Summary:

- The Walt Disney Company’s repayment of some debt indicates a cautious optimism for the future.

- The retention of a decent cash balance indicates some hesitancy of future prospects until the free cash flow starts rolling in again.

- Many parts of Walt Disney’s business will return to pre-Covid levels of activity.

- Parks and linear networks are the profit bright spots.

- Disney movies need to return to pre-pandemic levels. Meanwhile, losses will decline at the streaming business.

JHVEPhoto/iStock Editorial via Getty Images

The Walt Disney Company (NYSE:DIS) quarterly earnings report is usually a good pep talk, just like most quarterly reviews. But management’s actual view of things is best demonstrated by management actions. Right now, those actions appear to point towards a cautiously optimistic future as we determine how the Federal Reserve conducts its current asset deflation project.

Debt Moves

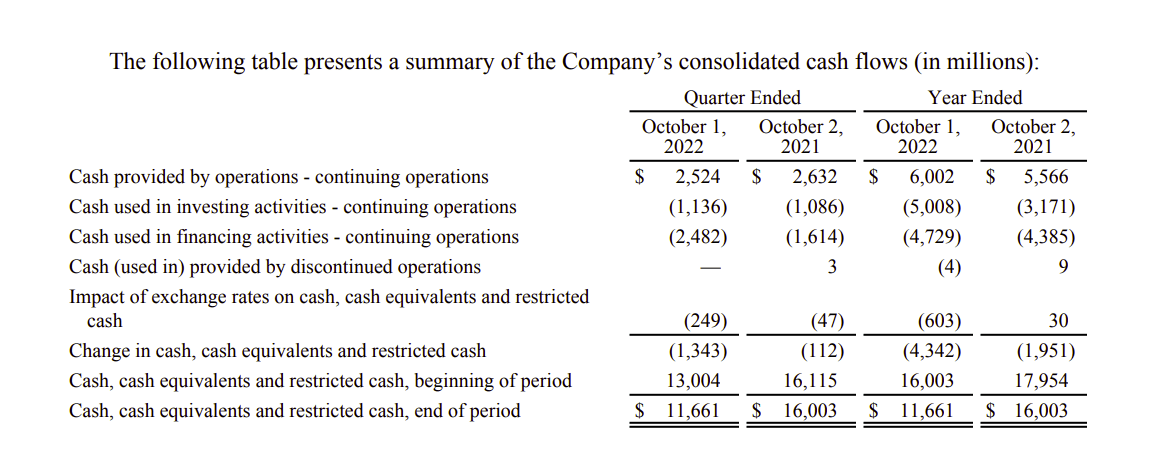

Disney’s management began repaying some of the debt that enabled them to keep a large cash balance outstanding. The large cash balance was sort of an insurance plan against the worst possible outcome during the pandemic. Therefore, repayment of some of the debt before the free cash flow really begins means that management sees some improvement this year. But management does not see enough improvement to repay more. Evidently, management still thinks there could be some challenges ahead. So, the cash balance kept on hand was on the large size.

Disney Summary Of The Cash Flow Statement Fourth Quarter Fiscal Year 2022 (Disney Fourth Quarter 2022, Earnings Press Release)

Total borrowings, including the current portion, dropped from about $54 million to $48 million. That approximate drop in debt accounts really for the change in the cash balance from the previous fiscal year to the current. It also indicates a cautious move on the part of management to not keep as much cash on hand. Had they thought they needed the cash, they would have inevitably found a way to “roll-over” the current debt to delay repayments.

Parks

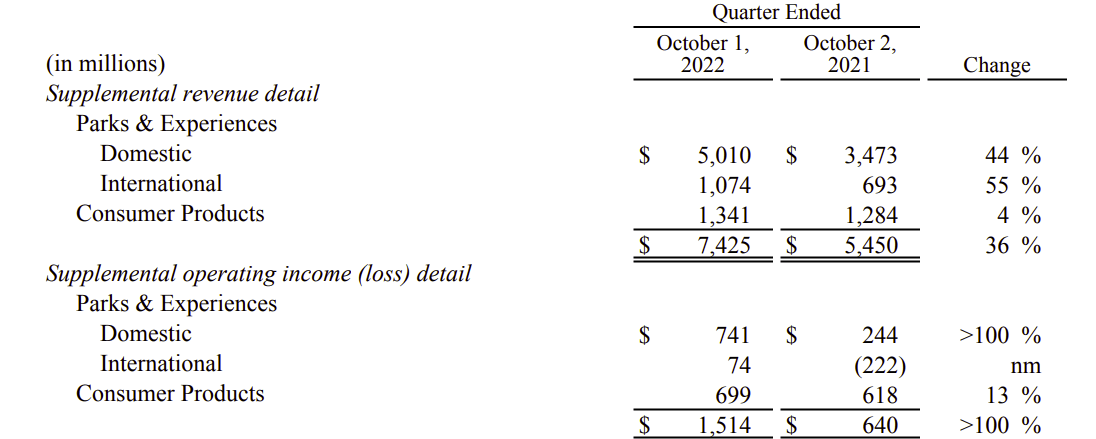

Some of the cautious optimism is due to Disney’s parks. Except for China, the parks are open and doing a pretty good business. Management was even able to raise some prices at the parks this fiscal year.

Disney Fourth Quarter Summary Of Parks & Experiences (Disney Fourth Quarter 2022, Earnings Press Release)

This part of The Walt Disney Company spent the year basically returning to normal. By the end of the fiscal year, most of this part of the company was back to normal. It is very likely that the operating income of this area will improve some more as we continue to move away from the necessary moves made for covid.

Linear Networks

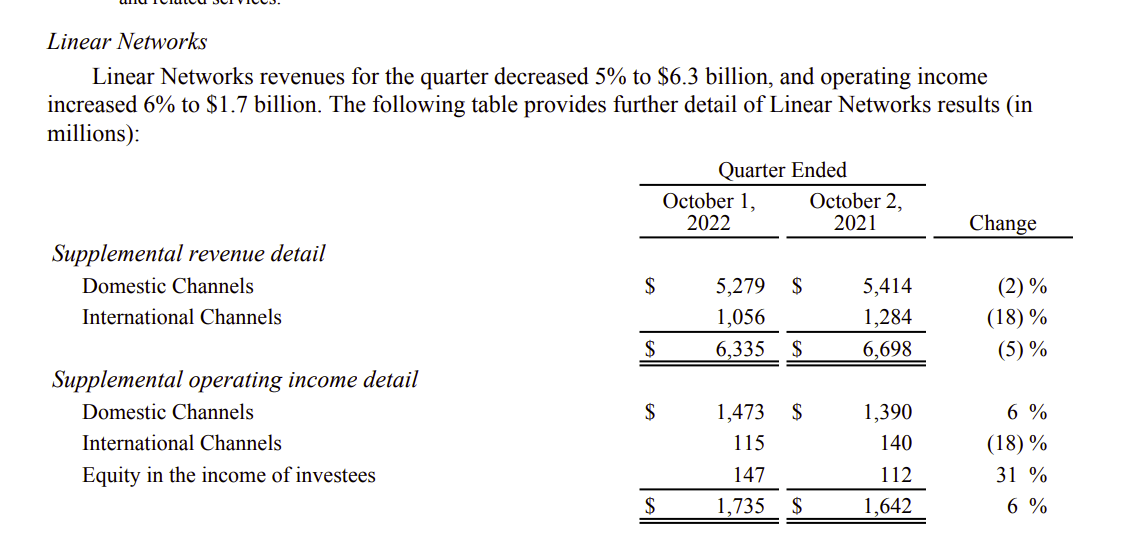

This was another bright spot and a reason to continue to be optimistic about the future.

Disney Financial Summary Of Linear Networks Results Fourth Quarter 2022 (Disney Earnings Press Release Fourth Quarter 2022)

The profitability held up well here during covid (relatively speaking). If anything, people were stuck at home to watch more television. So, once people can get out of the house, the fact that this area was able to increase profits at all is really kind of amazing.

This is an area that is likely to predictably decline in the future. My own feeling is that this group of businesses is very likely to head to streaming in the future, along with “everything else.”

Cable in many ways has an attractive package. It just has to deliver that package the “new way” through streaming. I personally believe that there will be a way found to do that while remaining probably more than competitive with some of the streaming pioneers.

I already stream episodes of shows that I missed and can do that for a while. That is really not very different from the offerings of Netflix (NFLX). All the Linear Networks need to do now is put the whole thing into streaming. I actually watched the election results through live-streaming, and in fact, my cable channels come through streaming. I suspect that linear will change to meet the competition. Because of this, I do not see linear going away. But I do see the business changing considerably.

Direct To Consumer

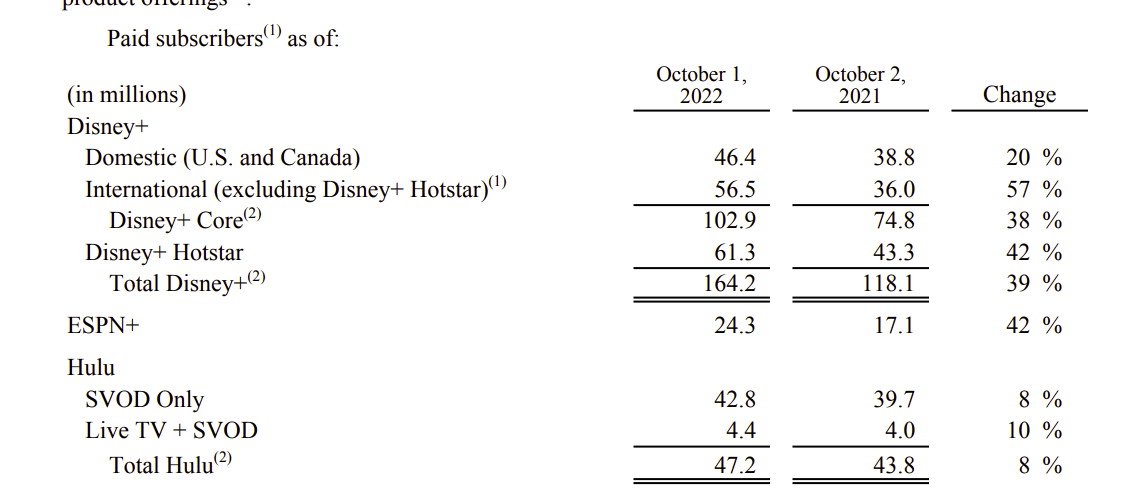

This area of Disney is where a whole lot of caution prevails.

Disney Presentation Of Streaming Subscriber Totals Comparison (Disney Earnings Press Release Fourth Quarter 2022)

The subscription services have focused upon growth in the past. That emphasis is now switching to lower losses with profits in the future. The low visibility comes from economic softness brought about by the rising interest rates. Advertising plays a role here and with Linear Networks. It is going to play a bigger role with the rollout of Ad-free and Ad services.

This business has been built quickly. So, the company is warning of some churn in the first quarter as Disney begins to raise rates and examine what it takes to make streaming profitable. Management has a plan that will likely unfold as the market reacts to the company’s goal of making a profit in this area.

Movies

The company is getting back to normal with theatrical releases. This takes time because management often needs to plan a movie approximately 2 years in advance. Covid really threw a monkey wrench into this area of the business.

Management did release some movies this year. But it clearly was not a full schedule. Movies in and of themselves are their own profit center because Disney is probably more dependent upon large successes than other studios due to the many franchises that management has exploited successfully over the years.

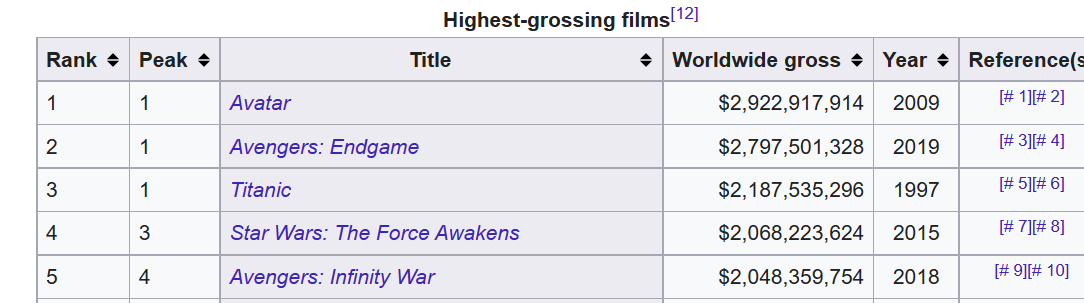

Top Grossing Movies Of All Time (Wikipedia List December 28, 2022.)

(Note: Wikipedia got this list from industry sources like “Box Office Mojo.”)

Getting the movie business back to normal is a huge issue for Disney. As shown above, Disney is one of the most successful and consistent hit moviemakers in the industry. As shown above, Disney has four of the top five movies. The latest release is the Avatar sequel, and it passed the $1 billion mark in only two weeks. This year should feature more releases than last year. Therefore, there is likely to be far more profits from this part of the company.

The success here also affects things like licensing clothing (along with the sales obtained as a result of that licensing).

Once the movie releases return to normal, an occasional bust does not have the impact it does now during the ramping-up period. Now, more money is going into making future movies than is likely to come back from the few hits released. That is likely to change now that theaters are largely back to normal and are looking to recover from the effects of covid as well.

The Future

This next fiscal year should easily be more profitable than was the current year. This recently completed fiscal year saw the ramp-up of the parks, the restarting of cruises, and the acceleration of the movie schedule toward pre-pandemic levels.

The covid pandemic interrupted a lot of businesses, including this one. But this management also kept the company profitable during those challenges. Not many companies can say that.

The coming fiscal year will be the first time since before the pandemic that things will largely return to normal. There still could be an occasional setback. But for the most part, the public and business is ready to return to the pre-pandemic days, even if the pandemic is not yet done with us. That should allow profits to largely return to previous levels.

Disney also has the acquisition from Fox that it has never really had the chance to properly exploit. That will also happen in the future and should be the source of additional profits and some growth in earnings.

Obviously, Disney management has cautiously kept a decent cash balance until the free cash flow begins to roll in. That is likely to happen in the coming fiscal year. When it does, it should lead to a pretty prompt deleveraging.

The market has its doubts because it is firmly focused on a recession. But this company has been fairly recession resistant for a very long time. Some parts of the company like the parks and the cruise ships are very sensitive to the economy. But other parts like Linear and Movies have a big resistance to economic downturns. Compared to other entertainment sectors, this is a remarkably performing business throughout the economic cycle.

The Walt Disney Company management has a lot to do in the future. Most of what needs to be done will result in considerably improved profitability.

Disclosure: I/we have a beneficial long position in the shares of DIS either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Disclaimer: I am not an investment advisor, and this article is not meant to be a recommendation of the purchase or sale of stock. Investors are advised to review all company documents and press releases to see if the company fits their own investment qualifications.

I analyze oil and gas companies, related companies, and Disney in my service, Oil & Gas Value Research, where I look for undervalued names in the oil and gas space. I break down everything you need to know about these companies — the balance sheet, competitive position and development prospects. This article is an example of what I do. But for Oil & Gas Value Research members, they get it first and they get analysis on some companies that is not published on the free site. Interested? Sign up here for a free two-week trial.