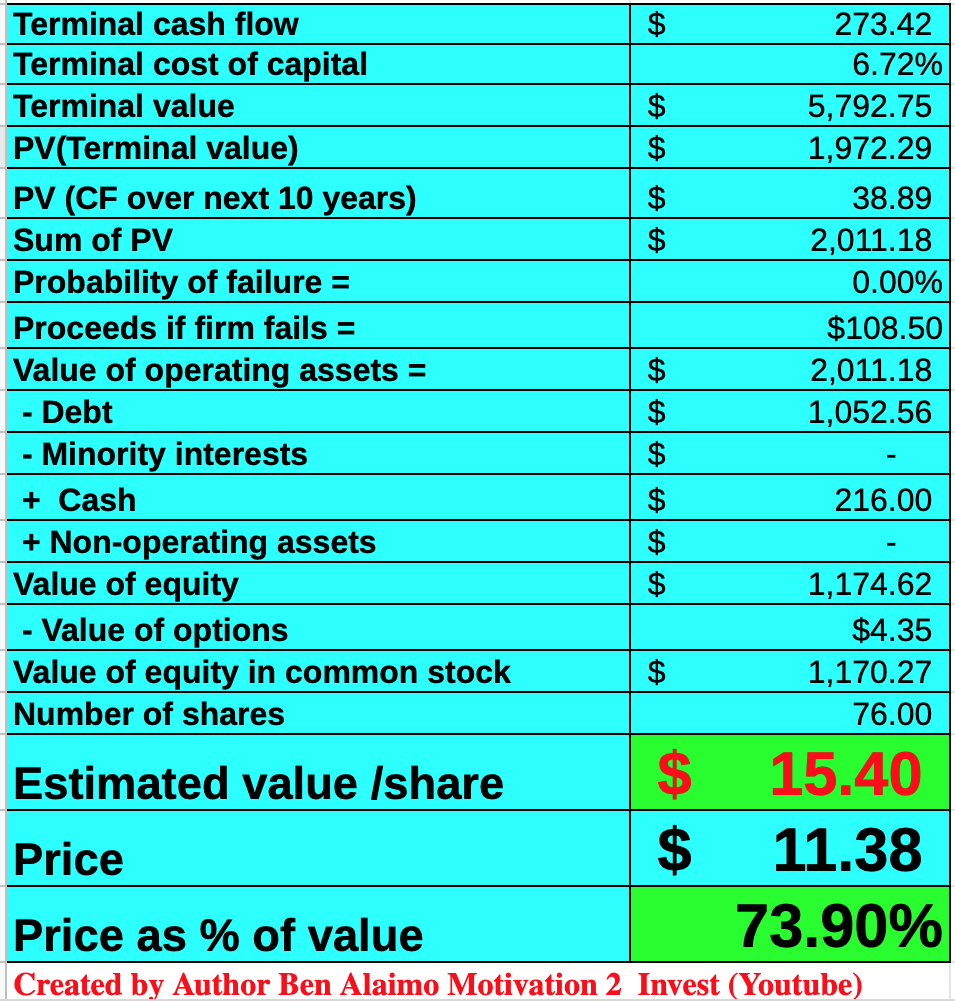

Given these factors, I get a fair value of $15/share, the stock is currently trading as ~$11.38/share at the time of writing and is thus 26% undervalued. $15/share is also the proposed buyout amount which gives me faith in my valuation model.

As a comparison, the potential acquirer Byju’s is valued at US$22 billion and has over 115 million registered students, compared to 44 million students for 2U, valued at $700 million.

Risks

High Debt

As mentioned prior 2U does have a substantial $1 billion in debt, which is surprising and risky for a growth company, which is operating at a loss. Competitor Coursera (which I also believe is a great company), has a more conservative approach and hence the higher valuation.

Controversial Sales Tactics

2U has been accused in a Wall Street Journal report of controversial sales tactics which “push” students into piling on $115K in debt and getting degrees which resulted in low salaried jobs. As with any news story, I believe this tactic has been blown out of proportion. I believe all college education is overpriced and does exploit students somewhat (classroom or online). However, with online education it is usually much cheaper and thus more inclusive. But I do hope 2U takes these reports seriously and better trains it’s salespeople to communicate more as an advisor.

Final Thoughts

Overall 2U is a leading Ed-Tech provider, the company’s elite university partnerships with Harvard, MIT, Oxford and more, are its competitive advantage in my eyes. The industry is competitive; however, as the Ed-tech market is forecasted to be worth $1 trillion by 2028, I believe it’s big enough for 2U, Coursera and many more. The company does have high debt levels and is operating at a loss as it invests for growth. However, the stock is undervalued intrinsically and the recent talks of an acquisition have acted as a catalyst for the stock to move.

Disclosure: I/we have a beneficial long position in the shares of TWOU either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.