Summary:

- Shares of Box have been among the few enterprise software stocks to enjoy gains this year, yet outperformance in 2023 is likely to continue.

- In its most recent quarter, Box accelerated constant-currency billings to 20% y/y growth, which is a very positive growth indicator.

- At the same time, the company also hit record pro forma operating margins.

- The company is still modestly valued at <4x FY24 revenue.

Brad Barket/Getty Images Entertainment

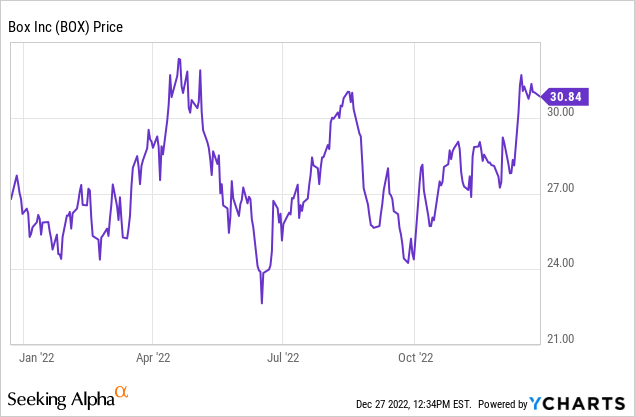

There are very few tech companies, let alone in the enterprise software space, that have not seen massive declines in share price this year. Box (NYSE:BOX) stands alone as a rare exception: the file storage and sharing company has seen its stock rise by ~15% this year, a testament both to its modest valuation as well as the recession-proof, recurring nature of its enterprise business.

Despite its relative outperformance this year, I continue to hold onto my view that Box will continue to beat the broader market indices in 2023:

Box remains a core holding in my portfolio, and I am still bullish on the name despite already capturing nice gains on it this year. In my view, the company continues to enjoy secular tailwinds from the proliferation of remote/hybrid work and distributed teams (necessitating an enterprise-grade file sharing and collaboration solution like Box), and additional products like e-sign that are natively embedded into Box’s core functionality will continue to drive growth for years to come. In addition, once installed and an entire company’s files live on Box’s servers, it becomes very difficult to replace Box with another competing solution: making its ARR base quite stable and secure.

Here is my full bull case for Box:

- Box’s product portfolio expansion has led to a $74 billion market – Despite competition, Box cites a massive $74 billion market across storage, content collaboration, and data security. That’s a big enough space for multiple incumbents, and also suggests Box is only currently ~2% penetrated into this overall market. Recent portfolio additions like Box Sign have greatly expanded Box’s potential.

- Multi-product strategy is winning – Now roughly half of Box’s new deal bookings come from Box Suites customers who are purchasing more than one Box product. Additions like Box Sign continue to pave the way for incremental revenue growth.

- Founder-led – Though many Silicon Valley startups have been passed over from their founders to professional CEOs, Box remains led by its co-founders Aaron Levie and Dylan Smith as CEO and CFO, respectively.

- Enterprise orientation – Of all of its well-known competitors, Box is the only company that is enterprise-focused. The company touts its security features plus advanced capabilities like Box Skills as key distinguishers versus the likes of Dropbox.

- Growth plus profitability in one package – Box touts “growth + FCF margin” as its key metric for balancing revenue and profitability; and this has marched steadily upward to 33% in FY22. Box hopes to hit 44% by FY25.

- Possibility of an acquisition – Buyout speculation started brewing for Box in 2021, and chatter on Dropbox picked up in 2022 as well. Though a deal may not be imminent, the company’s product fits neatly into one of the other software giants’ portfolios (Salesforce (CRM) or Oracle (ORCL)) and its free cash flow also makes it an accretive target.

Box also remains quite modestly valued. At current share prices near $31, Box trades at a market cap of $4.40 billion. After we net off the $402.7 million of cash and $368.9 million of debt on Box’s most recent balance sheet, the company’s resulting enterprise value is $4.37 billion.

Meanwhile, for FY24 (the fiscal year for Box ending in January 2024), Wall Street analysts have a consensus revenue and EPS estimate of $1.10 billion (+10% y/y) and $1.47 (+27% y/y) respectively (data from Yahoo Finance). This puts Box’s valuation multiples at:

- 3.9x EV/FY24 revenue

- 21x forward P/E

Especially at a time that the market is laser-focused on stability and profitability, I think Box still has plenty of room for double-digit stock price appreciation in 2023. I continue to view Box as a safe hold that has a home in every portfolio. Load up on some fallen angels, too (Asana (ASAN), Palantir (PLTR), Twilio (TWLO), C3.ai (AI), and DocuSign (DOCU) are among my favorite names that come to mind), but also include Box for its defensiveness and relative lack of correlation to other SaaS names.

Q3 download

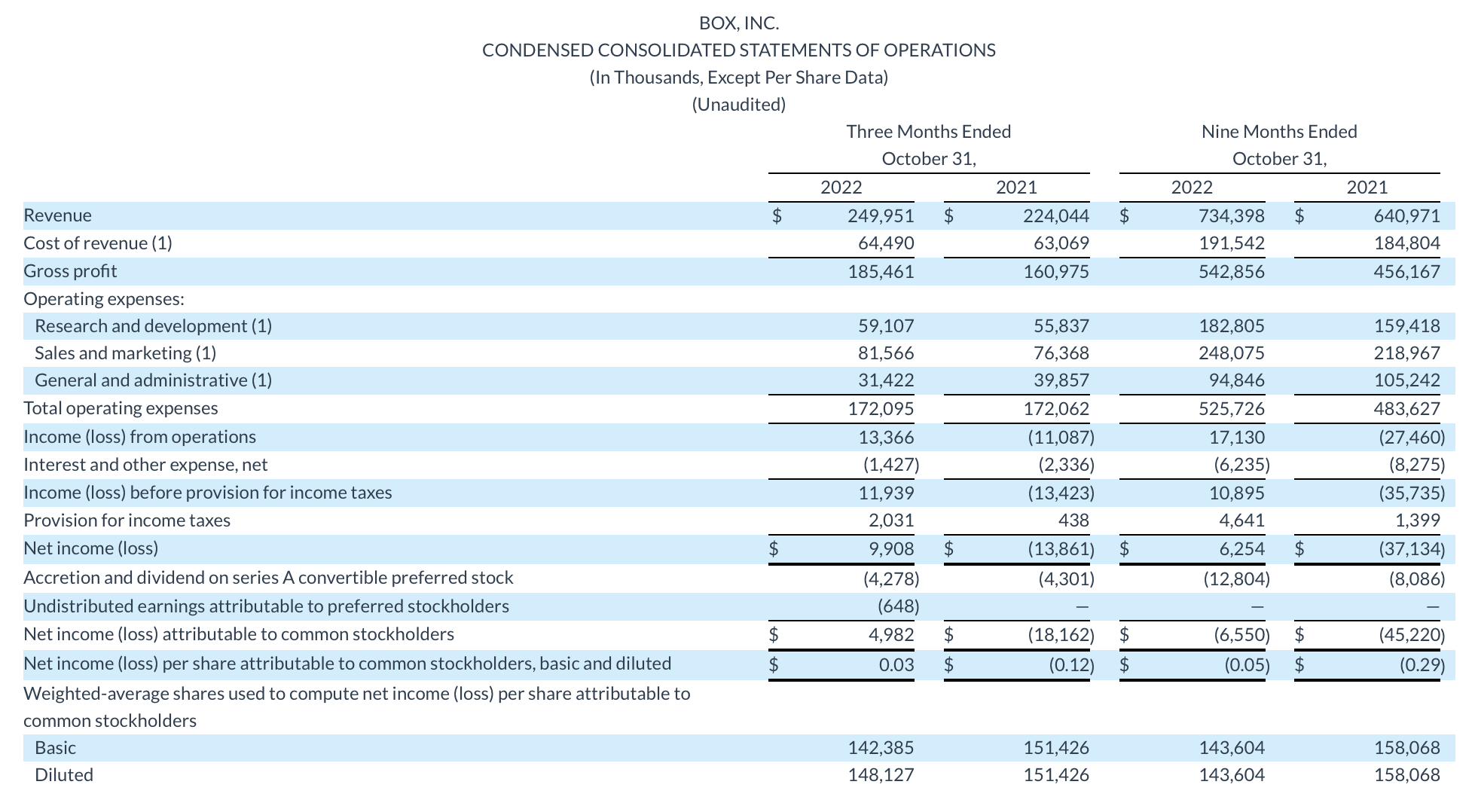

Let’s now review Box’s latest, excellent Q3 results in greater detail. The Q3 earnings summary is shown below:

Box Q3 results (Box Q3 earnings release)

Box’s revenue grew 12% y/y on an as-reported basis to $250.0 million. Like other companies in the market, Box suffered from FX headwinds that steepened relative to Q2. On a constant currency basis, Box’s revenue would have grown at 17% y/y, which is roughly flat to Q2.

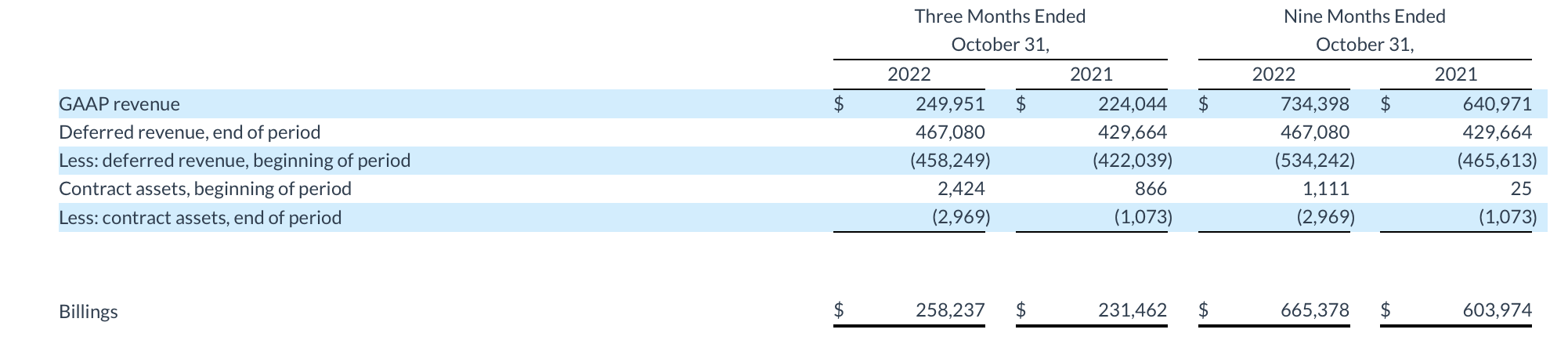

Where Box shone in Q3, however, was on billings. As seasoned software investors are aware, billings represent a better long-term view of an enterprise software company’s growth trajectory as it captures deals signed in a quarter that will be recognized as revenue in future quarters. Box’s billings grew 12% y/y to $258.2 million, but on a constant currency basis billings were up 20% y/y – accelerating from 16% y/y constant currency billings growth in Q2.

Box billings (Box Q3 earnings release)

The company notes that its top-of-the-line Enterprise Plus packages have seen strong traction since its introduction last year. Per CEO Aaron Levie’s prepared remarks on the Q3 earnings call:

As we’ve shared, Enterprise Plus, our multi-product Suites offering is a key strategy to increase the efficiency of our sales motion and to bring the full value of the Box Content Cloud to customers. Enterprise Plus brings the full suite of Box’s advanced product capabilities into a simple product bundle. And we’ve seen tremendous uptake from our go-to-market teams and customers.

We launched ePlus just over a year ago, and it has become our most successful suites launch to date. In Q3, Enterprise Plus comprised over 90% of our suite sales in our large deals. And suites represent 73% of our large deals, up from 63% just a year ago. And we are now seeing renewal rates of ePlus come in higher than our overall company renewal rates […]

We are pleased with our continued strong adoption of Enterprise Plus, as we know that when a customer adopts our multi-product offerings, we see greater total account value, higher net retention, higher gross margins and a more efficient sales process.”

The company also noted that its gross churn rate of 3% was lower than 5% last year, demonstrating the stickiness of the company’s product once installed.

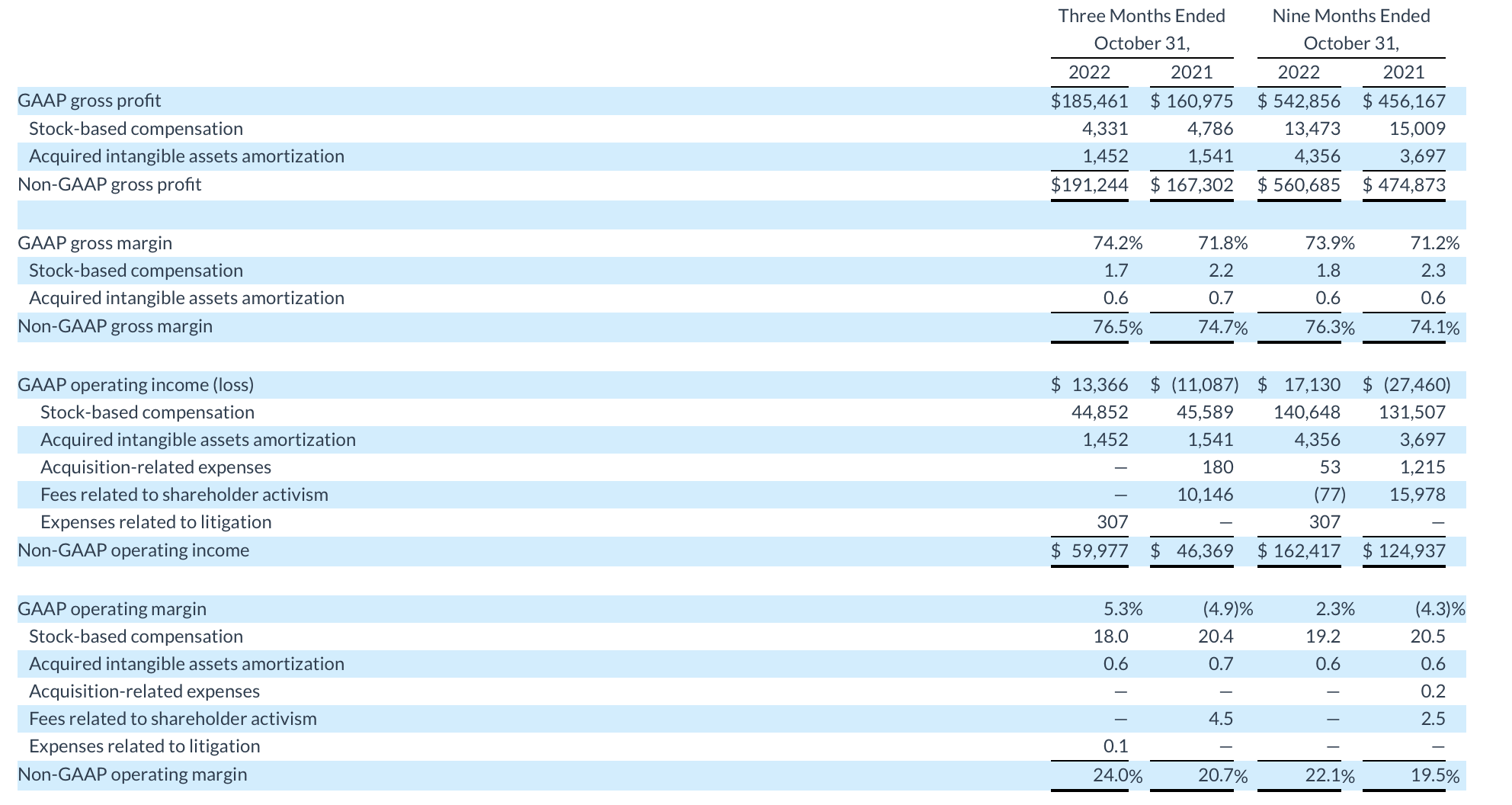

Box also excelled at delivering profitability gains. Pro forma gross margins rose 180bps y/y to 76.5%, driven by economies of scale on higher-value customers adopting Suites/Enterprise Plus plans, and cost benefits of Box now running fully on the public cloud.

Box margins (Box Q3 earnings release)

In turn, Box also boosted pro forma operating margins by 330bps to 24.0%, driven by additional sales and marketing efficiencies. Q3 represented a record quarter for operating margins for Box. The company also notes that it is on track to deliver “growth + FCF margin” of 37% this year, which is four points better than 33% in FY22 and showing nice progress toward the company’s goal of 45% by FY25.

Key takeaways

Box is a fantastic combination of sturdy growth, strong recurring revenue, consistent margin progress, and a modest valuation. Stay long here heading into 2023.

Disclosure: I/we have a beneficial long position in the shares of BOX either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.