Summary:

- Merck’s Keytruda drug has shown promising results in treating bowel cancer, according to Germany’s largest newspaper.

- Merck has significantly increased its oncology portfolio, with Keytruda achieving nine U.S. approvals in earlier-stage cancers.

- The company’s phase III trials targeting earlier-stage cancers have shown impressive outcomes, including a reduction in the risk of death for patients with lung and renal cell cancers.

- It also has a highly favorable growth outlook and an attractive dividend growth profile.

Nudphon Phuengsuwan

Introduction

I usually spend my mornings browsing various news outlets. This was part of a prior job where I provided daily macro and geopolitical newsletters for both private and institutional clients.

This includes American, German, French, Italian, and newspapers from other regions. I use translation for most of these (except English, Dutch, and German languages).

I mainly do this to get a good overview of what is happening across the world and how this could impact the stocks that I own and discuss on Seeking Alpha.

It’s also a case of “old habits die hard.”

The reason I’m bringing this up is because BILD, Germany’s largest newspaper, ran a fascinating headline on June 5 (translated): “This drug can “melt away” bowel cancer.“

The drug is Keytruda, the biggest blockbuster drug from healthcare giant Merck & Co. (NYSE:MRK), a healthcare company I started covering last year.

While I knew about Merck way before I started covering it, I just didn’t care until 4Q23, when I pushed myself to dig deeper.

Although MRK has returned less than 7% annually since January 2004 (which is the reason why I just didn’t care about it), I have started to really like this company, as it is making massive progress in major programs like oncology, positioning itself to aggressively grow its earnings, while helping millions of people with serious health conditions.

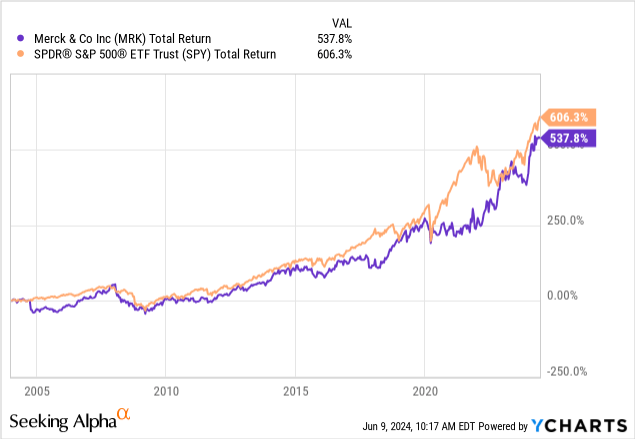

My most recent article on this company was written on February 29, when I called it “A High-Conviction Investment For Long-Term Growth.”

Since then, shares have returned 3%, slightly lagging the S&P 500’s 5% return.

In this article, I’ll update my thesis using the latest developments, which include major updates on its oncology programs.

So, let’s get to it!

Innovation-Driven Growth

Earlier this month, Merck presented at the American Society of Clinical Oncology (“ASCO”) annual meeting.

During this event, the company revealed a lot about its current products, pipeline, and research to address important financial needs.

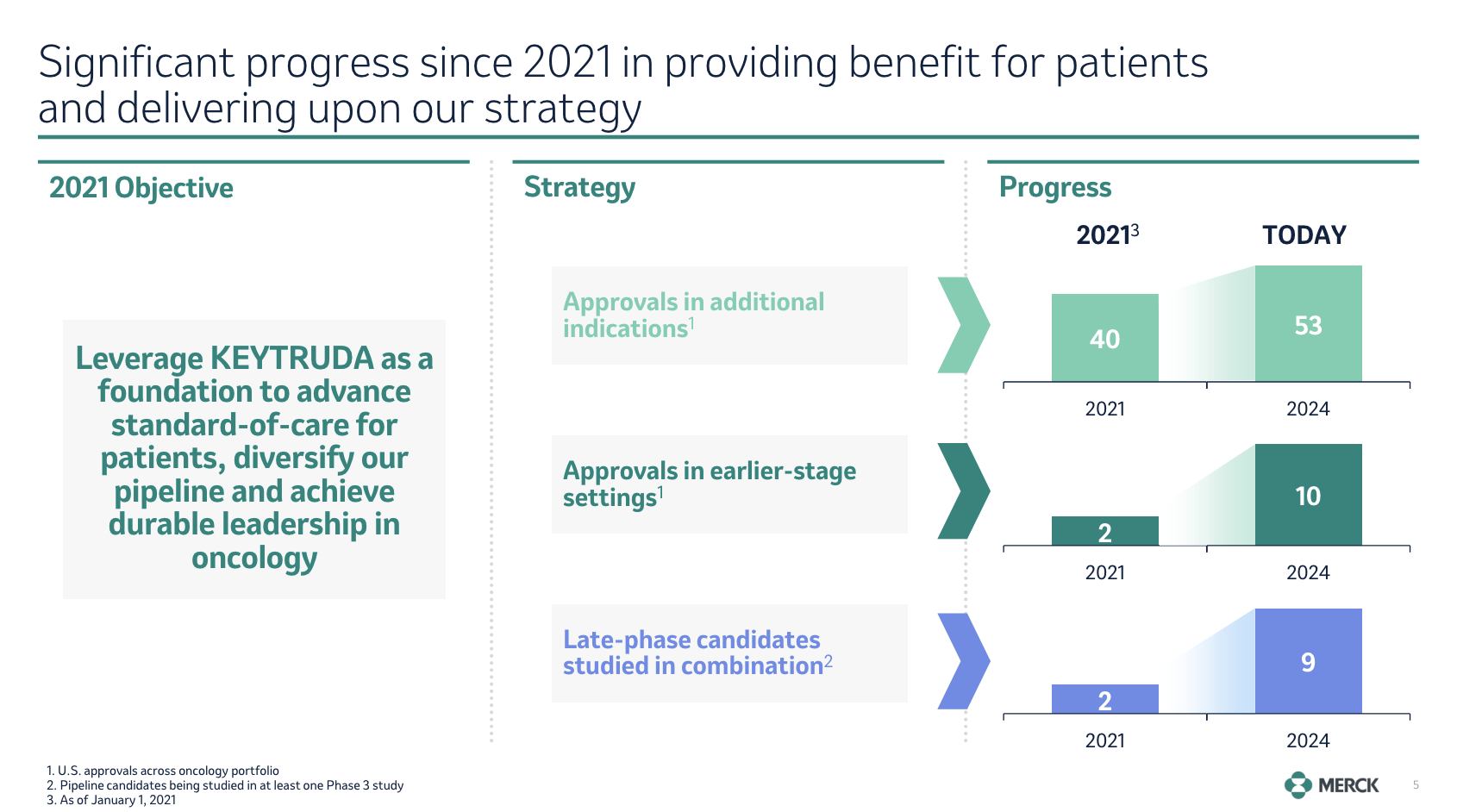

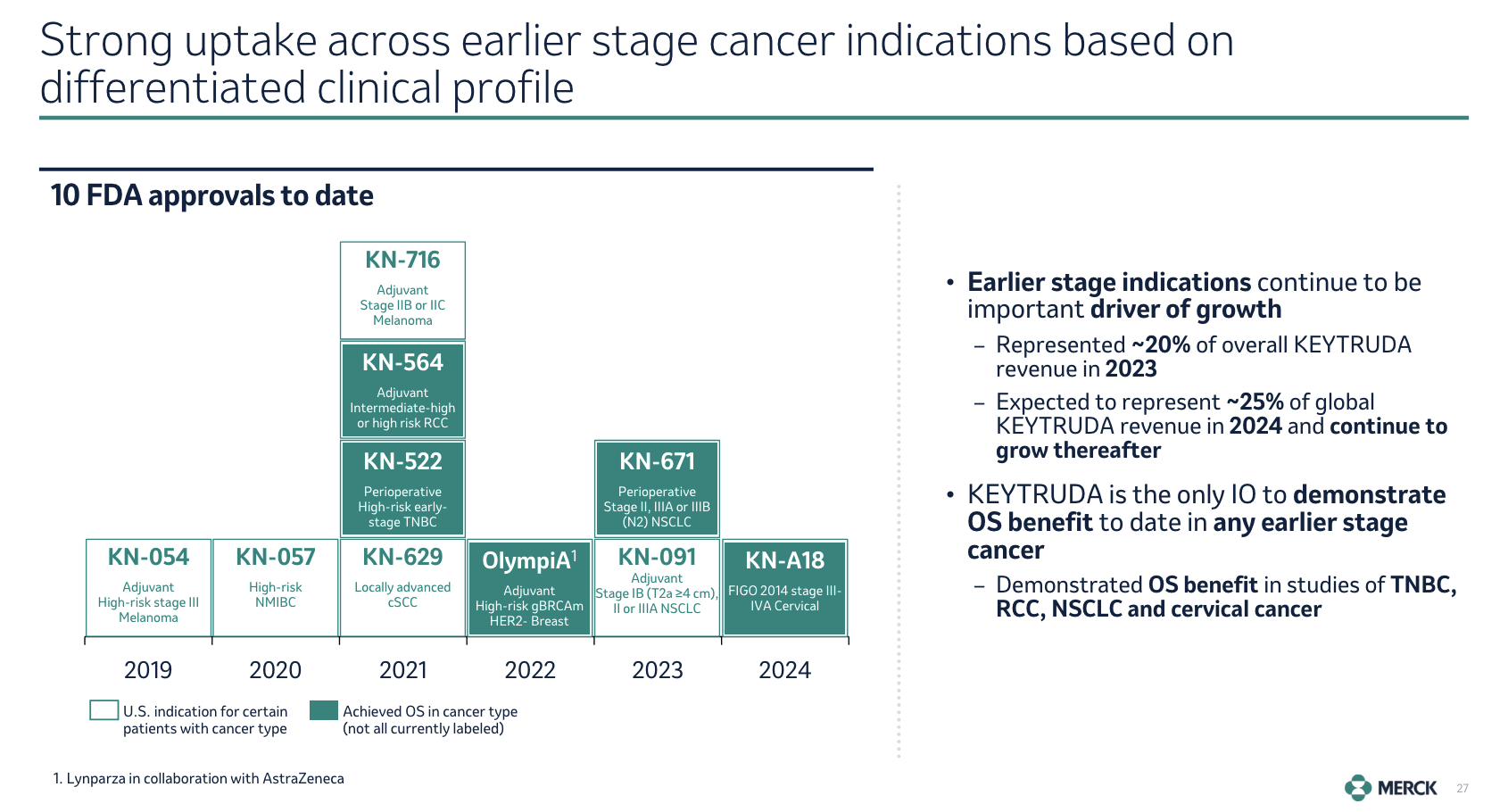

For example, since 2021, it has significantly increased its oncology portfolio, boosting the number of approved indications from 40 to 53 and the number of approvals in earlier-stage cancers from 2 to 10.

Merck & Co

Even more impressive, and with regard to my introduction, KEYTRUDA alone has achieved nine U.S. approvals in earlier-stage cancers.

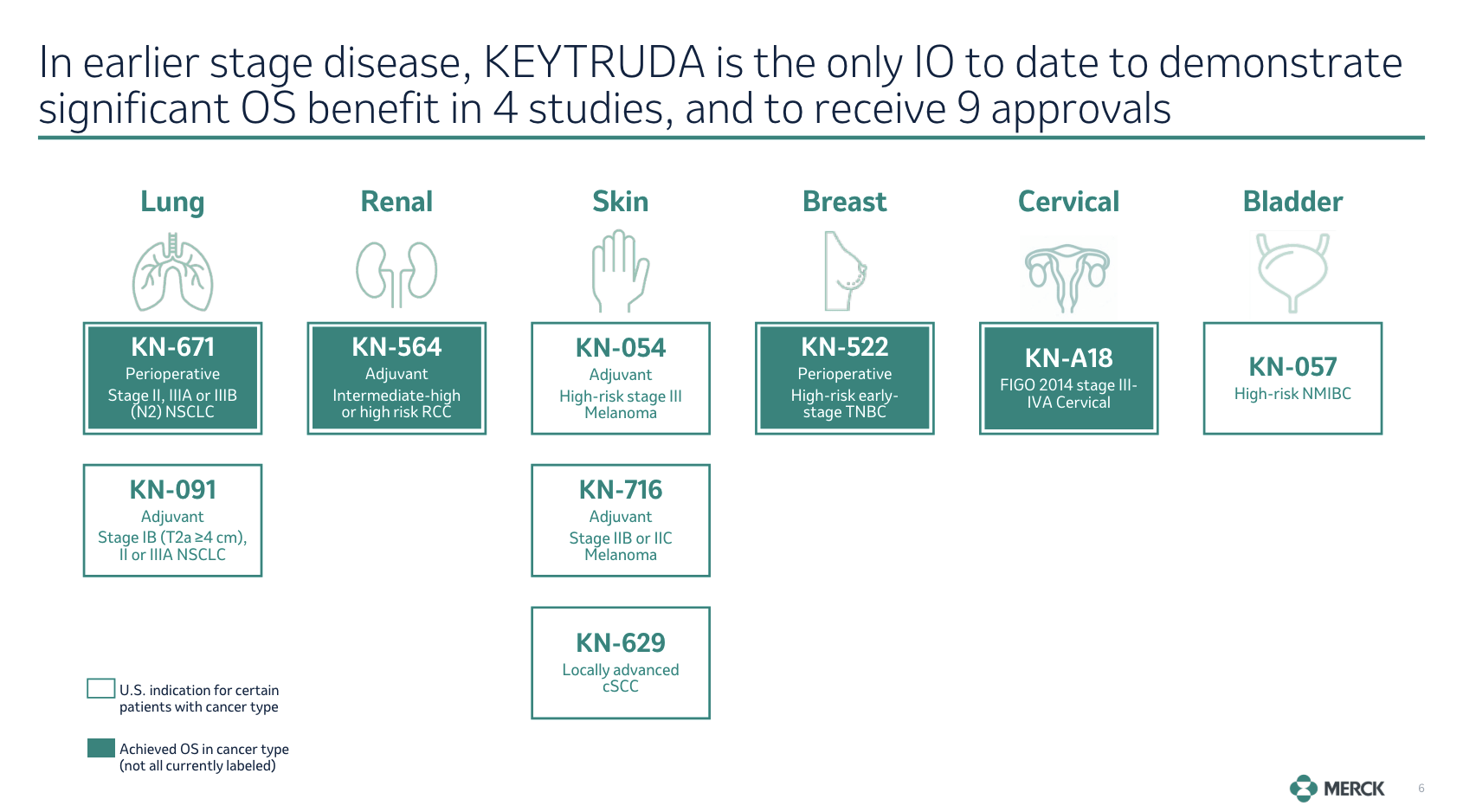

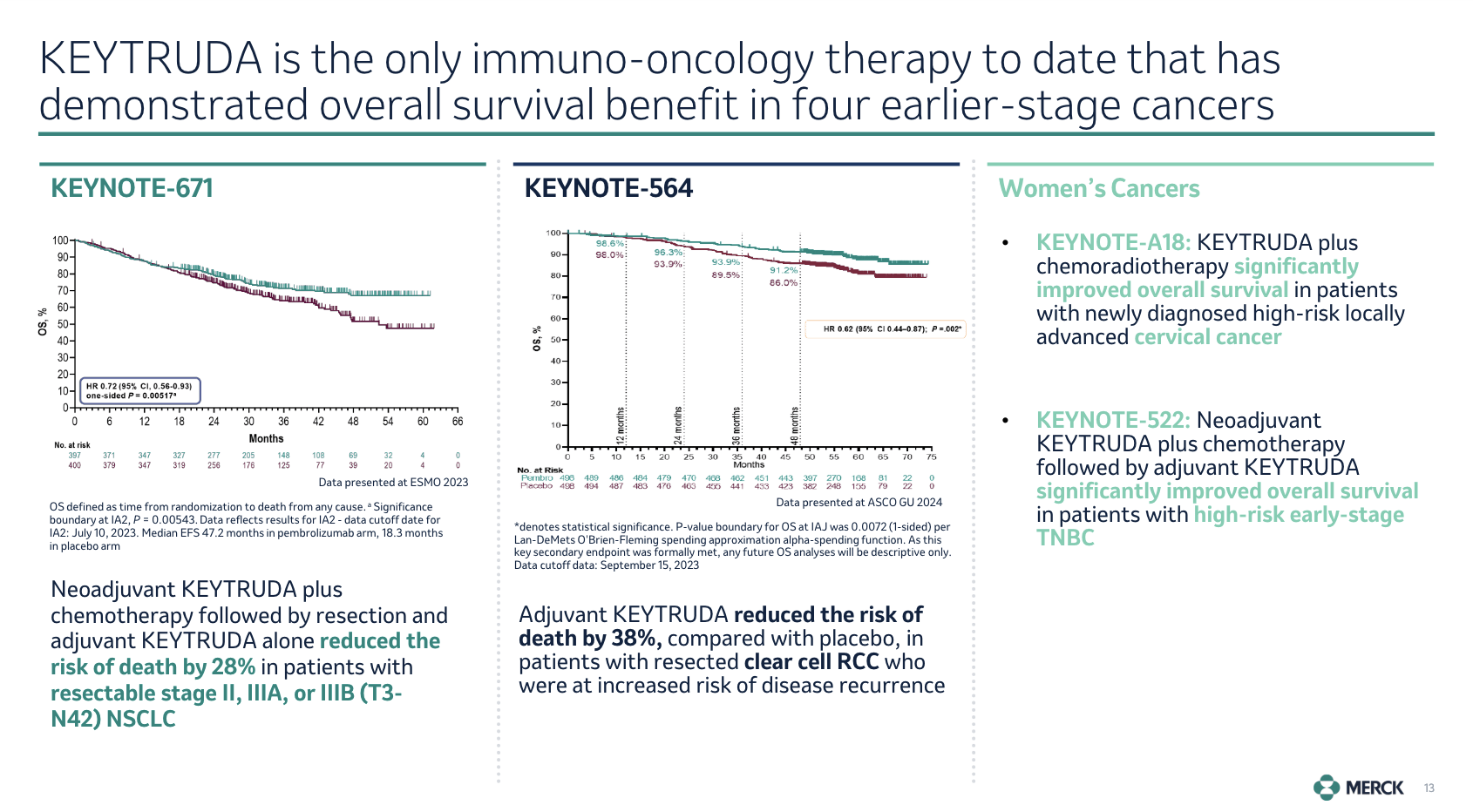

It is also the only PD-1/PD-L1 therapy that has shown an overall survival (“OS”) benefit in multiple tumor types, including lung, renal, breast, and cervical cancers (see the overview below).

Merck & Co

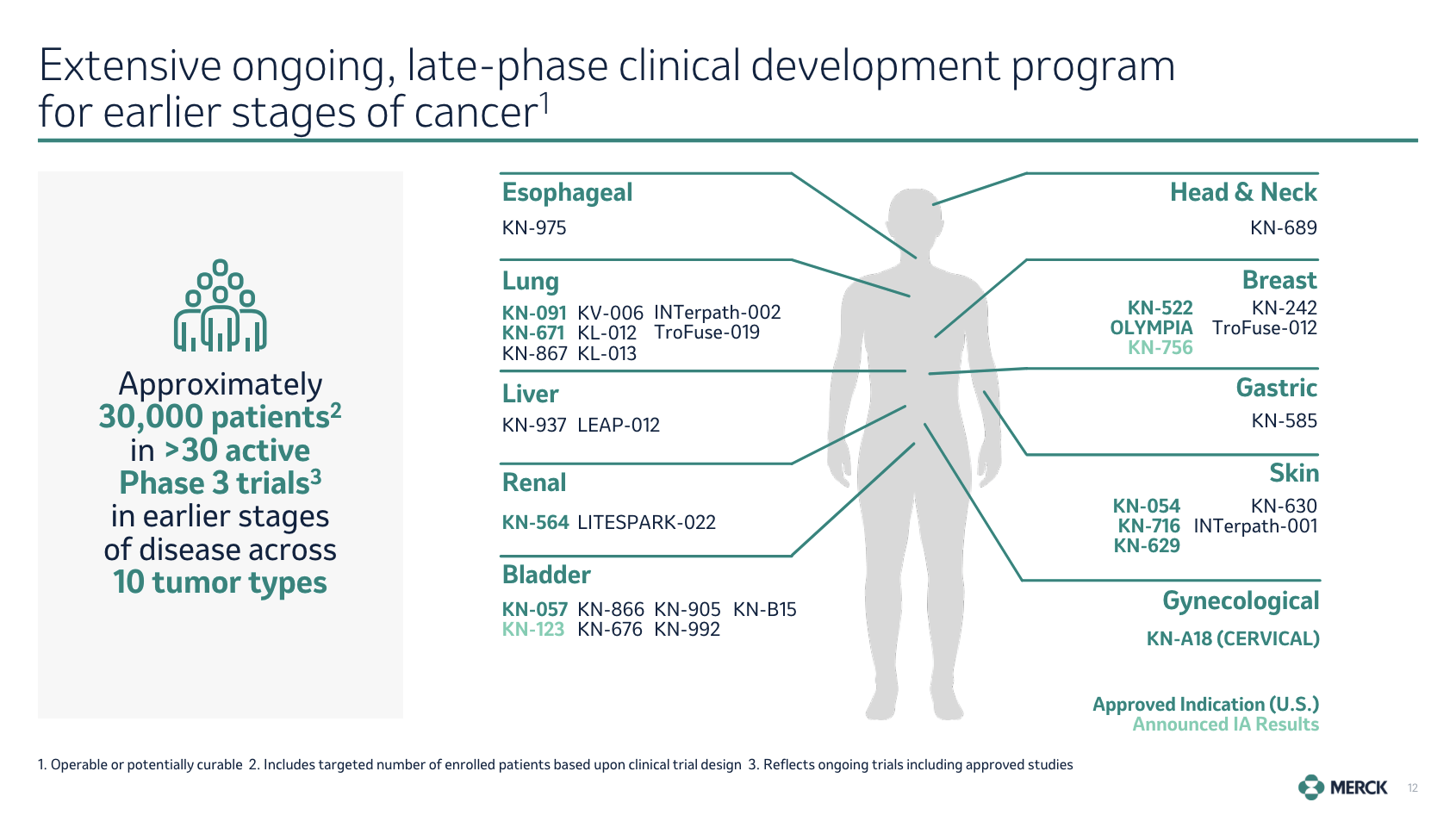

In light of OS rates, the company has enrolled roughly 30,000 patients in more than 30 phase III trials to target earlier-stage cancers.

As one can imagine, these trials are important, as they show OS rates in early stages and benefit both patients and the overall healthcare system.

Merck & Co

Even better is the fact that the results of these trials have shown impressive outcomes.

According to the company, the KEYNOTE-671 trial showed a 28% reduction in the risk of death for patients with resectable (can be removed with surgery) non-small cell lung cancer.

Meanwhile, the KEYNOTE-564 trial reported a 38% decline in the risk of death for patients with renal cell carcinoma post-surgery.

Merck & Co

On a side note, I’m leaving out some of the in-depth characteristics of these drugs.

During the aforementioned conference, the company explained a lot about the various treatments and how these drugs work, including precision molecular targeting.

I decided to leave some of that out to keep the main focus on the “big picture” and avoid turning this into a scientific paper on cancer drugs.

That said, in light of what we already discussed, I care more about how well Merck is now positioned to grow.

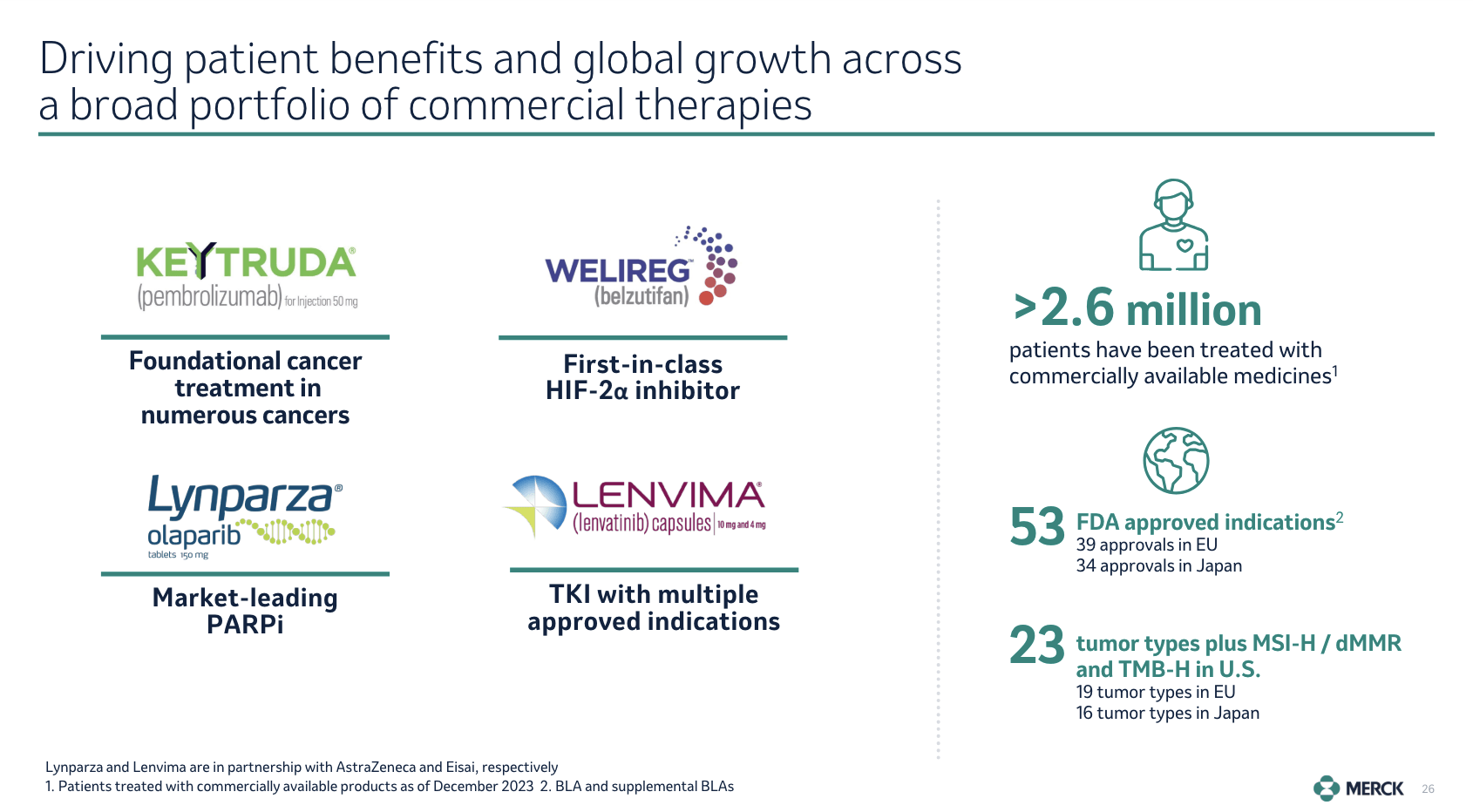

Using the overview below, it has a portfolio that serves 2.6 million people worldwide, supported by 53 approved indications across 23 tumor types and two tumor-agnostic indications in the U.S. and more than 70 indications in the EU and Japan.

Merck & Co

On top of a fantastic pipeline, the existing product portfolio has been very successful.

For example, in the U.S., treatment rates for early-stage non-small cell lung cancer have increased from 35% to 65% since the launch of KEYNOTE-091.

As we can see below, KN-091 was approved in 2023.

In general, earlier-stage indications represented roughly a fifth of all KEYTRUDA revenue last year. This share could rise to a quarter by the end of this year.

Merck & Co

Moreover, adjuvant treatment rates for high-risk early-stage triple-negative breast cancer have reached 65%.

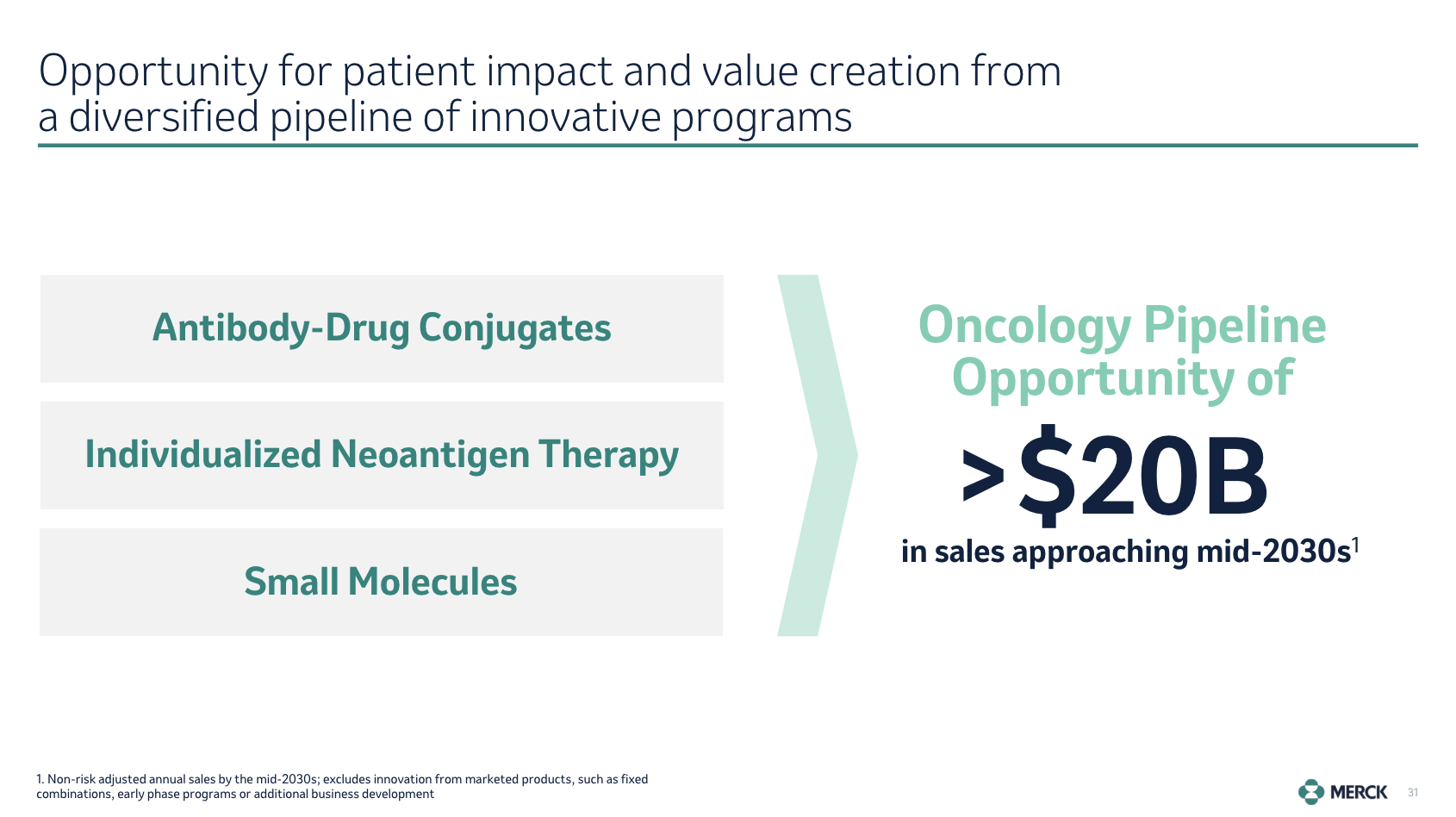

Putting all of this together, the company believes its oncology pipeline will generate incremental sales of $20 billion by mid-2030!

This excludes sales from currently marketed products.

Moreover, this year, the company is guiding for at least $63.1 billion in total revenue. $20 billion in incremental revenue is almost a third of that.

Merck & Co

So, what does all of this mean for shareholders?

I Believe The MRK Shareholder Value Is Highly Attractive

In general, Merck is doing well.

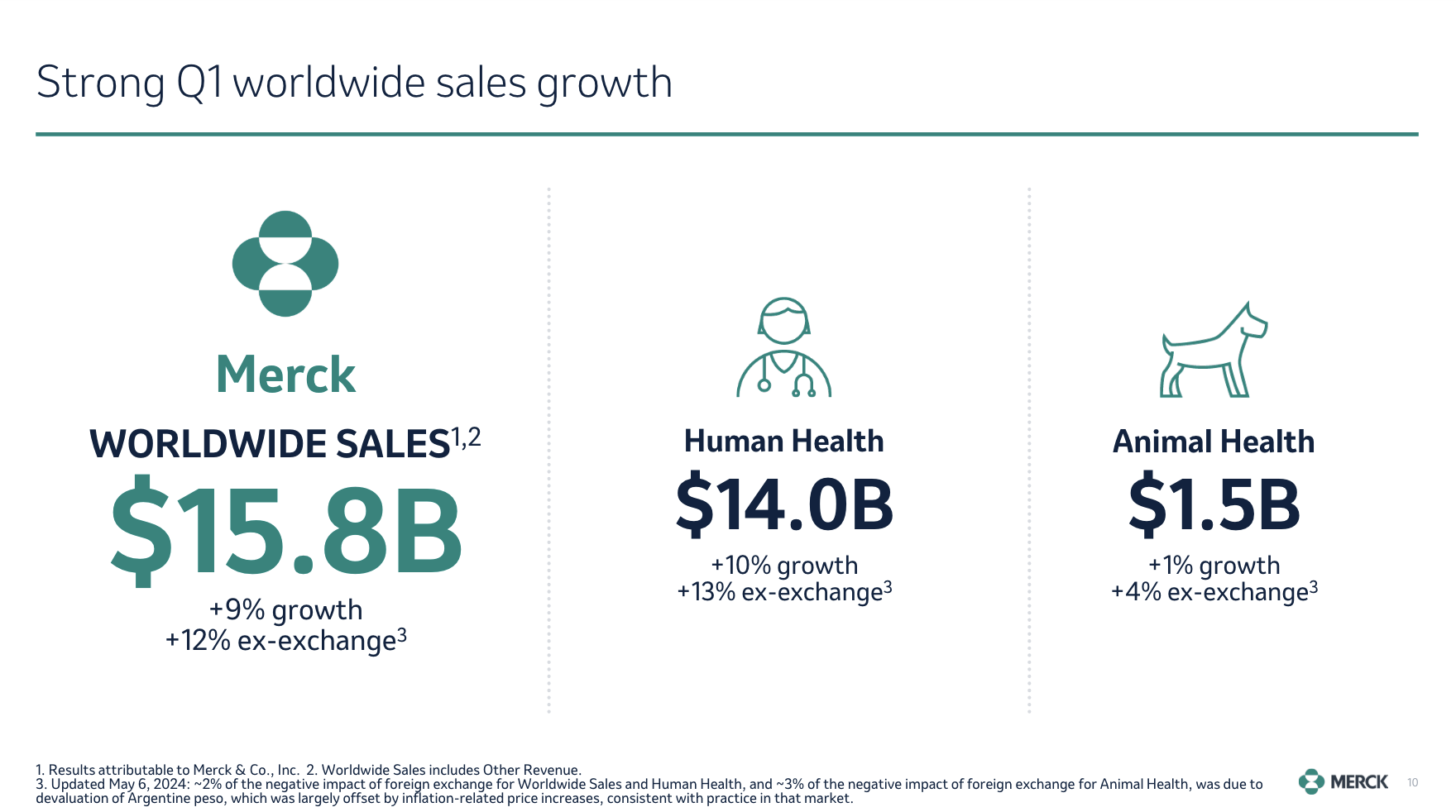

For example, in 1Q24, the company reported $15.8 billion in revenues. That’s 9% higher compared to the prior-year quarter and 12% higher if we exclude the impact of currency headwinds.

Merck & Co

KEYTRUDA saw a 24% increase in sales, totaling $6.9 billion, driven by the benefits we discussed in the first part of this article.

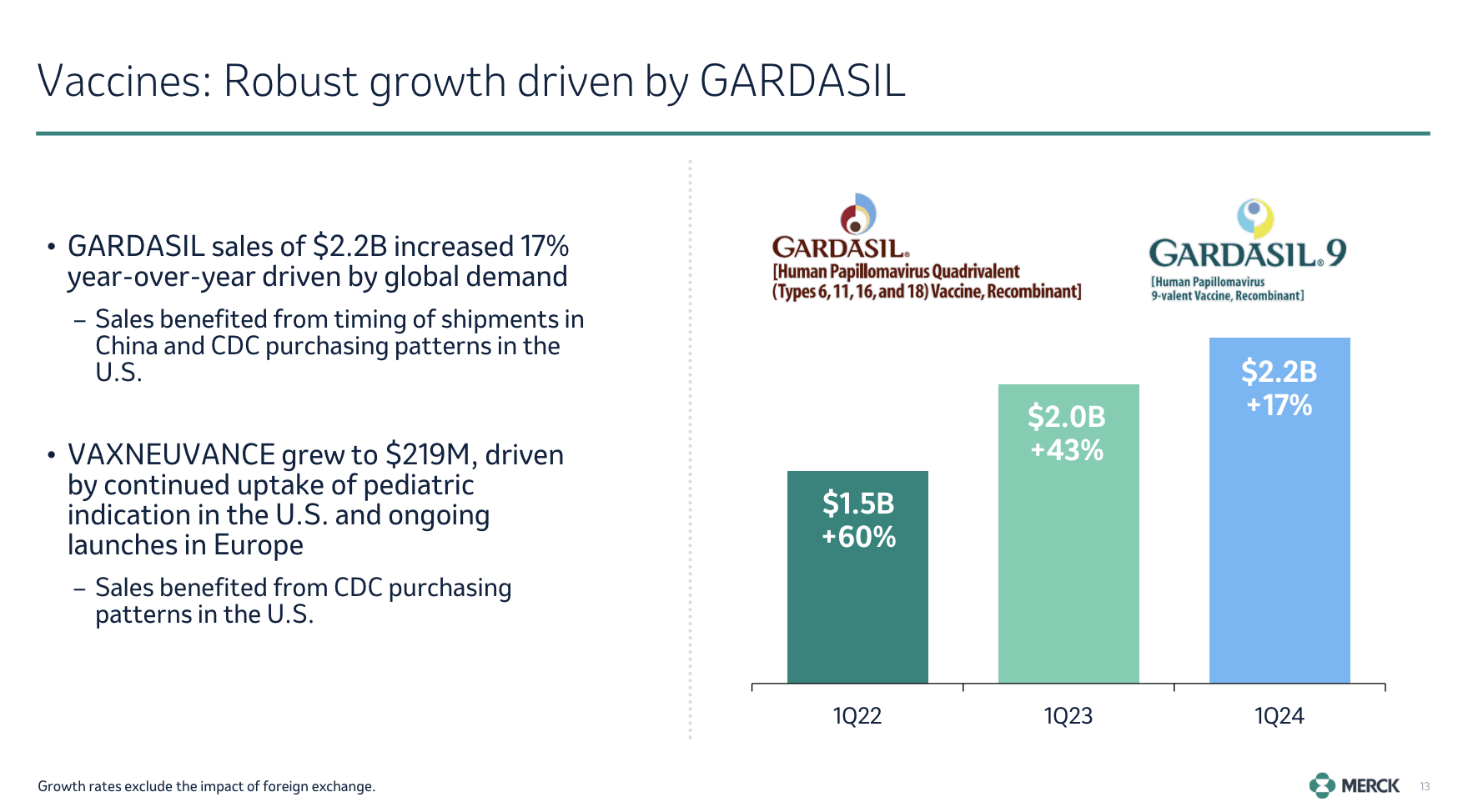

The vaccines portfolio, led by GARDASIL, also delivered strong growth with a 17% increase in sales. This vaccine protects women against various types of cancers.

In the first quarter alone, this vaccine generated $2.2 billion in revenue. Two years ago, that number was $1.5 billion.

Merck & Co

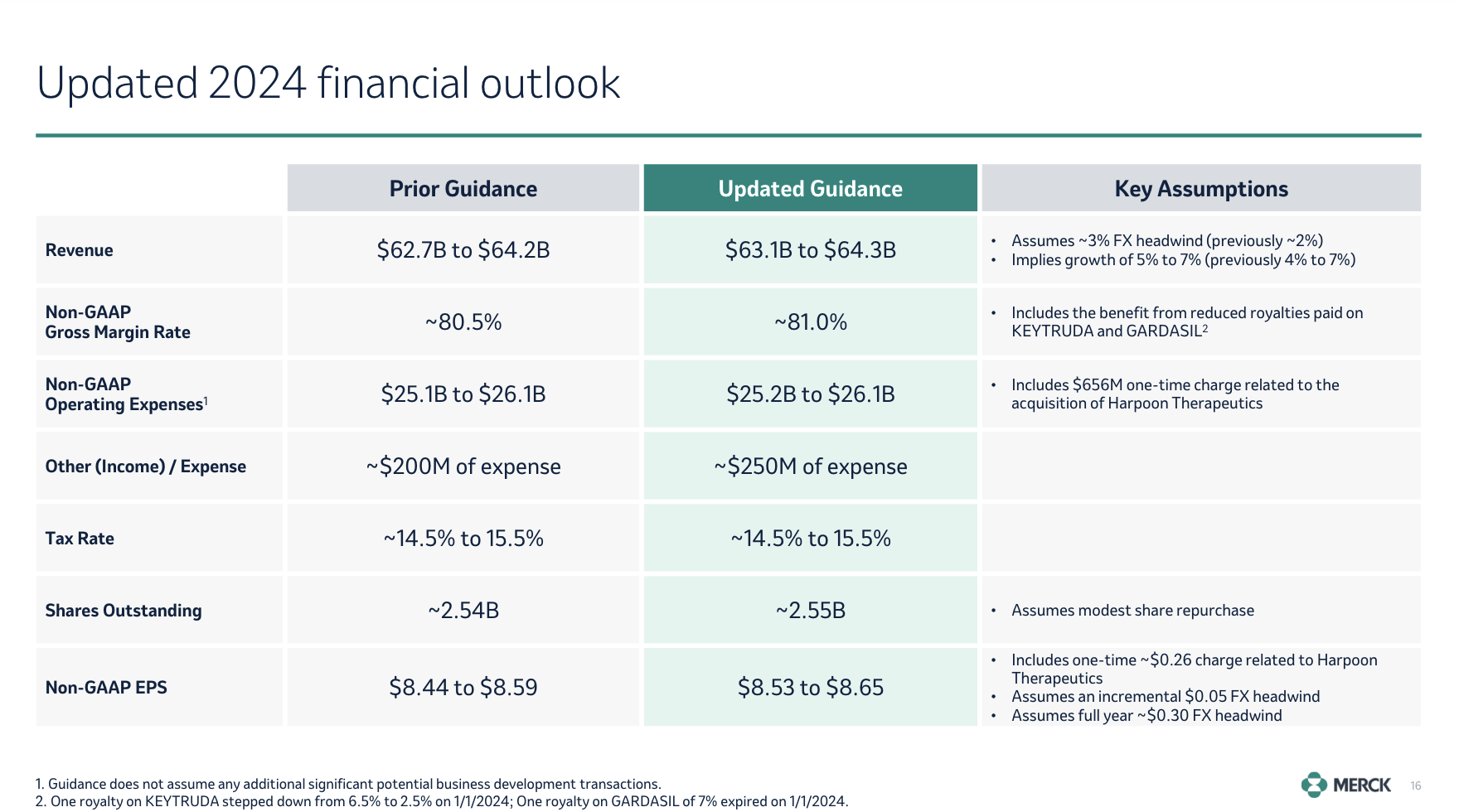

Thanks to strong results, MRK raised its full-year guidance, expecting between $63.1 and $64.3 billion in sales. This translates to between 5-7% year-over-year growth – despite foreign currency headwinds.

EPS is expected to come in between $8.53 and $8.65, also higher than previously expected.

Merck & Co

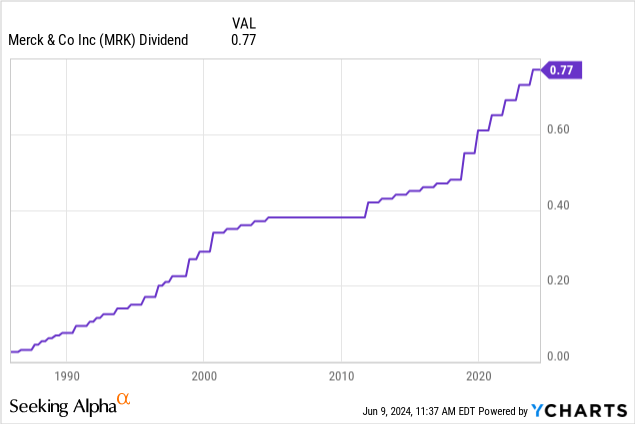

It also helps that MRK has a favorable dividend.

After hiking its dividend by 5.5% on November 28, it currently pays $0.77 per share per quarter. This translates to a yield of 2.4%.

This dividend comes with 13 consecutive annual hikes, a five-year CAGR of 8.8%, and a 2024E payout ratio of 36%, using the company’s EPS guidance.

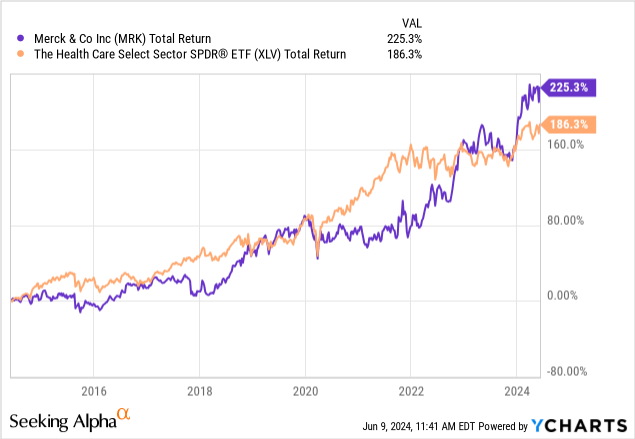

I believe the mix of favorable dividend growth and a fantastic oncology pipeline are the reasons why MRK has outperformed the Healthcare ETF (XLV) over the past ten years, returning 225% (versus 186%).

Even better, MRK is still attractive.

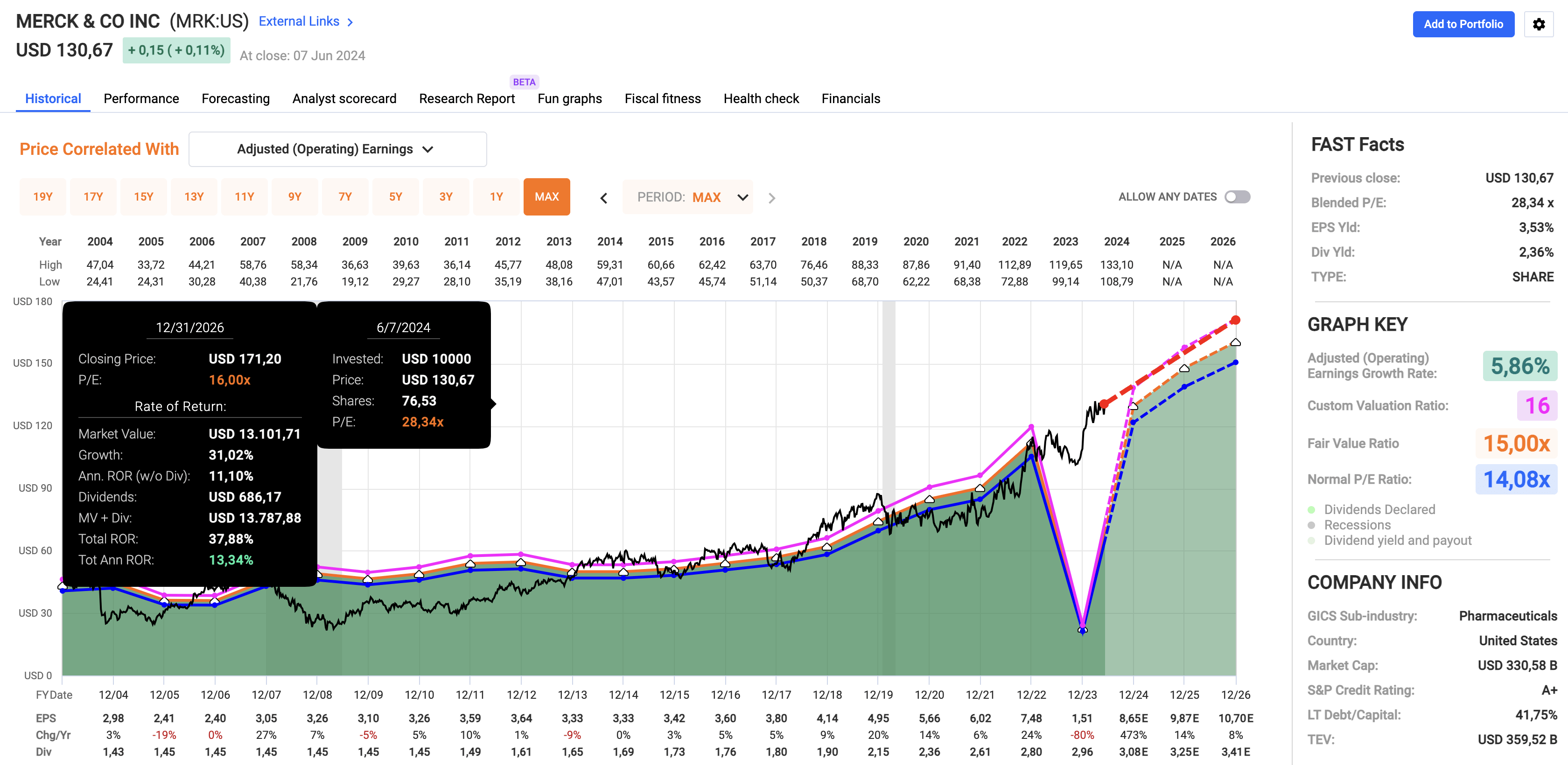

Using the FactSet data in the chart below, MRK is expected to grow its EPS by 14% and 8% in 2025 and 2026, respectively. 2024 is expected to be a rebound year after last year’s one-off upfront payments to Daiichi Sankyo.

FAST Graphs

Over the past five years, the company had a normalized P/E ratio of 16x, which would indicate a fair price target of $171, 31% above its current price.

I believe this target makes sense, as it indicates double-digit annual total return potential, including its 2.4% dividend.

Merck also enjoys an A+ credit rating, one of the best ratings in the world. It has a sub-1x 2024E leverage ratio.

As such, I stick to a Buy rating and believe the company is on a path of consistently elevated EPS growth, supported by a fantastic portfolio and pipeline.

Takeaway

Merck’s blockbuster drug, Keytruda, is revolutionizing cancer treatment, showing remarkable results in early-stage cancers.

With a robust pipeline and significant growth projections, Merck is well-positioned for long-term success.

Meanwhile, Merck’s strong dividend history and expected earnings growth further support my confidence.

Hence, I maintain a Buy rating for MRK, expecting elevated returns driven by their innovative pipeline.

Pros & Cons

Pros:

- Innovation in Oncology: Merck’s Keytruda is a game-changer, driving impressive results in early-stage cancer treatments.

- Strong Growth Potential: With an impressive pipeline and projected incremental sales of $20 billion by mid-2030, Merck is set for substantial growth.

- Solid Financial Performance: Recent quarters show strong revenue and EPS growth, with an upward revision in full-year guidance.

- Attractive Dividend: A 2.4% yield, consistent dividend hikes, and a sustainable payout ratio make MRK a reliable income stock.

Cons:

- High Expectations: The success of future growth heavily relies on the continued success of the company’s oncology pipeline and the approval of new indications.

- Market Competition: The healthcare sector is highly competitive, and Merck faces significant competition in oncology and other therapeutic areas. However, given its leadership position, I’m not too worried about that.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Test Drive iREIT© on Alpha For FREE (for 2 Weeks)

Join iREIT on Alpha today to get the most in-depth research that includes REITs, mREITs, Preferreds, BDCs, MLPs, ETFs, and other income alternatives. 438 testimonials and most are 5 stars. Nothing to lose with our FREE 2-week trial.

And this offer includes a 2-Week FREE TRIAL plus Brad Thomas’ FREE book.