Summary:

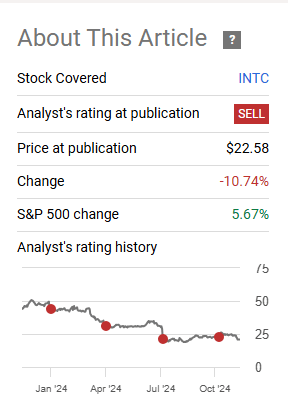

- We have maintained a “Sell” rating on Intel Corporation for some time, and it has worked out really well.

- Recent events suggest a possible Qualcomm buyout of INTC.

- This could present a real threat to the Intel bears and also create headaches for its arch nemesis.

- There are other reasons, as well, to turn less bearish on Intel, and we go over those in our verdict.

Robert Way

On our last coverage of Intel Corporation (NASDAQ:INTC), we were amused at the bullish enthusiasm over a bunch of mediocre numbers. Our dissection of those numbers suggested that the stock should head a lot lower.

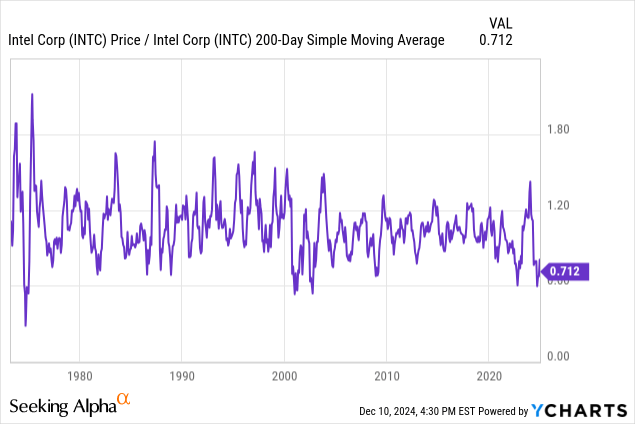

But if you simply use the 2009 and 2022 lows seen on this ratio and adjust for the cash burn (debt increase) over the next two years, we can see INTC drop another 40% from here. We maintain a “Sell” rating.

Source: Look For Big Downside In 2025 As Semiconductor Cycle Peaks.

In relation to a 40% drop over 2 years, we will certainly take an 11% drop over 1 month.

Seeking Alpha

But at this point, we have decided to upgrade the stock as the recent events seem to be pointing towards a buyout.

Will QUALCOMM Incorporated (QCOM) Take The Plunge?

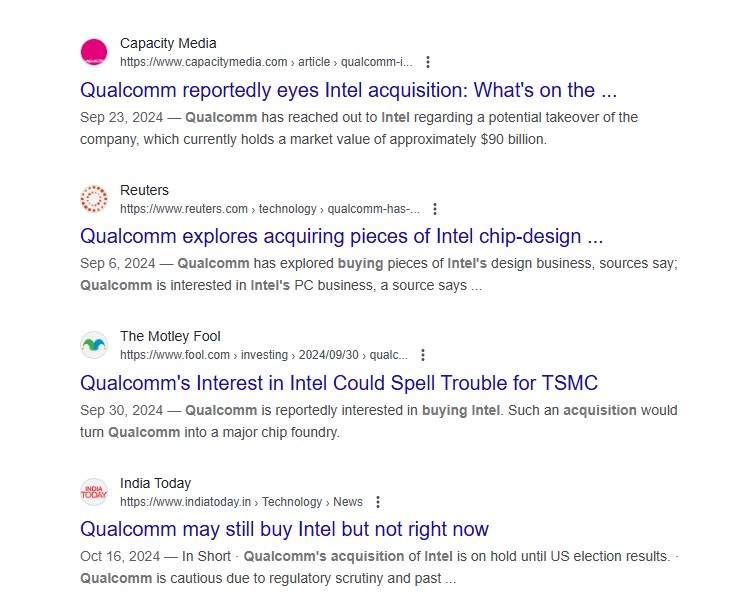

Rumors of QCOM potentially buying out INTC have been around for about 3 months now.

Google Search

Wall Street Journal confirmed this as well. We have not even mentioned this in any of our previous articles. Recent events, though, have made us believe that the risks of a buyout are a bit higher than what we would like. Here is our case.

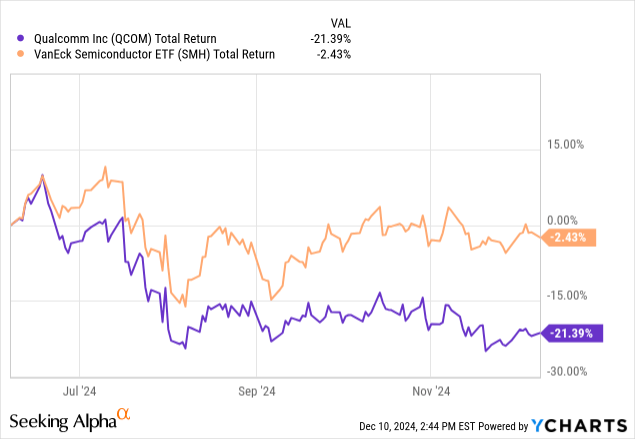

For starters, QCOM is acting incredibly weak relative to the VanEck Semiconductor ETF (SMH).

Almost always, this is due to disappointment in the earnings outlook. But in QCOM’s case, we can see that earnings estimates have held relatively steady, and recent results have been very good.

Seeking Alpha

The stock also appears cheap relative to the P/E multiples that it has sported over the cycle, and definitely appears cheap relative to some price-to-earnings and price-to-sales multiple seen on other stocks. We think the market is sniffing out a deal possibility and rightly punishing QCOM for this risk.

The other tell here for us was the exit of the CEO.

Effective Dec. 1, 2024, Intel Corporation CEO Pat Gelsinger has retired from the company and stepped down from the board of directors.

Intel has named two senior leaders, David Zinsner and Michelle Johnston Holthaus, as interim co-chief executive officers while the board of directors conducts a search for a new CEO. Zinsner is executive vice president and chief financial officer, and Holthaus has been appointed to the newly created position of CEO of Intel Products, a group that encompasses the company’s Client Computing Group (CCG), Data Center and AI Group (DCAI) and Network and Edge Group (NEX). Frank Yeary, independent chair of the board of Intel, will become interim executive chair during the period of transition. Intel Foundry’s leadership structure remains unchanged.

Source: INTC.

This is big. Gelsinger led the FAB transition. It was his baby, and getting out in such a time frame can mean one of two things. The company is looking to alter its strategy radically. This could mean sending the FAB part of the company in a different direction, perhaps with a new partner. INTC’s financials and credit rating have come under increasing strain as free cash flow is nowhere to be found and capex is drowning the company in debt. As we have said previously, a severe recession could send this company down to zero in the next 3 years. It is possible that the rest of the board has decided that this experiment has run its course.

The other alternative is that Pat Gelsinger was the biggest blockade to a QCOM takeover. This is speculation at this point, but it is likely the only other explanation for his departure after the company executed mass layoffs.

Why A QCOM Takeover Presents A Threat To AMD

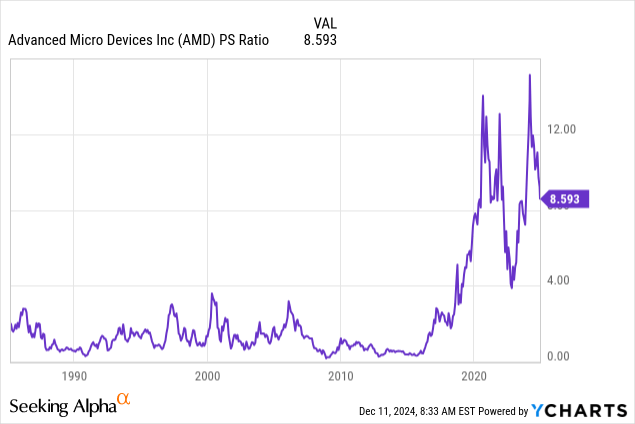

Advanced Micro Devices, Inc. (AMD) has also been beating the former giant INTC in the PC market via its cheaper chips. QCOM licenses GPU technology from AMD, which could help INTC in this arms race. QCOM has been trying to really improve this segment. Interestingly enough, ARM Holdings plc (ARM) is trying to pressure QCOM into paying more for its technology at the same time. The combination of QCOM and INTC could create a strong rival for AMD in the desktop and laptop markets. AMD is particularly vulnerable despite all the AI hoopla, AMD’s 2024 profits ($3.32 per share) will be about 14% lower than what they were in this four-quarter period in 2021 and 2022.

Seeking Alpha

Despite a negative 3-year growth rate in earnings, the stock still trades at 8.6X sales.

If AMD is forced to compete more vigorously, with lower margins, you can expect the stock to really tank.

Verdict

Getting back to INTC, at any point in a long or short thesis, the question should be the same.

What is my risk-reward ratio? We stuck with the INTC short thesis through some counterrallies as the fundamentals were poor, and the risk-reward was lucrative. As we get down to below $20.00, we see $5.00 of potential downside in the next year. Even though QCOM is said to have lost interest, we think this is still on the table. INTC could be easily bought out at $25.00 or even higher. So things are more balanced, and this is hardly a slam dunk case.

INTC is also now 29% below its 200-day moving average. It is hard not to look at that chart and see how many times it has rebounded sharply when it hit levels similar to this.

You can call them bear market rallies if you like, but they can be very painful for bears to hold through.

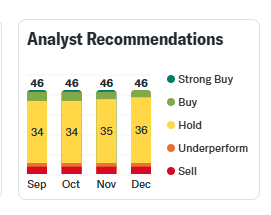

We have also read a few analyst reports from the major banks. For a community that is almost always bullish, they have thrown in the towel on INTC. This is a community that could see a meteor hurtling towards Earth and put out a report saying NVIDIA Corporation (NVDA) deserves an upgrade because their chips will be used in space missiles to blow up the meteor. So for them to go dark, it takes a lot. There are only 4 buy ratings (no strong buys) out of the 46.

Yahoo Finance-INTC

Contrast this to AMD, which cannot get the AI bump in its revenues to save its life and still earnings less than 2021-2022.

Yahoo Finance-AMD

All of this gets us to one point. We are now upgrading this to a “Hold” from a Sell. Those wishing to speculate on the QCOM buyout should consider using calls on INTC or puts on QCOM.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult a professional who knows their objectives and constraints. Our articles are not written for “buy and hold” investors.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Are you looking for Real Yields which reduce portfolio volatility?

Conservative Income Portfolio targets the best value stocks with the highest margins of safety. The volatility of these investments is further lowered using the best priced options. Our Enhanced Equity Income Solutions Portfolio is designed to reduce volatility while generating 7-9% yields.