Summary:

- Broadcom Inc. reported earnings after the close Thursday.

- AI revenue continues to drive top line and earnings growth.

- Best-in-class margins and cash flow make AVGO stock worthy of a Buy.

MF3d

Broadcom Inc. (NASDAQ:AVGO) shares jumped after hours on Thursday after the company reported fiscal fourth quarter and full-year earnings. I was yet again impressed by the company’s results as it turned in another impressive quarter driven by strength in the data center. Revenue and earnings growth remains robust, while cash flow continues to cover the dividend and offer room for further expansion. Despite a high valuation, this stock looks poised for further upward momentum.

In my last piece on AVGO, I recommended a Buy rating due to the company’s prime positioning in the market for AI infrastructure, best-in-class margins, healthy free cash flow, and the fast integration of the VMware acquisition. From a profitability standpoint, the growth in the data center (e.g., custom AI accelerators, Ethernet switches, optical transceivers, etc.) and VMware’s accretive contribution to earnings were the main financial drivers behind this recommendation. That article can be read here.

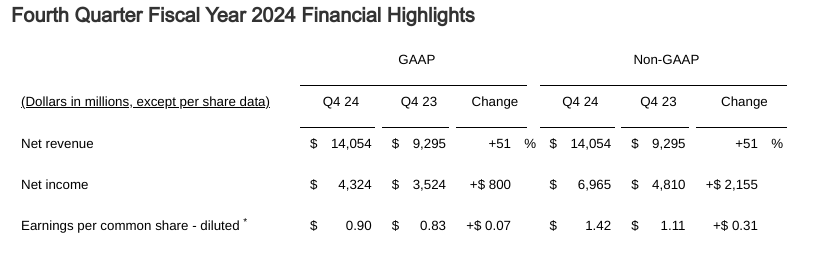

Let’s start with a quick recap of the Q4 2024 earnings results, starting with the financials:

Broadcom IR

The immediate thing that jumps out is that quarterly revenue and earnings growth have maintained course, when perhaps some investors had expected it to taper off somewhat after Nvidia (NVDA) reported a slower-than-expected growth curve. Revenue is up to $14.05 billion, up 51% YoY but also up 8% QoQ, indicating that demand is still rising and that the VMware acquisition isn’t masking organic growth, and earnings per share has achieved another record high.

Broadcom also reported $12.2 billion in AI revenue for FY2024, which exceeded previous guidance of $12 billion and was up 220% YoY, driven by ongoing strength in demand for custom AI accelerators and Ethernet switches. This was a major factor in free cash flow climbing to a whopping $5.5 billion, which is up 15% over Q3 and represents 39% of revenue, which is just an extremely impressive number. Speaking of impressive numbers, the company has again maintained a gross margin of close to 77%, translating much of the increase in revenue into income and cash flow down the income statement.

As I mentioned in my previous article, the addition of VMware has had an almost immediate windfall, as software revenue jumped from $2.8 billion pre-acquisition to more than $5.8 billion in Q4. With the segment boasting a gross margin around 90%, this is already paying off handsomely for Broadcom as well.

Finally, the company issued upbeat guidance for Q1 2025 as well. It expects $14.6 billion in revenue (+22% YoY/+4% QoQ) and $9.64 billion in EBITDA, which would be an increase of more than 6% YoY, and would be EPS of around $1.51 if we assume similar taxation and interest expense and use the company’s expected Q1 2025 share count. This would represent another record high and shows the company’s ability to maintain its best-in-class margins at these higher levels of revenue. Broadcom also announced it would be raising its dividend by 11% to $0.59 per share, which is in line with the company’s previous cadence. Based on the growth in free cash flow, Broadcom’s payout ratio has actually gone down to 0.50 even with the increase.

There have been some fears about Apple dependency after the company announced intentions to replace a Broadcom-supplied Wi-Fi + Bluetooth chip in its iPhone with an in-house chip instead. Estimates put Apple at around 20% of Broadcom’s total revenue, so initially this might appear like a cause for concern. However, just a couple of days ago, Broadcom and Apple (AAPL) announced a partnership to build AI accelerators for inferencing tasks as soon as 2026. This will likely more than make up for any lost revenue from the Wi-Fi + Bluetooth chip content in the iPhone.

My main point here is that Broadcom’s business is so diversified and the company maintains strength in so many areas that no one dependency should cause concern for investors or sink the stock in the case of a lost contract here or there.

Investor Takeaway

Broadcom’s earnings demonstrated more of what the market has come to expect over the last few quarters as AI-derived revenue ramps, margins remain elevated, and cash flow continues to more than cover the dividend, which is growing year after year. Despite fears over Apple reliance, I think the company remains well positioned in AI infrastructure and elsewhere.

I continue to see AVGO as a valuable long-term opportunity with an asymmetric risk-reward profile and savvy management that can target and integrate synergistic acquisition targets like VMware. Despite a valuation that is a bit rich, I think this stock is one to buy and hold for investors with a long time horizon. I am re-iterating a Buy rating following strong quarterly and full-year earnings.

Thanks for reading!

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AVGO either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.