Amazon.com, Inc.’s Q1 earnings report shows strong performance, with revenue and EPS beating estimates.

The twin growth engine of AWS and Ads is building momentum.

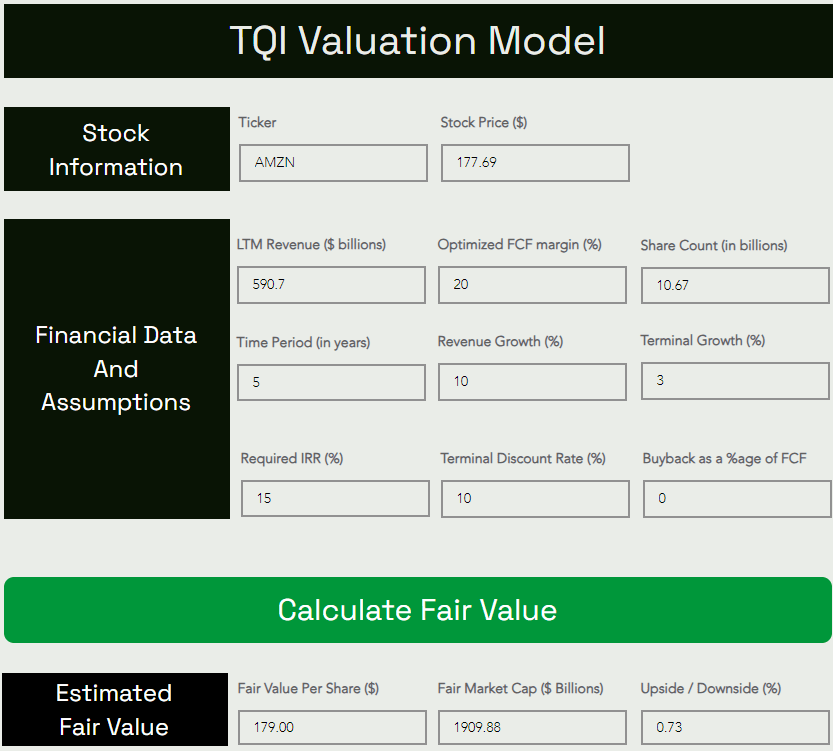

Amazon’s fair value estimate has increased to $179 per share, and the stock is still a long-term “Buy” as per our valuation model.

Brett_Hondow/iStock Editorial via Getty Images

Introduction

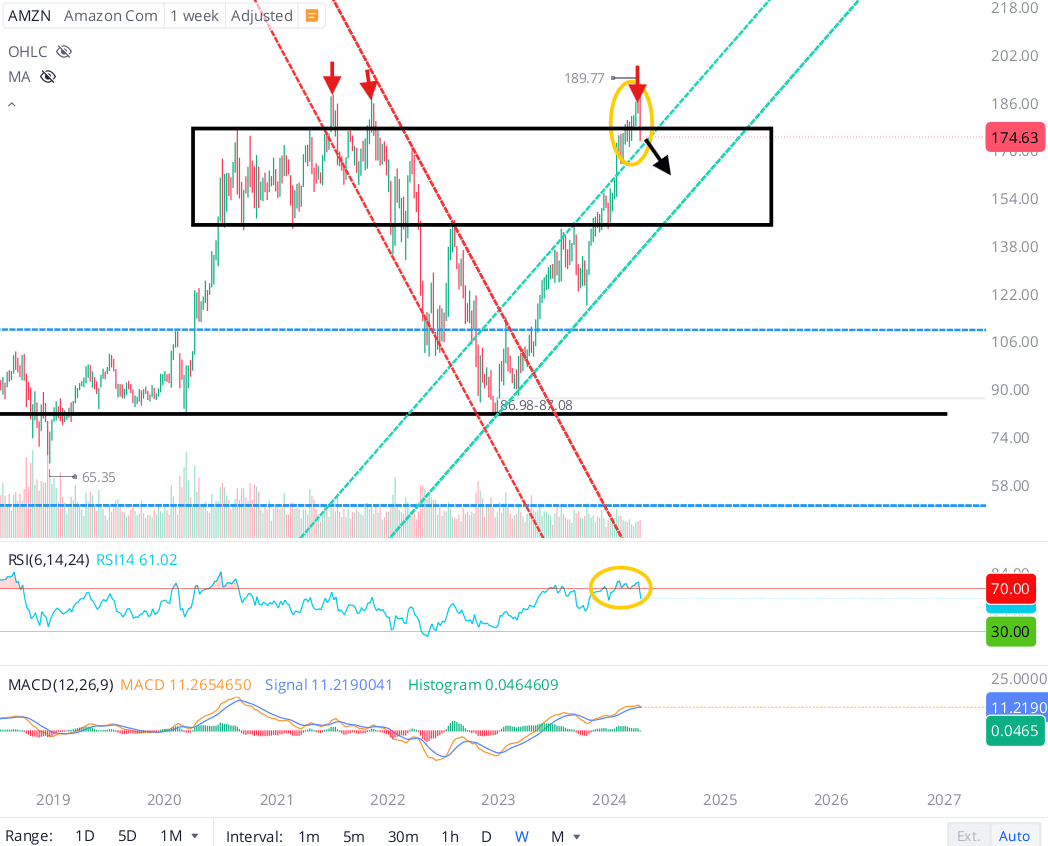

In “Big Tech’s Big Breakdown, The Technical Setup Ahead Of Earnings,” I wrote the following about Amazon.com, Inc. (NASDAQ:AMZN):

Along with Meta and Google, Amazon has been one of our largest holdings at TQI since its inception in late 2022. After being undervalued throughout 2022-23, Amazon’s stock has finally caught up to our fair value estimate of $175 per share. In fact, Amazon overthrew its rising channel recently to break out of its resistance box almost in a straight line move up; however, this upside breakout has been firmly rejected with the stock re-entering the resistance box on the back of last week’s pullback.

WeBull Desktop

With AWS stabilizing in recent quarters and management announcing several large deals last time around, Amazon’s financial performance is likely to remain robust. The operating leverage story at Amazon looks lucrative, and I expect to see rapid earnings growth over the medium term.

Considering AMZN is still fairly valued, I don’t see the need for a deeper pullback here; however, if the Q1 earnings report disappoints and/or the macro worsens, Amazon could consolidate within the broad resistance box [$140-$180] until fresh impetus is found for the next leg higher.

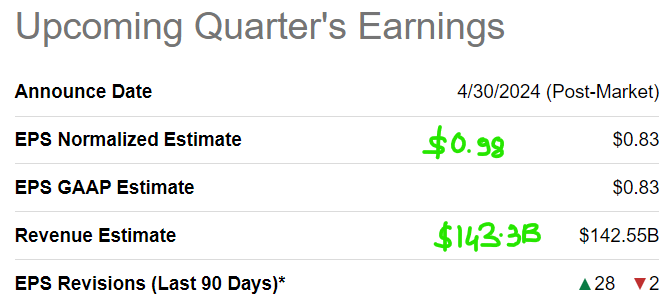

Heading into its Q1 report, Amazon was projected to deliver revenues and EPS of $142.5B and $0.83 per share, respectively. While Amazon’s revenue beat for Q1 is minuscule, EPS of $0.98 per share came in ~18% ahead of estimates, with AWS revenue growth of 17% y/y as the key highlight for Q1.

SeekingAlpha

In this note, we will briefly review Amazon’s Q1 2024 report and re-run AMZN stock through TQI’s Valuation Model to see if the stock is still a buy.

Brief Review of Amazon’s Q1 Earnings Report

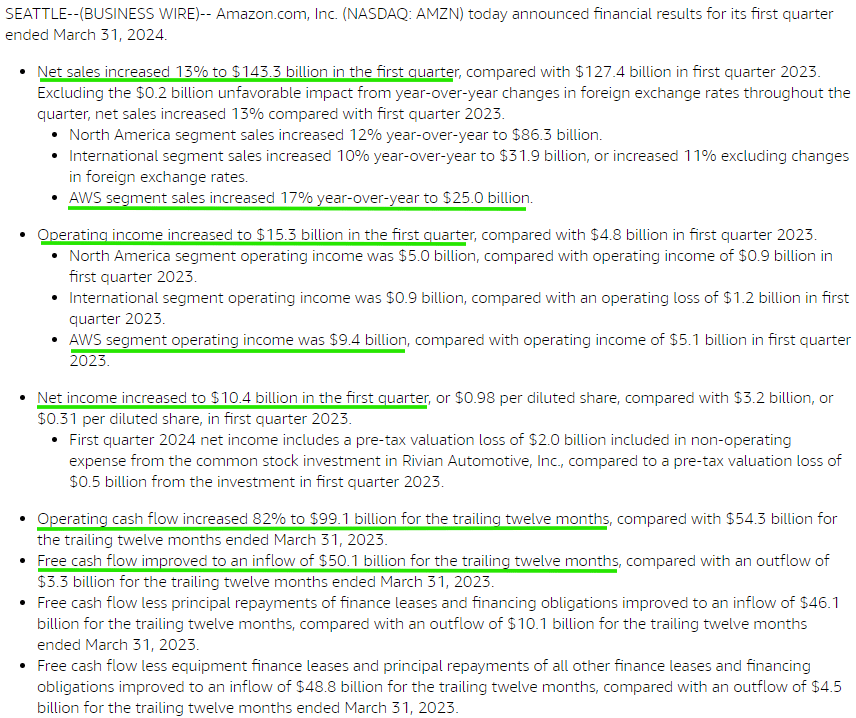

In Q4 2023, Amazon’s net sales rose +13% y/y to $143.3B, driven by a stronger-than-expected growth re-acceleration at Amazon Web Services (“AWS”) and continued momentum within Ads and the retail ecosystem. With AWS contributing nearly ~61% of Amazon’s operating income in Q1, the importance of Amazon’s cloud business cannot be understated. For a while now, the market narrative has been that Microsoft Azure (MSFT) is the big winner among cloud hyperscalers in the era of GenAI; however, Amazon’s cloud business expanding faster than Microsoft in dollar terms is a sign that AWS can defend its market share, and stay the leading hyperscaler in the future!

Amazon Investor Relations

During Q1 ’24, Amazon’s operating income increased to +$15.3B, driving TTM operating cash flow higher to $99.1B (up +82% y/y). Over the last twelve months, Amazon has generated free cash flows of $50.1B, and in my view, the operating leverage story at Amazon is going from strength to strength. A lot has been made about Amazon’s valuation multiple, but based on current pricing, Amazon is trading a P/FCF multiple of ~36x, which is not excessive for a company growing sales at a healthy clip and expanding margins rapidly.

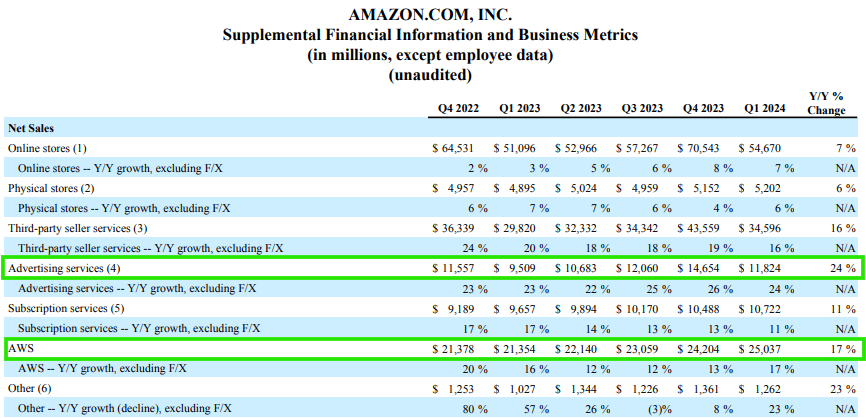

As you may know, my investment thesis for Amazon has been centered around its twin growth engine of AWS and Ads. We have already talked about AWS’ importance; however, Amazon’s Ads business is no slouch, with growth of 24% y/y to $11.8B in Q1 2024. While AWS is already a $100B ARR business, Amazon Ads business is growing faster and looks on track to reach that $100B ARR milestone in the next few years.

Amazon Investor Relations

Here’s what Andy Jassy (Amazon’s CEO) had to say about this report (emphasis added):

It was a good start to the year across the business, and you can see that in both our customer experience improvements and financial results. The combination of companies renewing their infrastructure modernization efforts and the appeal of AWS’s AI capabilities is reaccelerating AWS’s growth rate (now at a $100 billion annual revenue run rate); our Stores business continues to expand selection, provide everyday low prices, and accelerate delivery speed (setting another record on speed for Prime customers in Q1) while lowering our cost to serve; and, our Advertising efforts continue to benefit from the growth of our Stores and Prime Video businesses. It’s very early days in all of our businesses and we remain excited by how much more we can make customers’ lives better and easier moving forward.

In my view, Amazon’s Q1 report is the best one among big tech companies so far in this earnings season. Amazon’s profitability concerns are a thing of the past; however, the ongoing revenue mix shift towards faster-growing, higher-margin AWS [cloud] and Ads businesses will likely continue to drive incremental improvements in profit margins and cash flow generation at this big tech giant for years to come.

Ahead of earnings, the fervor of a potential dividend from Amazon was quite high, but I see no indication of a capital return program in the Q1 report. That said, given Amazon’s scale and profitability, I continue to think that it is only a matter of time before Amazon transforms from a cash cow to an “infinite buyback pump” [a capital return machine] for its shareholders.

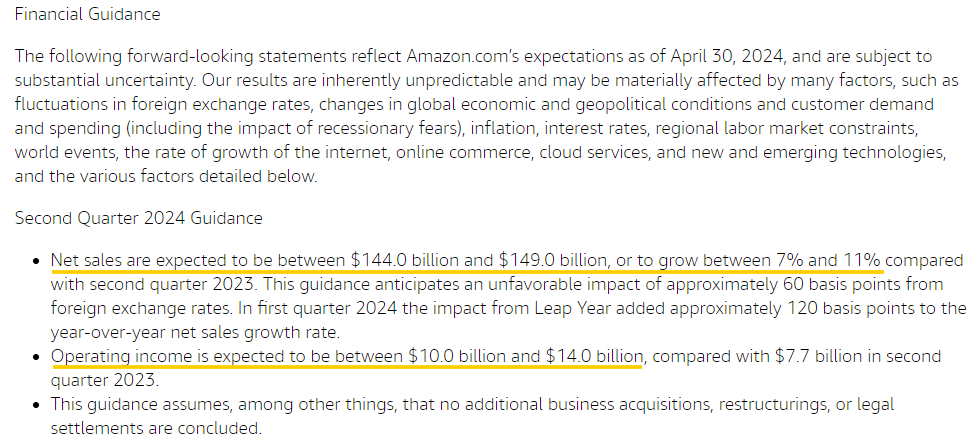

Now, coming to guidance – for Q2 2024, Amazon’s management has guided for net sales of $144-149B (growth of 7-11% y/y) and operating income of $10-14B. The sales guidance calls for a sizeable moderation in growth and falls short of consensus street estimates of $150B. As long as economic resilience persists, Amazon will likely beat these numbers, given its management’s history of sandbagging guidance.

Amazon Investor Relations

With its impressive performance in Q1 2024, Amazon’s twin-growth engine is building momentum. While the Q2 guide is lighter-than-expected, Amazon’s business fundamentals are moving in the right direction.

Following the release of its Q1 report, Amazon is trading at ~$177 per share (up by +1.5% in after-hours at the time of writing) – slightly above our previous fair value estimate. Let’s see where our model sees Amazon’s fair value and expected return now.

Is AMZN Stock A Buy, Sell, or Hold?

According to TQI’s valuation model, Amazon’s fair value estimate has moved up from ~$171 to ~$179 per share (or $1.91T) in light of its Q1 2024 report. With the stock trading at ~$177 per share, AMZN is fairly valued, and you know we couldn’t say the same thing about most of AMZN’s high-flying “Magnificent 7” big tech peers.

TQI Valuation Model (TQIG.org)

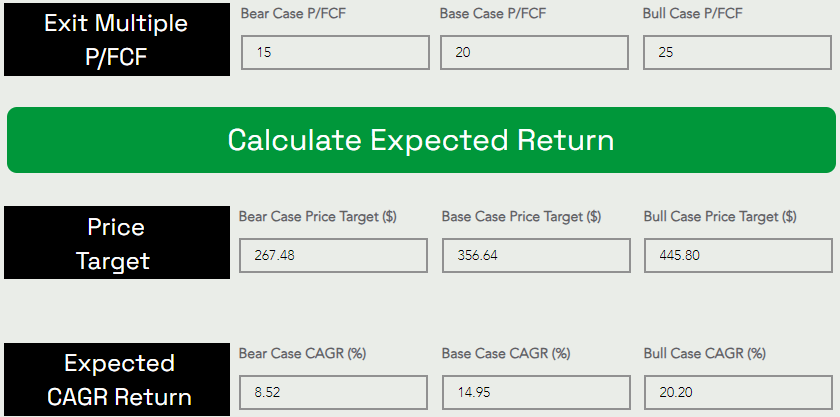

Predicting where a stock would trade in the short term is impossible; however, over the long run, a stock would track its business fundamentals and obey the immutable laws of money. If the interest rates were to stay depressed, higher equity multiples would be justifiable. However, I work with the assumption that interest rates will eventually track the historical long-term average of ~5%. Inverting this number, we get a trading multiple of ~20x.

Assuming an exit multiple of 20x P/FCF, I see Amazon’s stock price rising from ~$177 to ~$356 at a CAGR rate of ~15% over the next five years.

TQI Valuation Model (TQIG.org)

While Amazon’s 5-year expected CAGR return is more or less in line with our investment hurdle of 15%, AMZN stock remains a long-term “Buy” under our valuation process (especially since our model does not consider buybacks/dividends, which are only a matter of time).

Concluding Thoughts

Barring a macroeconomic shock, I think Amazon will re-test its all-time highs sometime in 2024, with the business looking stronger than ever before. In combination with its GenAI innovations [like Q [code bot launched today] and Rufus (AI-shopping assistant)], I think Amazon’s retail ecosystem and twin-growth engine of AWS & Ads will continue to push AMZN’s revenues and free cash flows higher over time.

Amazon is a fundamentally sound business with market-leading positions in humongous secular growth markets: e-commerce, digital advertising, and cloud. Based on its improving business fundamentals, reasonable valuation, and attractive long-term risk/reward, I continue to view Amazon as a solid investment in the $170s.

Key Takeaway: I rate Amazon.com, Inc. stock a “Buy” at $177 per share, with a strong preference for staggered accumulation.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of AMZN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

How To Invest In This Environment?

In order to navigate this tricky economic period, we are pursuing “Bold, Active Investing with Proactive Risk Management” at our investing group – “The Quantamental Investor“. With a laser focus on valuations, profitability, and balance sheet strength, we are buying the winners of tomorrow! Furthermore, we are utilizing index-based options to guard against significant broad-market declines. Join us today to prepare for whatever the market may throw at you in 2024!