Summary:

- American Airlines will report Q3 numbers on October 20, when it is well understood that demand for air travel is back at an all-time high.

- Key topics of conversation will probably include capacity, costs in the face of labor challenges, and the strength of the international business.

- Be careful with airlines in general and AAL specifically, considering potential headwinds in 2023 and the historically poor risk-adjusted returns.

FangXiaNuo

Following a long period of 18 months in which airline stocks sank progressively in the face of lingering COVID-19 challenges, the sector is now on fire. September 2022 earnings season has been highly bullish for the space, as airline shares (JETS) have climbed a solid 10% in only 12 trading days.

Improved investor sentiment could continue to fuel the rally after American Airlines (NASDAQ:AAL) reports what is widely expected to be another stunner, following Delta’s (DAL) and United’s (UAL) well-received reports. While I would not be surprised to see American’s numbers shine, I remain skeptical of the stock ahead of what could be a year of deceleration in economic activity.

Red-hot demand for air travel

Regarding the headline numbers, analysts expect American to post YOY revenue growth of 50% in Q3. If achieved, the figure would fall short of United’s 66% reported on October 18 and Delta’s 53% delivered in the prior week. EPS of $0.56 would be only the second positive earnings figure witnessed since the start of the pandemic, in the March 2020 quarter.

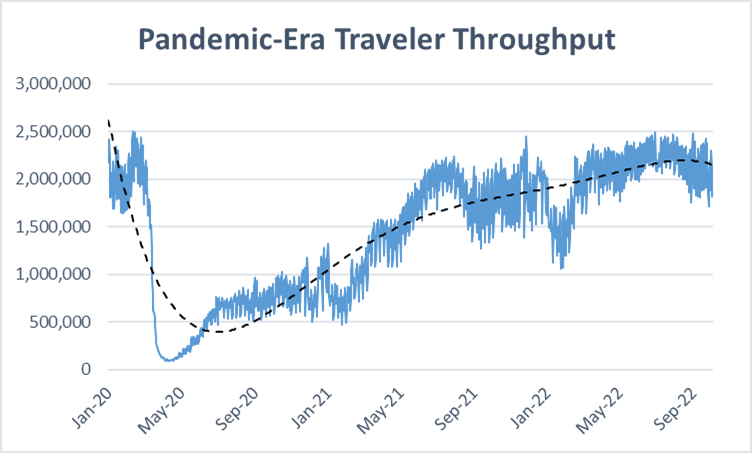

At this point, it is very well understood that demand for air travel is pretty much back at an all-time high (see airport traffic chart below). The key players in the airline industry have begun to report metrics that are now better than pre-pandemic levels — think per-unit revenues, occupancy, and even segment sales, in many cases.

DM Martins Research, data from tsa.gov

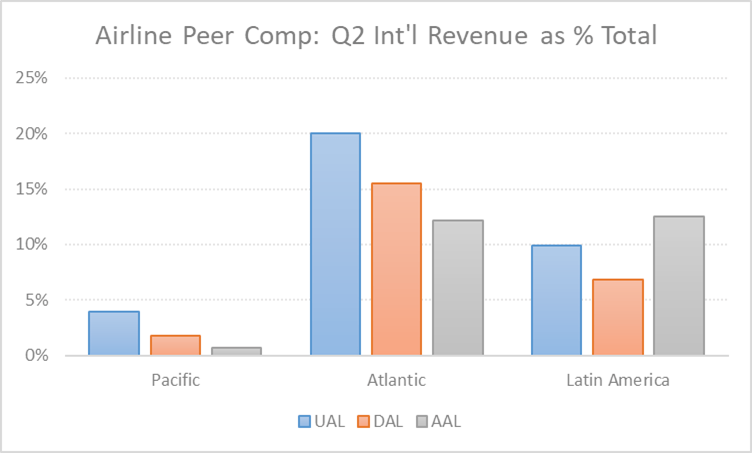

I will be interested to see how American performs outside the US. This is where Delta and United were able to flex their muscles the most, since international travel has lagged behind the rebound in domestic activity during this COVID-19 recovery. The potentially bad news for American is that the company is heavily exposed to a Latin American market (one-half of international revenues in Q2, see below) that, based on its peers’ reports, has performed quite a bit worse than their Transatlantic businesses.

Lastly, the earnings day discussions will not be complete without a serious conversation about capacity, which in turn also impacts ex-fuel operating costs. The airline space has been suffering from labor shortages and, in some cases, delayed aircraft deliveries from Boeing (BA). Not having the resources to capitalize on red-hot demand can be a problem for a sector in which “the good times” can be so rare and end so quickly.

DM Martins Research, data from company IR pages

American Airlines is not my favorite airline stock

My take on the airline sector is to avoid it in general, considering the historically poor risk-adjusted returns, unless one is looking to make a quick buck betting on the early stages of economic expansion (probably not now). Also keep in mind that hot inflation and rising interest rates can quickly lead to decreased discretionary spending as early as the first few months of 2023, which could be bad news for airlines.

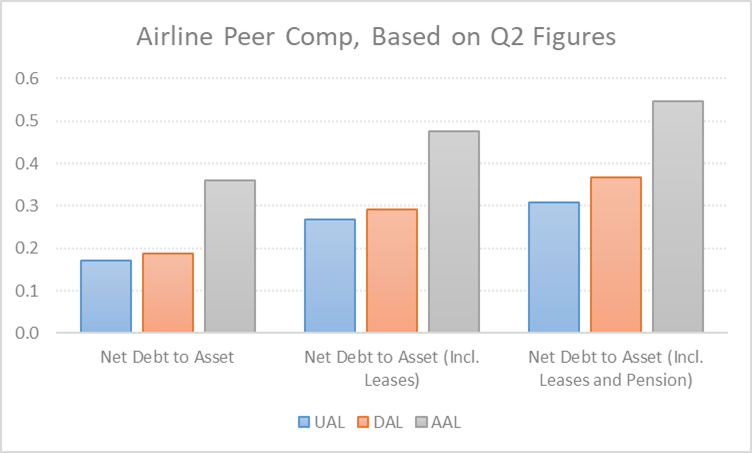

The other approach is to be market neutral by betting on winners against losers. Assuming that this is the trading proposition, I would likely be long DAL and UAL and short AAL — an idea that I have defended since the publishing of my first airline sector deep dive, in 2018. The three key reasons supporting my skepticism towards the latter are (1) a less robust balance sheet (see chart below), (2) unit margins that are the lowest of the Big 3 legacy carriers, and (3) an international mix that leans too heavily on Latin America and not enough on the more lucrative Atlantic business.

DM Martins Research, data from company reports

Of course, AAL can still move higher this week, depending on the quality of the Q3 results and outlook. But even in the immediate term, I wonder whether most of the upside opportunity may have already been captured in the earlier days of this earnings season. For these reasons, I stay clear of AAL at this moment.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in DAL, UAL over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Join EPB Macro Research

EPB Macro Research is a thriving community of investors seeking better risk-adjusted returns, while optimizing their portfolios to benefit from the next economic cycle. I invite you to join EPB, where you can read more about multi-asset diversification and participate in the discussions about the markets, the economy and investment strategies.