Summary:

- Earnings estimates for Nvidia Corporation are all over the place, leading me to translate them into scenarios and applying sensitivities.

- This approach allows us to understand where the current share price stands in relation to all available analysts’ scenarios.

- Trying to be as neutral as it can get about this much discussed high-flyer, I feel no FOMO about Nvidia.

- Nevertheless, I would be a willing buyer with a small portion of my portfolio, yet not at today’s prices.

BING-JHEN HONG

As Neutral As It Gets

Nvidia Corporation (NASDAQ:NVDA) is obviously extensively covered by analysts and contributors, most of whom have clear bullish or bearish opinions about this high-flying stock. I do not have such a clear perspective. Therefore, the purpose of this article is to help us understand the wide range of scenarios currently proposed for Nvidia. With no personal involvement and no special expertise in the sector, this is intended to provide a scenario, sensitivity, and valuation analysis of probably the most discussed stock. This aims to bring a view to the discussion that is as neutral as it can get.

At the end of my analysis, I present my personal game plan on how I approach Nvidia. My result will be that Nvidia seems to be priced at the very upper end of currently available expectations. Given this background, I will only take a small position in the event of a double-digit correction from current levels. Otherwise, I have no FOMO and have no issue with staying out, while some of Nvidia’s customers, Microsoft and Alphabet, are by far my largest holdings.

Spilling The Beans

I owned shares in Nvidia already five years ago yet did not partake in the last months’ and years’ surges. My ownership of Nvidia shares was only of short duration and at that time was not at all tied to its current AI-enabling business model. My initial purchase was with Nvidia still primarily being the graphics card supplier to the gaming industry, which has become a rather mixed segment in terms of reliable growth. I am therefore not at all feeling remorseful about missing out on over 3.000% of returns on a storyline that wasn’t on my radar soon enough. Furthermore, speaking of hypotheticals in hindsight makes no sense at all in the stock market, and I can only warmly recommend this mindset to every investor.

Key Risks Summary

Before getting started with my main thesis analyzing scenarios and sensitivities, I would like to point out that this article does not aim to rehash all the chances and risks that can be found elsewhere in detail. Nevertheless, especially the risks cannot be neglected in a comprehensive article, and therefore I include this section briefly summarizing key Risks I gathered about Nvidia. Chances appear obvious from my point of view and are redundant to enumerate yet again.

- While Nvidia’s competitive advantage and leadership appear to be mostly unchallenged in the foreseeable future, this will naturally change in the mid- to long term. Competitors are no less than other potent public firms.

- Some of these potent firms are currently Nvidia’s customers. Given operating margins of 65% that Nvidia enjoys, it is questionable how much Microsoft, Alphabet, and others will want to lavish their “supplier” with such generous profits if they can potentially develop the competence in-house.

- “Supplier” is in quotes because Nvidia is known for developing and designing their chips. But they are manufactured by companies like TSMC (TSM). Aside from general supply chain risks, Nvidia’s dependence on Taiwan could quickly become problematic, not least due to Chinese threats around the island, which they claim as their own.

- Returning once more to the customers: Nvidia’s success is based on the arms race for AI capabilities and their anticipated productivity gains. If such expectations are exaggerated, it would not be good for Microsoft, Alphabet, and others — continuing with the examples given — but they can quickly stop their investment behavior. Nvidia, as the “shovel maker” in this gold rush, could immediately crash out of the curve.

- Export restrictions to China make life hard for Nvidia in this market, where local tech giants like Huawei could become competitors.

- Nvidia’s status as a monopoly in a key technological area might prompt government intervention. However, it could just as well be that the government supports the domestic market leader as a flagship company.

All Over The Place

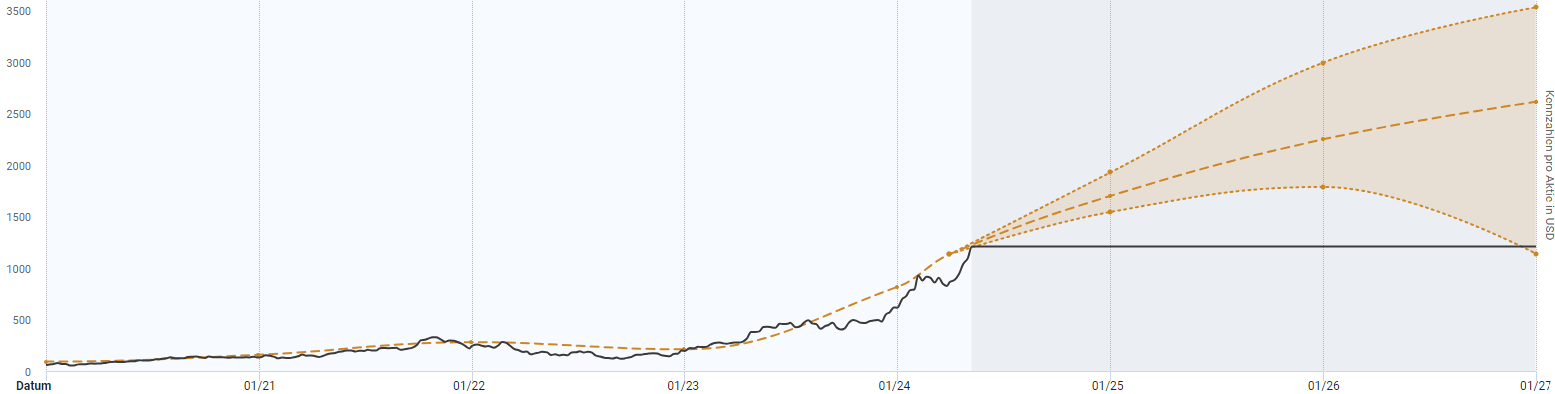

Getting to the core of my thesis, this heading describes analysts’ expectations for Nvidia best. Below you see Nvidia’s stock price in black with the center orange dashed line representing the adjusted EPS (consensus) times the current adjusted P/E multiple. It is crucial to understand that this does not show price targets or stock valuation but uses the current valuation to display how future analysts’ estimates diverge, illustrated by the forecast funnel. Uncertainty that high should lead to high discount rates. Moreover, scenario and sensitivity analyses appear indispensable. This qualifies discounted cash flow analysis, or DCF, as a viable method, even if some claim it is not for a company like Nvidia.

Aktienfinder.net

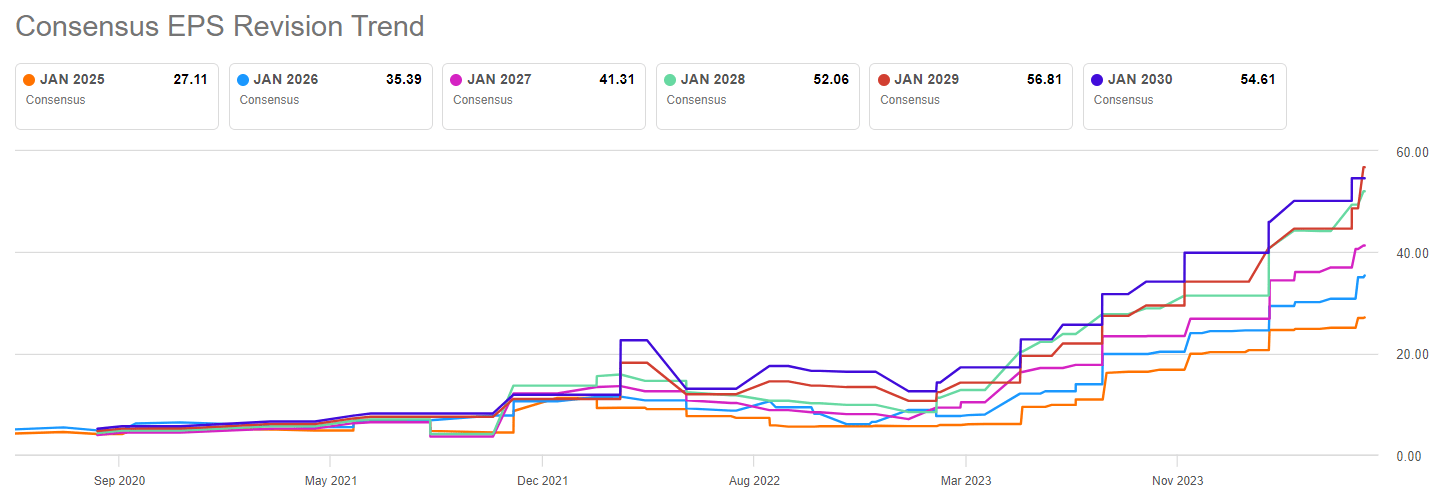

What makes consensus estimates for Nvidia especially unreliable and therefore underscores the necessity for scenarios and sensitivities is the fact that they have had to be revised upwards quarter after quarter to entirely new levels. This, in turn, indicates that analysts’ estimates could still be conservative.

Seeking Alpha

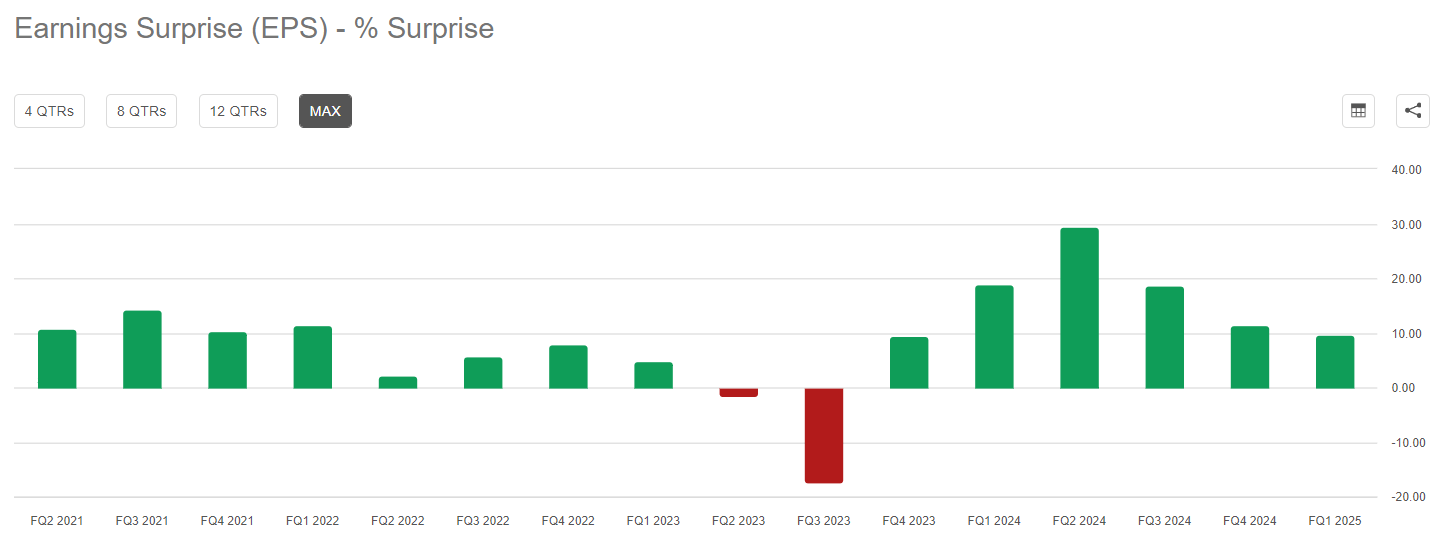

On the other hand, continuously increasing expectations make it harder to beat them. This is complaining at a high level, as seen below, Nvidia was able to exceed Street expectations almost consistently, often by a significant margin. At times, by as much as 20 to 30 percent. However, the declining beat-trend over the past four quarters indicates that these high expectations are gradually catching up to Nvidia’s high potential. This could make further significant beats more challenging because a lot is already being priced in.

Seeking Alpha

Don’t Be Too Generous With Capital Costs

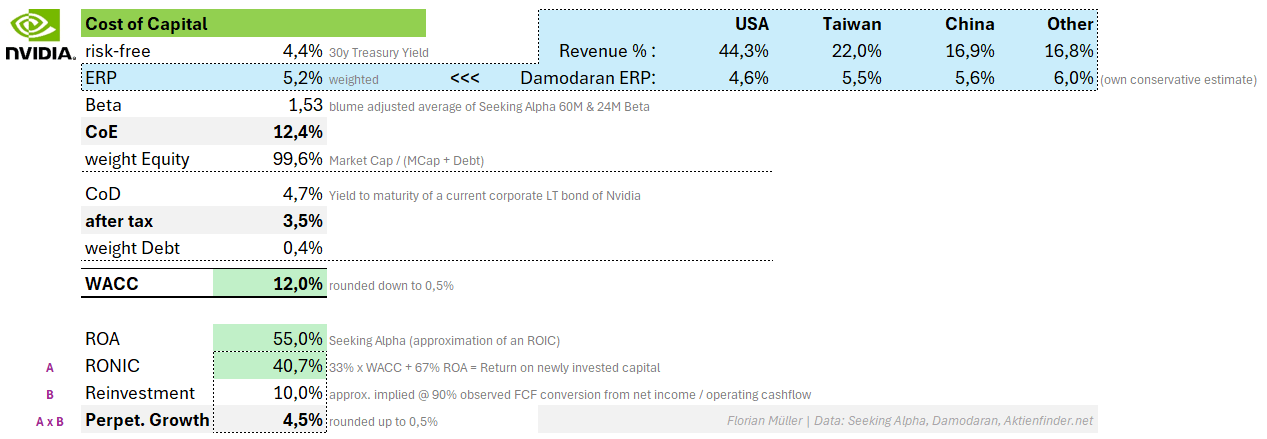

Although some present it as if it were, Nvidia, despite its impressive growth, is far from immune to all kinds of risks and demands the same level of rigor in determining its cost of capital. All the following is summed up in the table afterward. With market capitalization completely overshadowing debt providers, Nvidia’s WACC is effectively equal to its cost of equity. This is slightly increased by country risks in China, Taiwan, and internationally. However, it is primarily driven by a significantly elevated beta factor. I have even applied the normalizing Blume adjustment to this Beta to avoid being overly conservative. Summarizing, I round Nvidia’s WACC to a value of 12% and will vary this in later sensitivity analyses.

Author | Data: Seeking Alpha, Damodaran, Aktienfinder.net

To estimate a perpetual growth rate for the years following 2029, I took a look at Nvidia’s latest Return on Assets as a simplified ROIC proxy, which stands at an astonishing 55% according to Seeking Alpha. Assuming that this return is yielded on newly invested capital, with a longer-term drift towards WACC, I calculated a 41% return on newly invested capital (RONIC) going forward. From operating cash flow or adjusted EPS, a Free Cash Flow conversion of approximately 90% is observed, implying that the 10% gap was reinvested in the business. 10% reinvestment times 40+% RONIC leads me to estimate a rounded 4.5% perpetual growth rate. This will also vary later through sensitivity analyses.

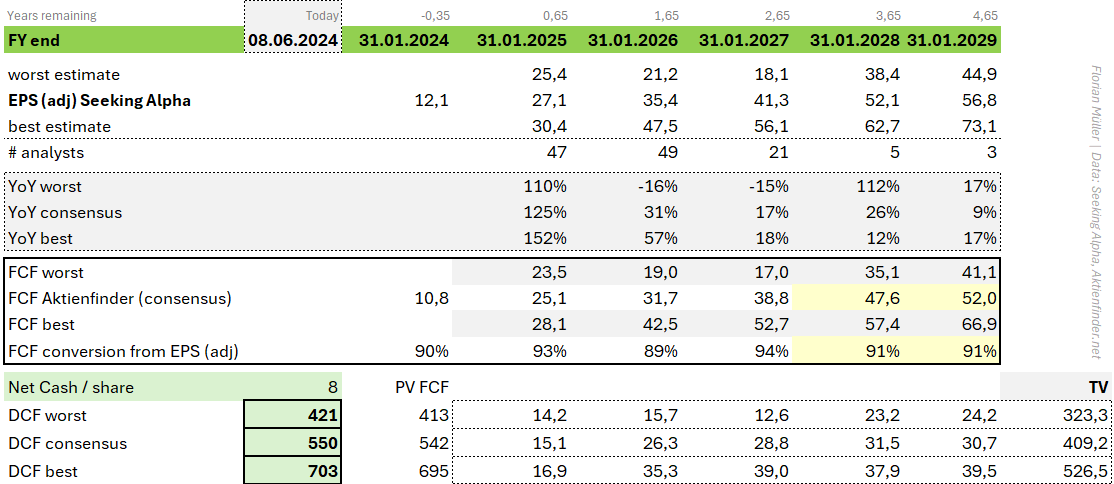

Spot Estimates For All Kinds Of Forecasts

I am now considering the whole range of analysts’ estimates for adjusted EPS as long as at least three estimates are available, which is the case until early 2029. Where I lack free cash flow data, I apply the free cash flow conversion as far as observable and apply it to the adjusted EPS estimates. Finally, adding net cash, I land at spot estimates per share of

- 421 USD based on the most pessimistic forecasts,

- 550 USD based on the consensus forecasts, and

- 703 USD based on the most optimistic ones.

However, this still assumes my WACC of 12% and terminal value growth (TVg) of 4.5% after 2029.

Author | Data: Seeking Alpha, Aktienfinder.net

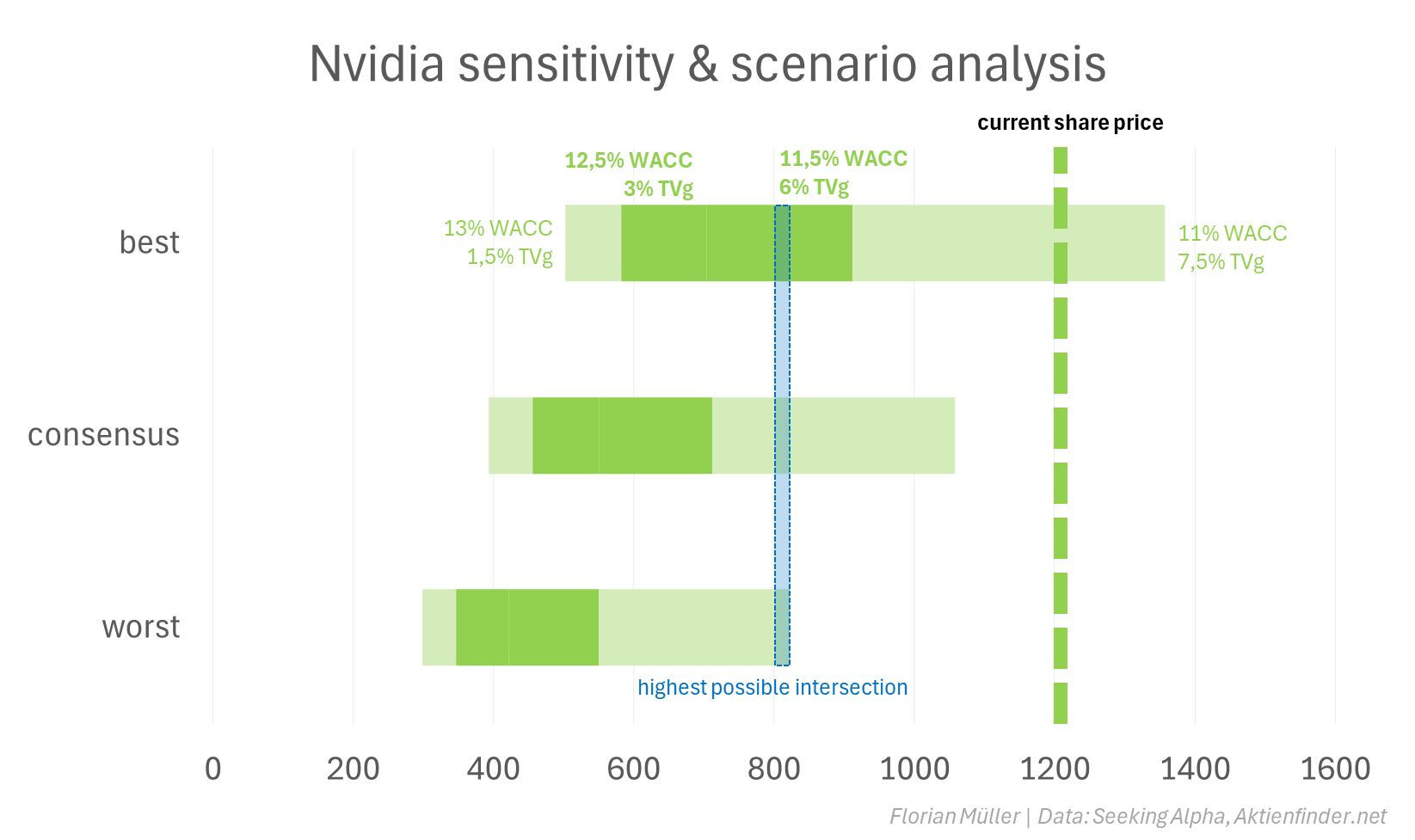

Sensitivities Indicate High Expectations Priced In

I have now performed respective sensitivity analyses for all three scenarios, with the sensitivity parameters being WACC and Perpetual or Terminal Value Growth (TVg). This yields the result that,

- based on consensus estimates, the current share price of approximately 1,200 USD is unreachable, with the highest value landing at less than 1,100 USD at 11% WACC and 7.5% TVg.

- Justifying around 1,200 USD per share or more would require relying on the best of all analysts’ estimates until 2029, then applying a 7.5% TVg and a maximum discount rate of 11.5% — all of which is, of course, within the realm of possibility. Therefore, I would not speak of a bubble.

Author | Data: Seeking Alpha, Aktienfinder.net

My Game Plan For Nvidia

Finally, please refer to the graphical visualization of my analyses below, which once again illustrates that only the most optimistic currently available estimates, combined with the depicted valuation parameters, lead to justifying the current share price. For myself, I have set a game plan on how I will approach Nvidia. I consider a price around the highest possible intersection of all scenarios highlighted in blue to be adequate. This is above 800 USD per share (or 80+ USD after the stock split) and

- represents my utmost positive valuation limit of the weak analyst estimates,

- a sensitivity considerably above my spot estimate based on consensus estimates, and

- even a slightly progressive valuation stance based on the most optimistic estimates.

At the same time, this implies that, given all the uncertainty, I would buy into Nvidia in case a 30% correction from its current levels might occur.

Author | Data: Seeking Alpha, Aktienfinder.net

Takeaway

With this article, I wanted to provide readers with the truth that none of us can with any, not even close, certainty estimate whether Nvidia is currently completely overvalued, fairly valued, or significantly undervalued. As a non-tech guy, which most of us investors are, I have no qualified opinion on what the actual operating core business of the company could be doing in the long-term future, which I am confident enough to say out loud here. Therefore, all I can do is run the models, do the math, and observe expectations priced in.

With Nvidia, this leaves me to remain as neutral as I can get. I plan to buy in with a 1%-of-portfolio position in case of a significant double-digit dip. 1% that I don’t mind losing much in case this was still a bubble, and 1% I will enjoy seeing multiply, in case Nvidia might still not be priced to its groundbreaking potential. Neither regretting that I am not in with more.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in NVDA over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.