Summary:

- Dell Technologies Inc. experienced strong top-line growth driven by AI infrastructure sales and the general compute refresh cycle, positioning it well for eFY26.

- Commercial devices offset the -18% decline in Consumer device sales. Enterprise sales are expected to improve in e2h26 as more AI workloads are done at the edge.

- Dell may realize strong top-line growth in eFY26 as a result of strong enterprise sales for its integrated infrastructure stacks.

- General compute servers & storage are expected to undergo their next refresh cycle, adding much needed margin accretive revenue into the product mix.

J Studios/DigitalVision via Getty Images

Dell Technologies Inc. (NYSE:DELL) realized strong top-line growth driven by enterprise AI infrastructure sales and the turn of the next general compute refresh cycle. With Storage and Commercial devices growing on a year-over-year basis in Q3 ’25 and modest optimism for enterprise refresh cycles, I have reason to believe that Dell is well-positioned for growth across all segments in eFY26 that may be margin accretive. Despite the optimism, I believe DELL shares are appropriately priced and will be downgrading my rating to a HOLD with a price target of $126.48/share at 8.48x eFY26 EV/aEBITDA.

You can read my previous coverage of Dell Technologies here:

Dell Technologies: Buy Into Earnings (Earnings Preview).

Dell Technologies Operations

Corporate Reports

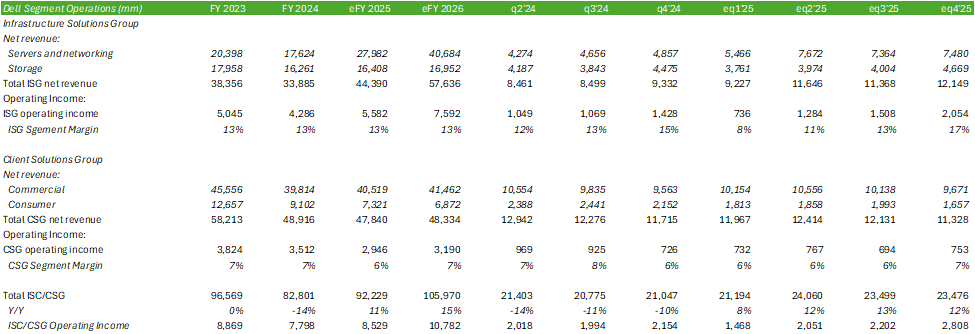

Dell Technologies reported mixed Q3 ’25 earnings results on November 26, 2024, with 13.27% growth for the Infrastructure Solutions Group [ISG] and a -1% decline in Client Solutions Group [CSG] revenue paired with an 11bps decline in adjusted EBITDA. Dell reported a miss in total revenue of $24,366M, -$343M below consensus estimates, and a strong EPS beat at $1.15/share, well above consensus estimates of $2.05/share.

Revenue in ISG was primarily driven by AI infrastructure, driving Server & Networking sales up 58% on a year-over-year basis in Q3 ’25. In CSG, commercial sales improved by 3% on a year-over-year basis, while consumer sales declined by 18% from the previous year. The silver lining for CSG is that consumer sales have improved for the last two quarters on a sequential basis.

Infrastructure Solutions Group [ISG]

ISG has been the primary revenue driver for Dell as growth for AI servers continues to accelerate. Order demand grew by 11% sequentially to $3.6b in Q3 ’25, driven by Tier 2 cloud services providers [CSPs] and enterprise customers. In the quarter, Dell shipped $2.9b of AI servers and grew its AI server backlog to $4.5b.

Accordingly, customers are making large purchases of the full infrastructure stack, including power management & distribution as well as cooling solutions. In q3’24, Dell launched its 21-inch Orv3 Integrated Rack 7000, a 480kW rack that has integrated cooling, power, and networking. This rack was designed to be scalable for deployment at large AI factories for AI training.

In addition to this, Dell released its AI-ready platforms specifically designed for the Dell IR7000. This includes the Dell PowerEdge XE9712 and the Dell PowerEdge M7725. The XE9712 will be the industry’s first enterprise-ready Nvidia (NVDA) GB200 NVL72 server rack that can be scaled to 72 Blackwell GPUs. The M7725 will support upwards of 27.000 Advanced Micro Devices (AMD) EPYC CPUs with direct-to-chip liquid cooling.

Dell realized double-digit growth in demand for general compute servers in Q3 ’24 on a year-over-year basis. Growth for these servers is primarily driven by improved unit sales and average selling prices as newer servers contain denser core counts, memory, and storage. Management suggested that the transition to the more efficient and denser 16G servers is the result of customers freeing up space for AI infrastructure. Accordingly, the 16G server has 2x the memory and storage when compared to the 15G server.

On the storage side, growth is trending with general compute server growth as the refresh cycle begins to ramp up. This can be seen in the segment’s 4% year-over-year growth rate and the last three quarters of sequential growth. Dell realized double-digit growth for its mid-level storage units, the PowerStore and PowerFlex products. PowerScale is the primary driver for storage growth given its capabilities of compatibility with unstructured data for AI capabilities.

Looking out to the end of eFY25 and eFY26, management remains optimistic in AI server growth as well as growth for general compute servers as IT departments undergo their next server refresh cycle. Management also anticipates a soft market for storage spend to remain relatively soft in the near term as IT department heads remain budget conscious. Growth in AI servers is expected to continue to increase, especially with the shipments of GB200 servers in eFY26.

In addition to this, Dell may realize strength in rack scale integration, providing the full infrastructure stack that includes the servers, networking equipment, and storage components as well as supporting infrastructure like cooling and power distribution & management.

Client Solutions Group [CSG]

CSG revenue declined by -1% on a year-over-year basis, driven by the large -18% decline in the Consumer subsegment. This decline was offset by Commercial growing by 3% on a year-over-year basis as enterprise customers begin their refresh cycles. Accordingly, upgrades may fall in line with new AI PCs in CY1h25.

Given the tight budgetary constraints across IT departments, management is anticipating PC sales to remain relatively soft in the near-term. Looking further out to eFY26, endpoint sales may realize strength as a result of newer AI PC models being released to enhance edge workloads.

Dell Technologies Financial Position

Corporate Reports

Dell realized pressure at the margins as a result of product mix, as AI server growth comes with competitive pricing. Despite gross margin compression, Dell improved operating costs by leveraging AI to improve business processes, expanding the adjusted operating margin by 20bps to 9.02%.

Looking out to Q4 ’25, I’m forecasting Dell to generate $25b in net revenue, with an adjusted EPS of $2.89/share. I’m forecasting Dell to realize modest margin improvements going into the end of eFY25 as the firm realizes higher growth for margin-accretive products, such as general compute servers and storage.

I’m forecasting Commercial devices to continue to trend upwards as more enterprises seek to leverage AI applications with more workloads being done at the edge. Furthermore, I’m also forecasting Consumer devices to continue declining as a result of tighter budgetary constraints and inflationary pressures on discretionary spending.

Looking out to eFY26, I’m forecasting growth to continue at a high level for ISG driven by AI infrastructure growth, including growth for storage. Management suggested that CSG will realize tailwinds in e2h26 as the beginning of the PC refresh cycle takes form.

On the balance sheet, Dell increased its days inventories to 33.43 days in q3’25, up from 17.83 days in the year-ago quarter. Management noted that this was the result of stocking up for AI order demand. Given the growth in inventory levels as a result of AI infrastructure, I believe that working capital may add some headwinds to free cash flow generation in Q4 ’25 if the inventory build persists.

Corporate Reports

Risks Related To Dell Technologies

Bull Case

Dell is entering into a period of strong tailwinds as refresh cycles in higher margin products, including general compute infrastructure, storage, and devices, takes form. Though I anticipate Consumer device sales to remain a drag on growth, I believe growth in ISG will more than offset this.

Bear Case

Despite management’s efforts to bolster operating margins, the strong growth in AI infrastructure inherently puts a drag on margins as the industry remains highly competitive. CSG has been relatively flat for the Commercial subsegment and may remain so if IT budgets remain tight going into eFY26. Consumer demand may also remain suppressed as a result of tight budgetary constraints as consumers face a higher cost of living.

Valuation & Shareholder Value

Corporate Reports

DELL shares currently trade relatively in line with its IT infrastructure peers, Hewlett Packard Enterprise (HPE) and Super Micro Computer (SMCI) at 12.12x EV/EBITDA on an unadjusted basis.

Seeking Alpha

In Q3 ’25, Dell repurchased 3.7mm shares for $398mm. I estimate that Dell has $5.3b remaining under its current share repurchase authorization.

Using an internal valuation model for DELL shares based on my adjusted EBITDA forecast for eFY26 and the stock’s historical trading premium, I believe shares are appropriately priced. I will be reducing my rating to a HOLD with a price target of $126.48/share at 8.48x eFY26 EV/aEBITDA.

Corporate Reports

Analyst’s Disclosure: I/we have a beneficial long position in the shares of DELL, HPE, AMD either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.