Summary:

- GoDaddy’s stock surged 100% recently but is now overvalued and poised for a contraction; my valuation model projects an 8.3% enterprise value CAGR over five years, justifying a Hold rating.

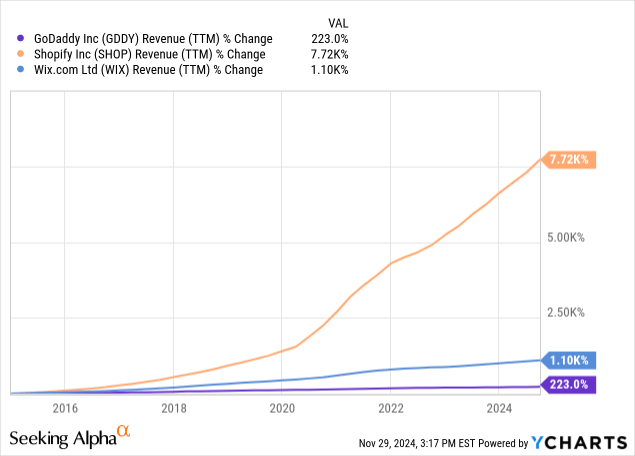

- Competitive threats from Shopify and Wix have led to a 1.4% customer decline; Shopify’s superior e-commerce platform pressures GoDaddy’s margins, necessitating heavy investment to stay competitive.

- GoDaddy does not offer exceptional medium-term return prospects; readers may find better long-term CAGRs from Shopify.

Delmaine Donson/E+ via Getty Images

GoDaddy (NYSE:GDDY) has recently delivered an exceptional price return of over 100% in a year, but this has led to somewhat of an overvaluation. Indeed, the company was undervalued prior to this, but now it is positioned for a potential near-term contraction.

Even without such a contraction, my valuation model indicates only a moderate enterprise value CAGR of 8.3% over the next five years. Therefore, my rating is a Hold. My outlook is further reinforced by the competitive threat from Shopify, which, I believe, will continue to pressure GoDaddy’s margins in the medium to long term.

Operations & Financials

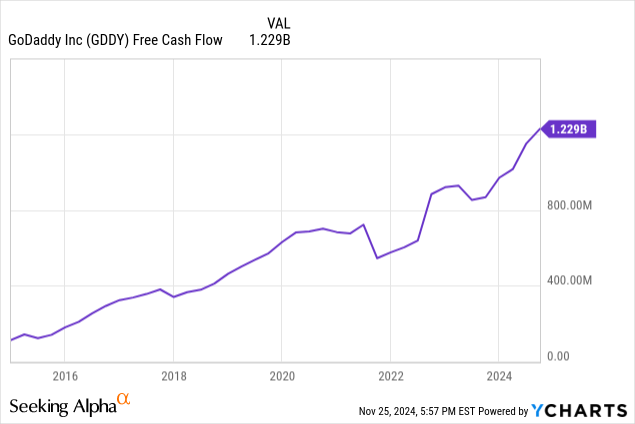

GoDaddy is a leading provider of internet services for small businesses, with operations split between its stable Core Platform (domains, hosting, and security) and its high-growth Applications & Commerce segment (e-commerce, payments, and marketing tools). Applications & Commerce has become its growth engine, with 16% revenue growth in Q3 2024 and strong adoption of bundled solutions. Management prioritizes shareholder returns, reducing outstanding shares by 23% since 2022 through aggressive buybacks, supported by its robust free cash flow. However, the company is facing a slight decline in its customer base (-1.4% year-over-year in Q3 2024) amid competitive pressures from Wix (WIX) and Shopify (SHOP). The company had a remarkably strong quarter in net income generation, up 45% year-over-year, resulting in a net income margin of 17%—this has undoubtedly supported the stock’s valuation expansion recently.

GoDaddy has raised its revenue expectations to a range of $4.545 billion to $4.565 billion for the full year 2024, indicating a 7% growth at the midpoint compared to the previous year. For the fourth quarter, it expects revenue between $1.165 billion and $1.185 billion (also a 7% year-over-year growth at the midpoint), with Applications & Commerce revenue growth expected in the mid-teens and Core revenue growth in the low single digits. This shows a moderately robust near-term outlook, but it still reveals pressure on the company’s Core segment, which is problematic for the long-term thesis amid competitive threats.

The company is focusing on higher-margin products such as productivity apps and website subscriptions—a strategic shift aiming to improve gross margins and reduce reliance on less profitable core domain services. The global rollout of its AI-powered GoDaddy Airo experience is expected to enhance user engagement and improve monetization gateways. Additionally, the company is now offering AI-powered digital marketing tools to integrate SEO, social media, and email marketing into a unified platform. However, the core domain services remain less profitable, which could potentially pressure its overall margins if not offset by the growth of its higher-margin products.

Moreover, management has decided to focus more on emerging markets where there is a growing demand for online services. India is a critical market for GoDaddy, being the first international market where the company established an office. It remains one of the largest markets for GoDaddy International. Beyond India, GoDaddy is expanding its reach to over 150 markets worldwide, including Africa, Asia, Latin America, and North America. Emerging markets account for approximately 50% of its new international customers, contributing around $400 million in revenue. This shows a robust long-term strategy and expansive market for management to capture and consolidate, and I think GoDaddy is quite well-positioned in this regard for sustainable growth.

GoDaddy competes with several well-established companies such as Namecheap, Bluehost (owned by Newfold Digital), Google (GOOGL) (GOOG) domains, and others. Newer platforms like Nexcess and A2 Hosting provide specialized services that can appeal to specific customer segments, such as those needing high-performance hosting for WordPress or e-commerce sites. On that note, Shopify provides probably the largest risk to GoDaddy expanding successfully through long-term e-commerce growth—I will analyze this more in my risks section below.

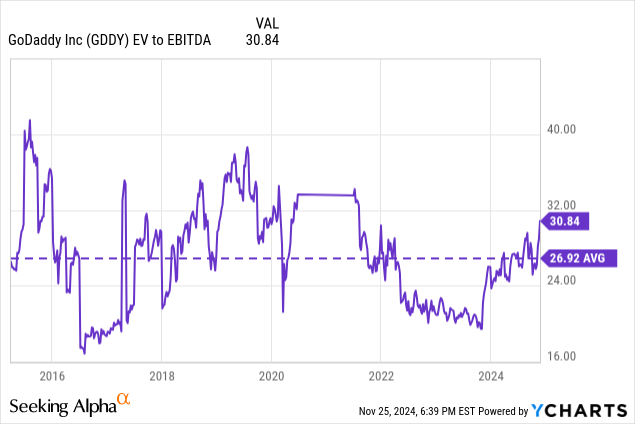

Valuation

|

TTM Revenue |

$4.48 billion |

|

November 2029 Revenue Estimate |

$6.75 billion |

|

November 2029 EBITDA Margin Estimate |

25% |

|

November 2029 EBITDA Estimate |

$1.69 billion |

|

EV-to-EBITDA Terminal Multiple |

27 |

|

November 2029 Enterprise Value Estimate |

$45.63 billion |

|

Current Enterprise Value |

$30.66 billion |

|

Five-Year Enterprise Value CAGR |

8.3% |

|

Weighted Average Cost of Capital |

10.2% |

|

Discounted Implied Current Intrinsic Enterprise Value |

$28.08 billion |

|

Margin of Safety |

-8.5% |

Guidelines for inputs:

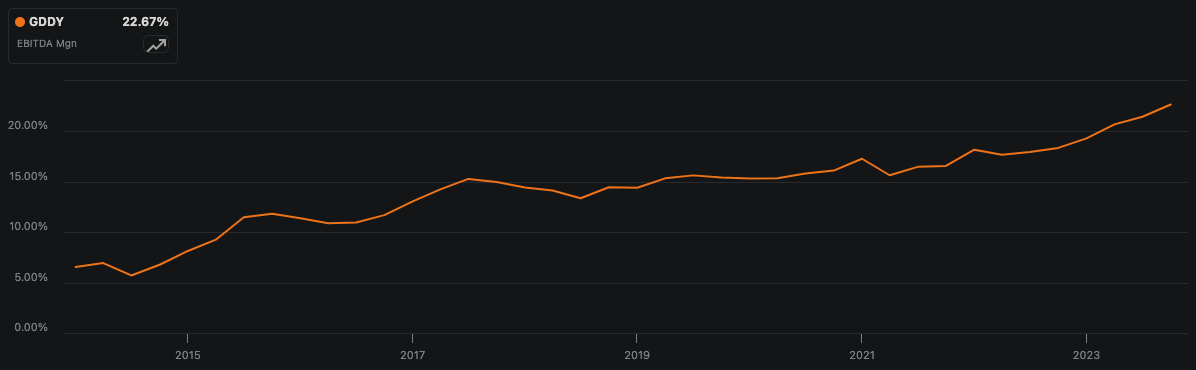

GoDaddy 10-Year EBITDA Margin (Author, Using Seeking Alpha)

- GoDaddy’s weighted average cost of capital is 10.2%, with an equity weight of 87.59% and a debt weight of 12.41%. Equity costs 11.06%, while debt costs 4.17% after tax.

My valuation model, which takes into account my own estimates, shows a moderate overvaluation of 8.5% and indicates that the stock is prone to near-term contraction. Even disregarding this potential contraction, the five-year enterprise value CAGR will likely be just 8.3%.

Board

GoDaddy has a robust board, including Aman Bhutani, GoDaddy’s CEO and board member since 2019; Graham Smith, the former CFO of Salesforce (CRM); Leah Sweet, a former PayPal (PYPL) executive; and Sigal Zarmi experienced in digital transformation from her tenure at Morgan Stanley (MS). Such a well-experienced board provides security to the medium-term investment thesis, but such guidance may not be enough to mitigate the long-term competitive threat from Shopify.

Shopify Risk

Shopify is consolidating its position aggressively, challenging GoDaddy by fundamentally altering the customer acquisition funnel and redefining the competitive landscape. Historically, GoDaddy relied on domain registration as the entry point for small businesses, upselling higher-margin services like hosting, email, and website building. However, Shopify has flipped this model by positioning itself as the go-to platform for entrepreneurs who prioritize e-commerce functionality first, such as setting up a store and transacting online, with domain registration becoming secondary or even unnecessary. This shift erodes GoDaddy’s control over the top of the funnel, reducing its ability to cross-sell ancillary services that drive customer lifetime value and profitability.

In addition, GoDaddy’s e-commerce capabilities are much less sophisticated than Shopify’s, with limited customization options and fewer built-in tools for enterprise-level needs. Therefore, GoDaddy may be left to compete in the lower-value DIY segment while Shopify dominates the higher-value customers.

Shopify’s dominance is also likely to compress GoDaddy’s gross margin further—over the past five years, its gross margin has declined in large part due to competition from platforms like Shopify and Wix. Given Shopify’s ongoing dominance, GoDaddy’s ability to grow its annualized recurring revenue from add-ons like hosting and email could be materially impaired. Therefore, GoDaddy likely needs to invest heavily in its innovation and technology to remain competitive moving forward, and this could put pressure on its EBITDA margins in the next five years, worsening the negative margin of safety indicated in my valuation model.

Conclusion: Hold

Even in an optimistic, conservative valuation model, GoDaddy is only likely to deliver an enterprise CAGR of approximately 8.5% over the next five years. This is the primary reason why my rating is a Hold. However, looking longer-term, the risks with the competitive threat from Shopify are a real concern, and I expect that the investment GoDaddy will have to make to remain competitive will open up periods of margin instability and valuation volatility in the medium to long term.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of GOOGL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.