Summary:

- Since the start of the year, the market has been under enormous pressure.

- Inflation, rate hikes, supply-chain disruptions, and China’s zero-covid policy all trigger a global recession.

- This environment brought even the most loved stocks to their knees, stocks that were market favorites for the last several years and put out incredible returns for their shareholders but have had trouble this year.

- In this series, I want to look at some of these stocks and give a quick look at their recent developments and if they are “buys” yet.

Derick Hudson

Introduction

In this series, I write about stocks I call “Fallen Angels”. You can read what exactly I mean by this term in the introduction of the two prior articles of this series.

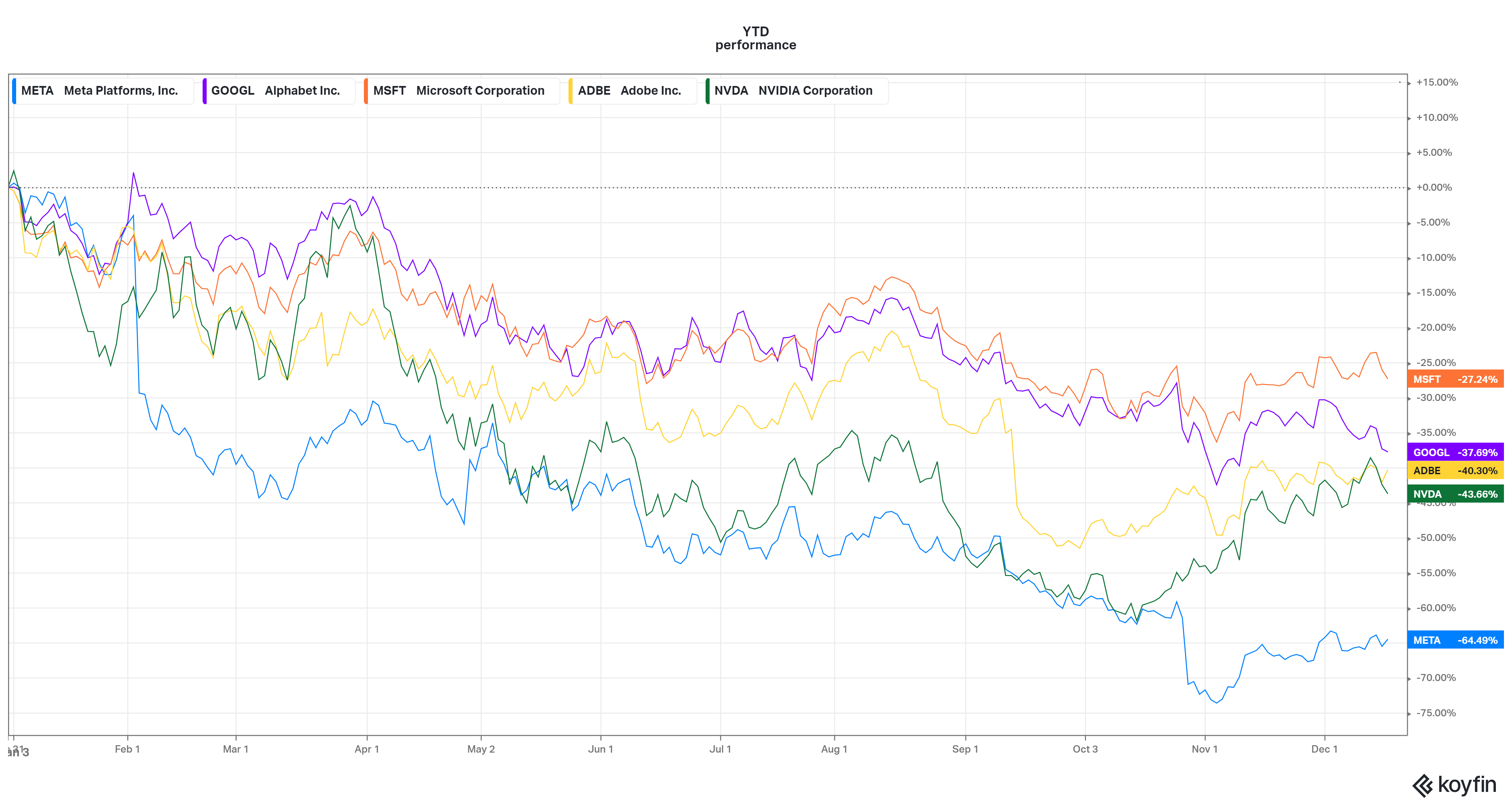

In short: stocks that had a tremendous performance in the last five years but took a deep dive this year. In the following chart, you get a first impression.

YTD performances (koyfin.com)

Meta Platforms (NASDAQ:META) is one of these stocks with a year-to-date performance of -65%. In the following, I will explain why that is and what that means for the stock from my perspective. I will dig into two fatal quarterly earnings and put the earnings in charts to visualize how badly the earnings have deteriorated. This, future growth outlook, and a problem I see with management’s metaverse spending make it hard for me to like META even though the valuation seems tempting. But I will get to all this in length in this article.

I think it is important for you to know my current view of the market. In the previous two articles, I wrote a whole paragraph on why I think the market could fall further next year. Click here to jump to the right paragraph to read more about my former view of the market. In short: I expect a higher level of the fund’s rate for a longer period of time and an earnings recession in the next year as a consequence.

The last FOMC meeting proved me correct. Powell is still inclined to hold onto his strategy to bring down inflation to his 2% goal.

“Changing our inflation target is something we’re not thinking about. We’re not going to consider that under any circumstances. We’ll use our tools to get inflation back to 2%,”

“Historical experience cautions strongly about cutting rates prematurely,”

“As for core services inflation, excluding housing, “we do have a way to go there.”

You can find these and more quotes here.

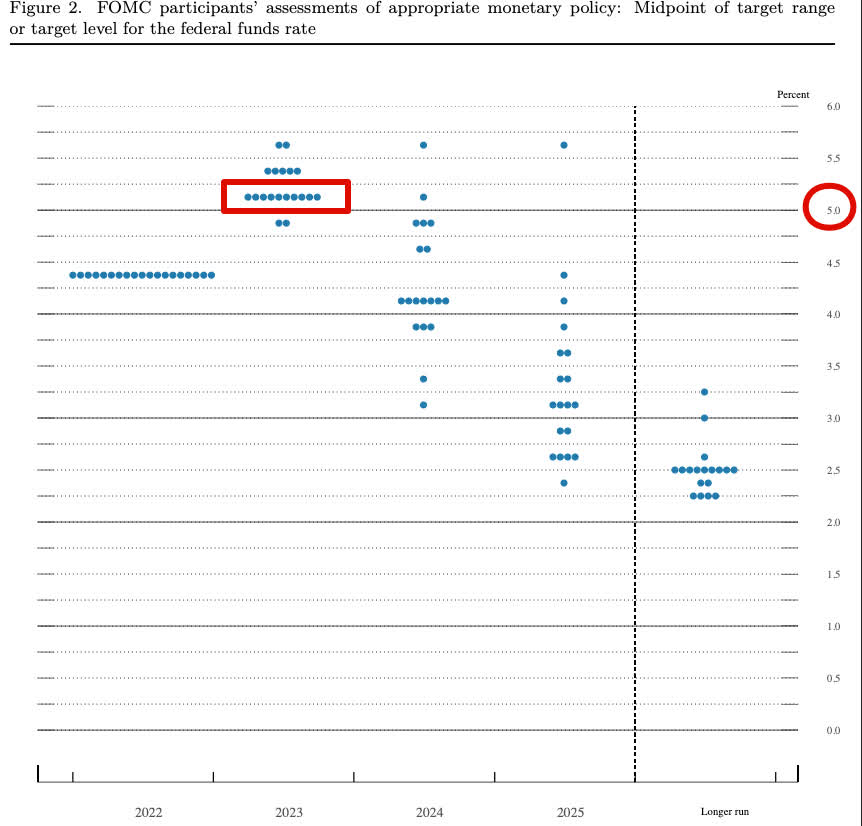

Additionally, the year-end rate for 2023 was increased to 5.1%, up from previous expectations of 4.6%. The dot plot shows not only that but also that rate cuts back to the levels of the last few years will take years:

Fed dot plot (Fed)

Official explanation by the FED: Each shaded circle indicates the value (rounded to the nearest 1/8 percentage point) of an individual participant’s judgment of the midpoint of the appropriate target range for the federal funds rate or the appropriate target level for the federal funds rate at the end of the specified calendar year or over the longer run. One participant did not submit longer-run projections for the federal funds rate.

This, in combination with this chart I showed in the other articles, gets me to the conclusion that a Fed pivot is maybe not as near as some might think, and even if the Fed pivots, it doesn’t have to guarantee you that the market has bottomed. Hence, I see the rally since the October lows as rather unsustainable gains.

But now, let’s start with the third stock of this series:

Meta Platforms (META)

META, formerly known as Facebook, was a famous and generally liked stock by the market for the last few years. META started with Facebook as the greatest social media platform and got more famous with big accumulations of apps like WhatsApp and Instagram. META did well in monetizing Facebook and Instagram and became the leader in the ads market. However, this year Facebook started to struggle, and CEO Zuckerberg’s plans to build a metaverse platform started concerns and caused the stock to fall.

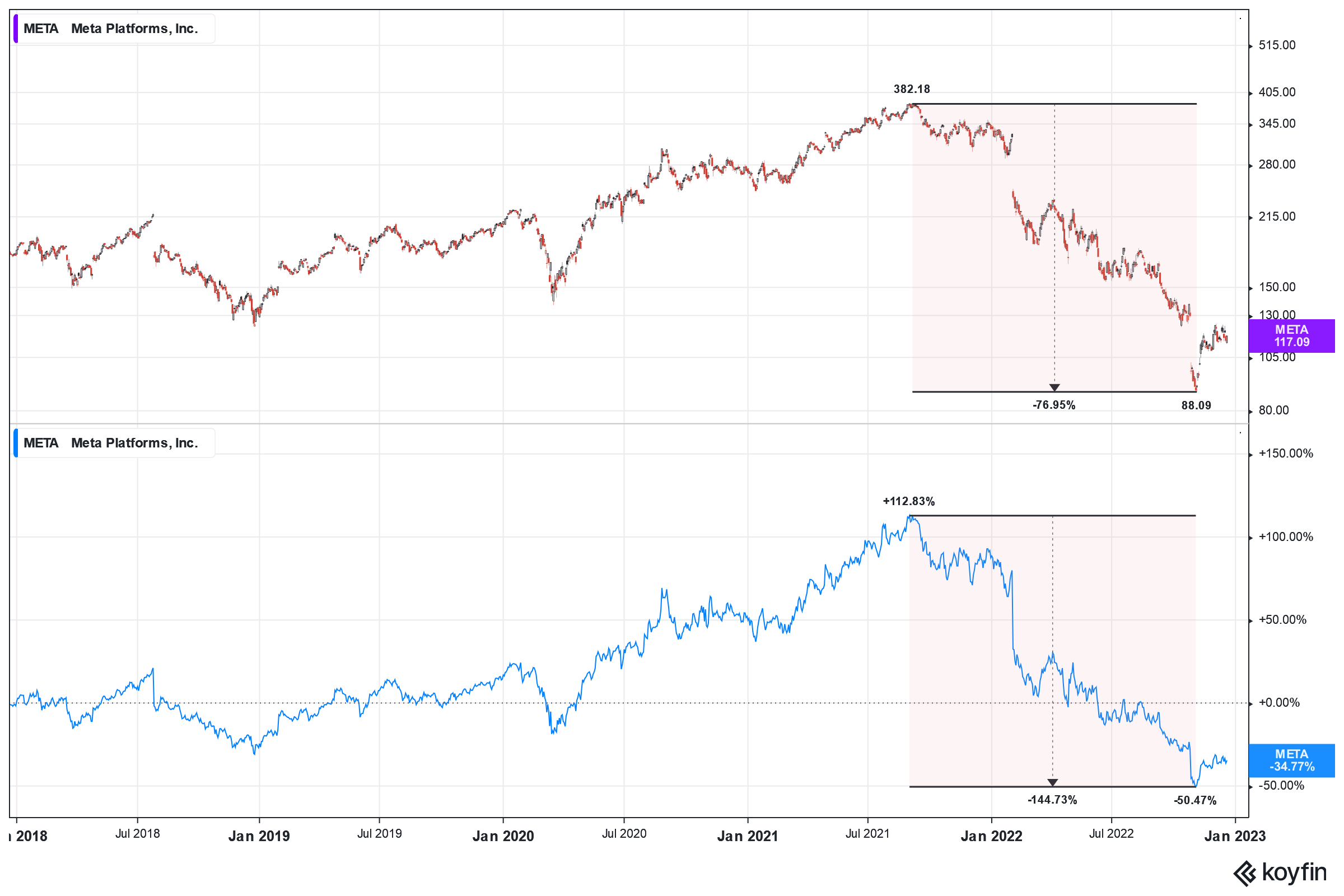

5-year peak performance and drawdown (koyfin.com)

As you can see, the share price dropped by almost 77% to the lowest level since 2015. The performance was +113% at its peak in September 2021 but dropped by an astonishing 145% to -50% at its lowest point. As of the time of writing, the performance is -35% for the last five years. That’s obviously bad, and the worst we have seen, and probably will see, in this series.

Other than with NVDA, we haven’t seen such a sell-off in the history of META yet, underlining the severity of this particular sell-off.

What happened?

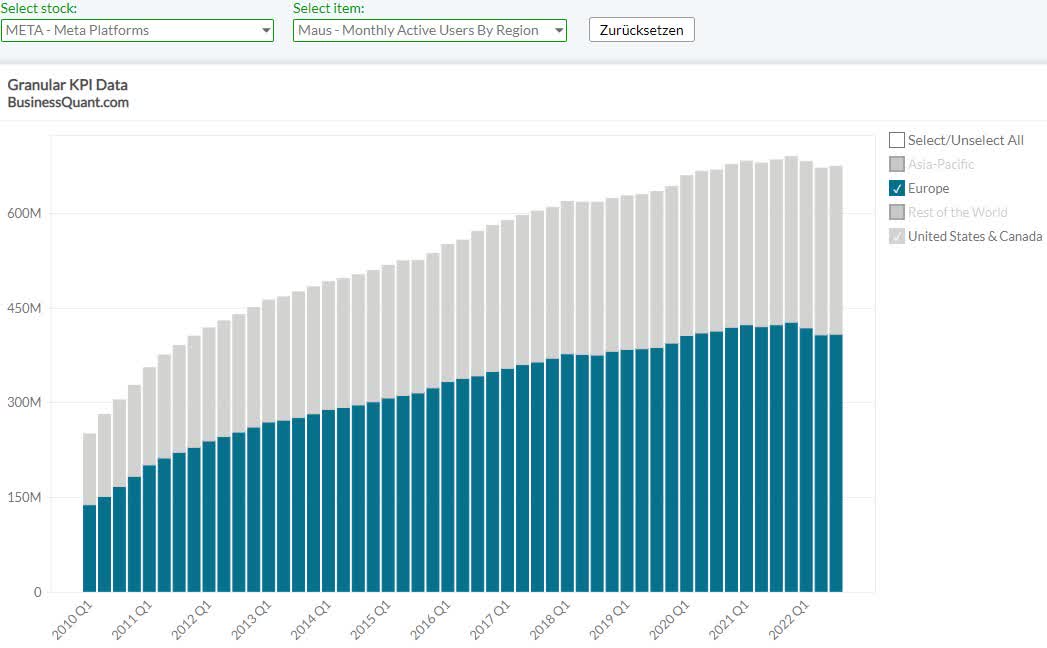

The big sell-off started with the Q4 2021 earnings, which got published in February this year. META missed earnings estimates by just 4%, but daily active users (DAUs) and monthly active users (MAUs) estimate miss, light guidance, and details about the metaverse losses worried the market and spurred a 26% sell-off the day after earnings. This is the greatest earnings sell-off META has ever seen. Revenue rose by 20% YoY to $33.67B, but costs and expenses grew by 38%, fueling a decrease in net income of 8% YoY. For the first time in META’s history, META had to report slower-than-average growth in DAU and MAU numbers that couldn’t reach expectations. Daily active users came in at 1.93 billion (up 5%), vs. Street estimates for 1.95 billion. And monthly active users of 2.91 billion (up 4%) came in short of expectations for 2.95 billion. The only growth of users is registered in Asia-pacific and “rest of the world.” As you can see in the following charts, DAUs and MAUs in the US and Europe are decreasing. This happened only one time before in 2018, but this time the decrease is way more severe. This is due to a higher competition with TikTok gaining more traction in the social media market and taking away META’s share of people’s time spent online.

DAUs by region (businessquant.com)

MAUs by region (businessquant.com)

Considering that US & Canada and Europe bring in the most revenue, this development should raise concern for future growth prospects.

In the Q4 earnings, META changed its reporting structure for the first time, breaking out the results of its metaverse efforts in the Reality Labs unit.

The metaverse, Zuckerberg’s big dream of the future, is supposed to be the next big thing for Meta. They even changed the name from Facebook to Meta Platforms to underline the importance of its new project. Andreas Steno Larsen of Steno Research put together why such projects like the metaverse may work in times of 0% rates but not in times of rising rates and with problems like high inflation and decreasing liquidity.

Here are two quotes:

I have a concession. The 0% yield curve of 2020/2021 turned me into a financial imbecile temporarily. I guess a lot of you know the feeling. Large sudden returns, no whatsoever value of money in sight and high-fives all around the sectors I was employed in. It felt good.

Take the idea of the metaverse. Its launch was probably advanced by the zero interest rate environment and as a consequence Meta and Mark Zuckerberg are now pissing away decent cash-flows on a project that no-one cares about during a cost of living crisis.

You can read the full article here: 3 reasons why everyone, Zuckerberg, me, and their dogs turn into idiots when rates are 0%.

My opinion regarding the metaverse is that this project is a big waste of money. If the metaverse is indeed the future of our living, META will profit enormously from being the first big mover in this space. If not, META will have spent an enormous amount of shareholder’s money that is gone by then. As of now, META has just created a worse-looking Sims.

META’s metaverse (meta.com)

This gets even worse, considering the amount of money META put into that. In Q4, the Reality Labs unit lost $3.3B, up from $2.1B a year ago. These two quarters alone account for $5.4B of losses for the metaverse. Imagine what META could have done with this money instead. Here are two examples that would have benefited shareholders:

- Buy back 1.75% of its shares

- Pay a dividend per share of $2.06 – meaning a dividend yield of 1.75%

This is calculated using the losses of (just) two quarters and the current share price of $118.04.

Q3 2022 was another earnings report that caused a massive sell-off of 24% the day after publishing. The second-greatest sell-off in META’s history.

Let’s connect with the metaverse again and assess its development.

The Reality Labs unit has bled $3.7B in the latest quarter, bringing the total losses to $9.44B for the nine months ended September 30.

Additionally, META said this in its press release:

We do anticipate that Reality Labs operating losses in 2023 will grow significantly year-over-year. Beyond 2023, we expect to pace Reality Labs investments…

At this point, we should ask ourselves if META is the right company to manage shareholders’ money.

Other stats of this earnings release weren’t much better either. Revenue decreased by 4%, and DAUs and MAUs continued to decline. The decline in revenues and an increase in costs and expenses of 19% brought down operating income by 46%, with operating margin almost cut in half to 20% from 36% in the year-ago period.

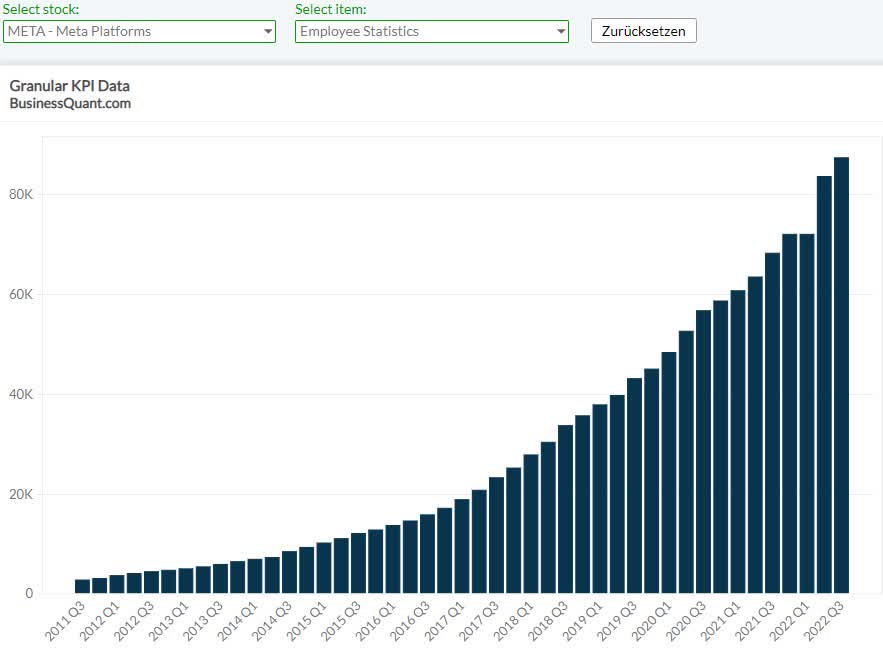

One thing that wasn’t discussed as much in the Q4 2021 earnings is the employee count, which rose by 28% YoY to >87K employees.

Employee count (businessquant.com)

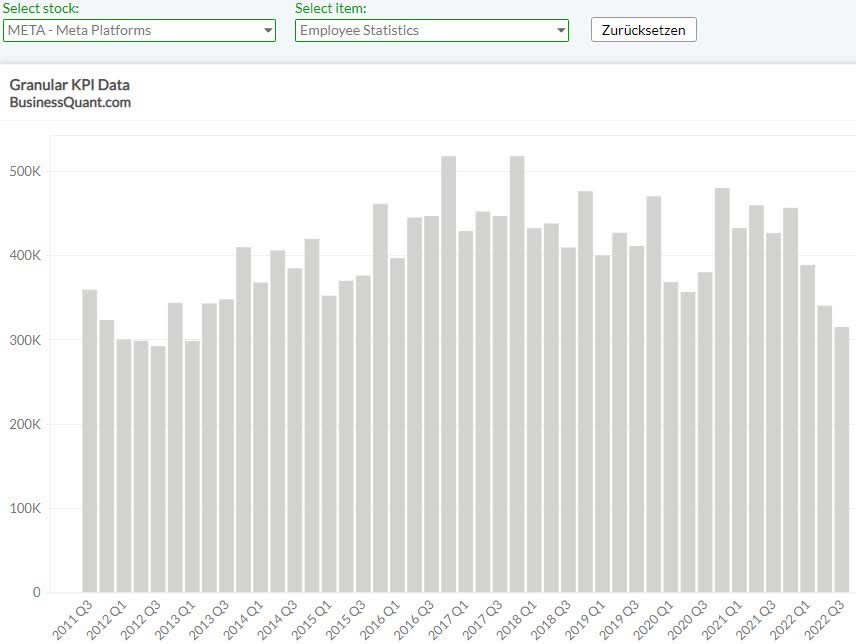

Notably, the employee count rose significantly this year, a year of rate hikes and economic slowdown. For me, personally, this is a sign of mismanagement. Of course, the management’s track record is good, considering all the years since going public, but the current development concerns me. Decreasing revenues and rising employee count brought the revenue per employee to the lowest since 2013.

Revenue per employee (businessquant.com)

After a massive backlash by the market and other tech companies firing employees, on 11/09, META stated to fire 11K employees, or about 13% of its headcount. This statement came after they said their headcount would stay the same through 2023 in their Q3 earnings. I think that it seems like the management’s actions aren’t on par with the changes in the current economy. Nevertheless, this is good news. But considering this brings the headcount not even back to the start of the year, this shouldn’t make the market too happy, in my opinion.

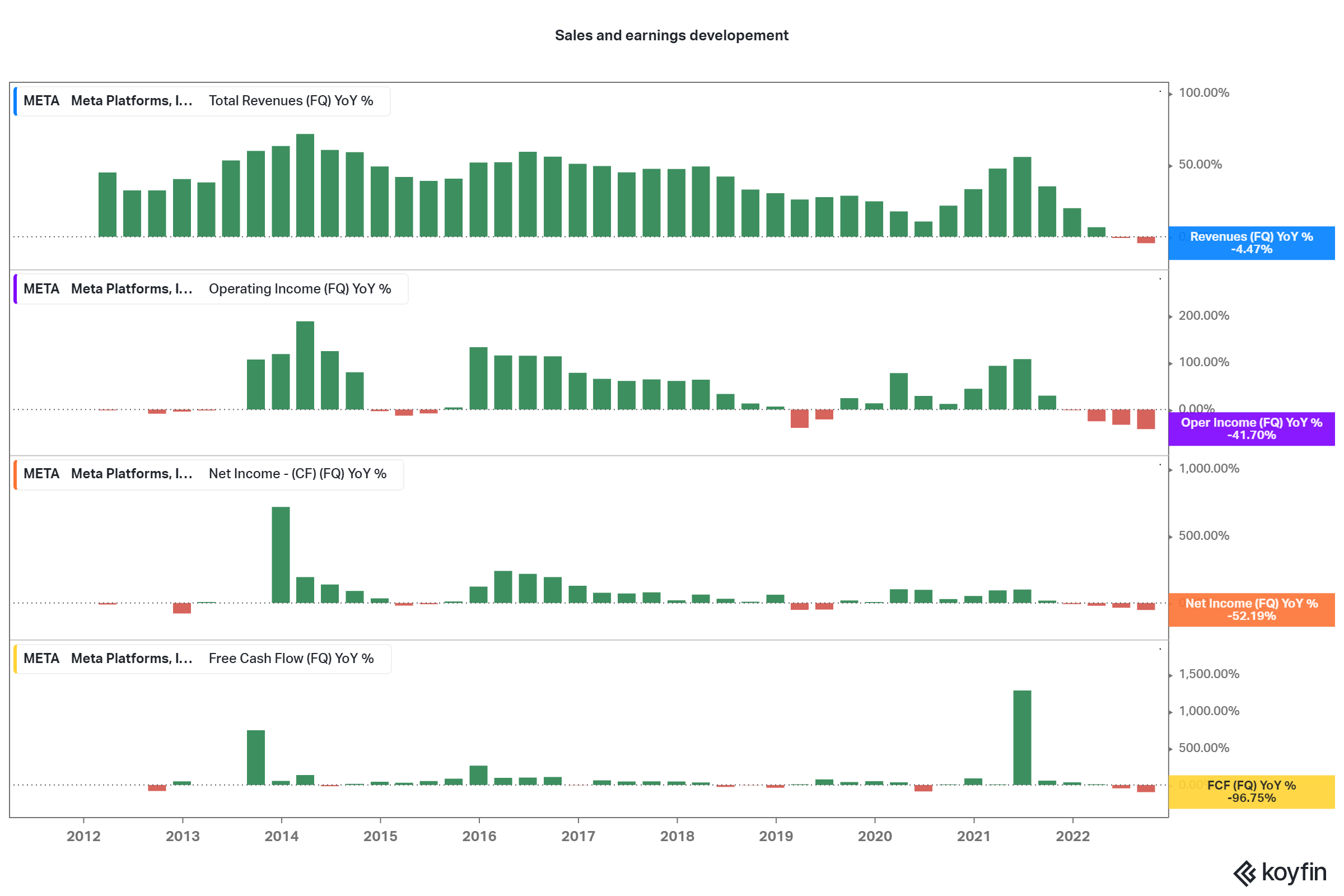

After discussing two of the worst quarterly earnings of META, let’s look at the big picture of earnings, like in the last two articles of this series.

Sales and earnings development (koyfin.com)

As you can see in the chart, the development we saw in the last two quarters is a premier for META. Never before was the YoY growth negative. All other metrics have seen negative growth before, but operating income and free cash flow were never before so bad. Free cash flow declined by a staggering 97%! Net income is just the second worst since going public, but that was ten years ago.

This comparison shows the bad state in which META currently is.

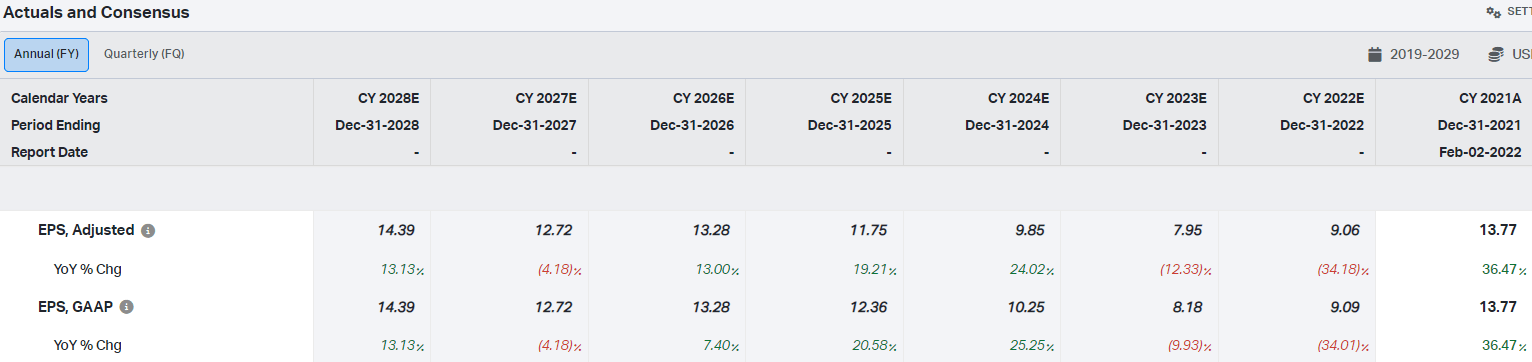

Do analysts think this will change in 2023 and beyond?

Not directly. Almost every metric is expected to decline further YoY for the next three quarters, and only sales are expected to pick up positive growth one quarter earlier than the earnings metrics.

Actuals and consensus (koyfin.com)

So it will take a long time for META to pick up on growth again and reach earnings and sales. According to analysts, it will take until 2028 to break the 2021 annual EPS.

EPS forecast (koyfin.com)

Is META’s valuation making up for all that?

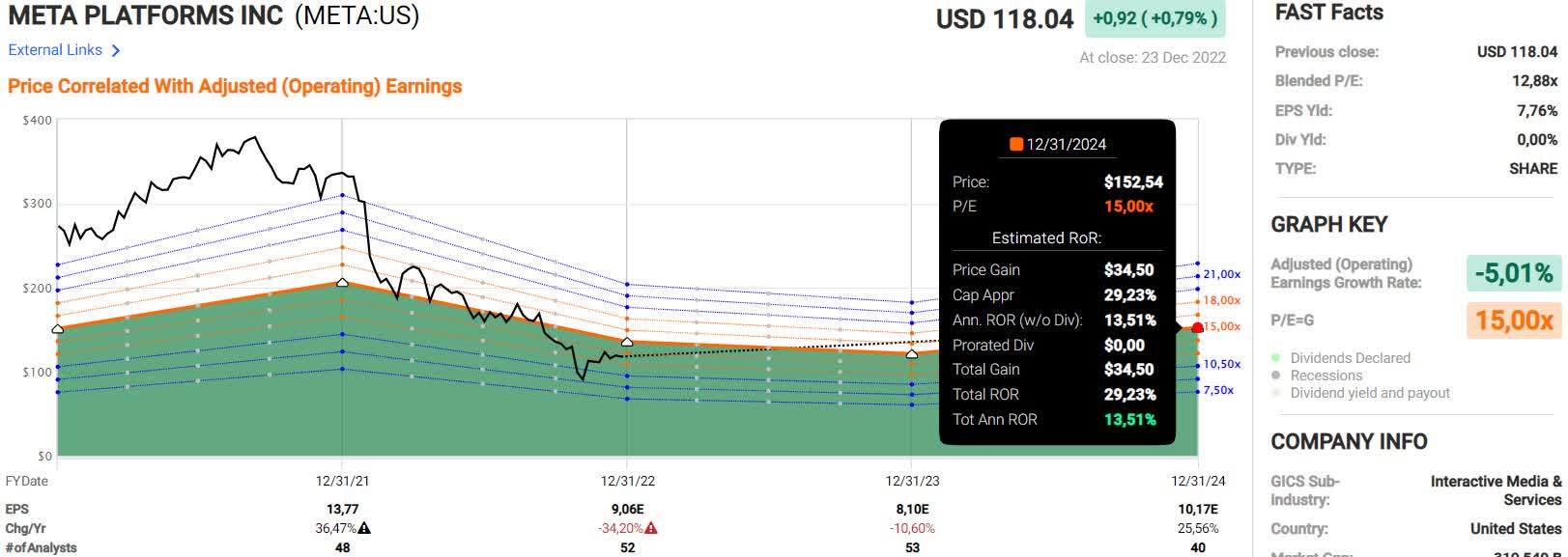

Looking at FastGraphs’ five-year chart, META is fairly valued at about 15x earnings.

FastGraphs five-year chart (fastgraphs.com)

If we look at the estimates, the 15x earnings fair value, according to the growth estimates, gets you an annual return of 13.5% until the end of 2024.

FastGraphs forecast (fastgraphs.com)

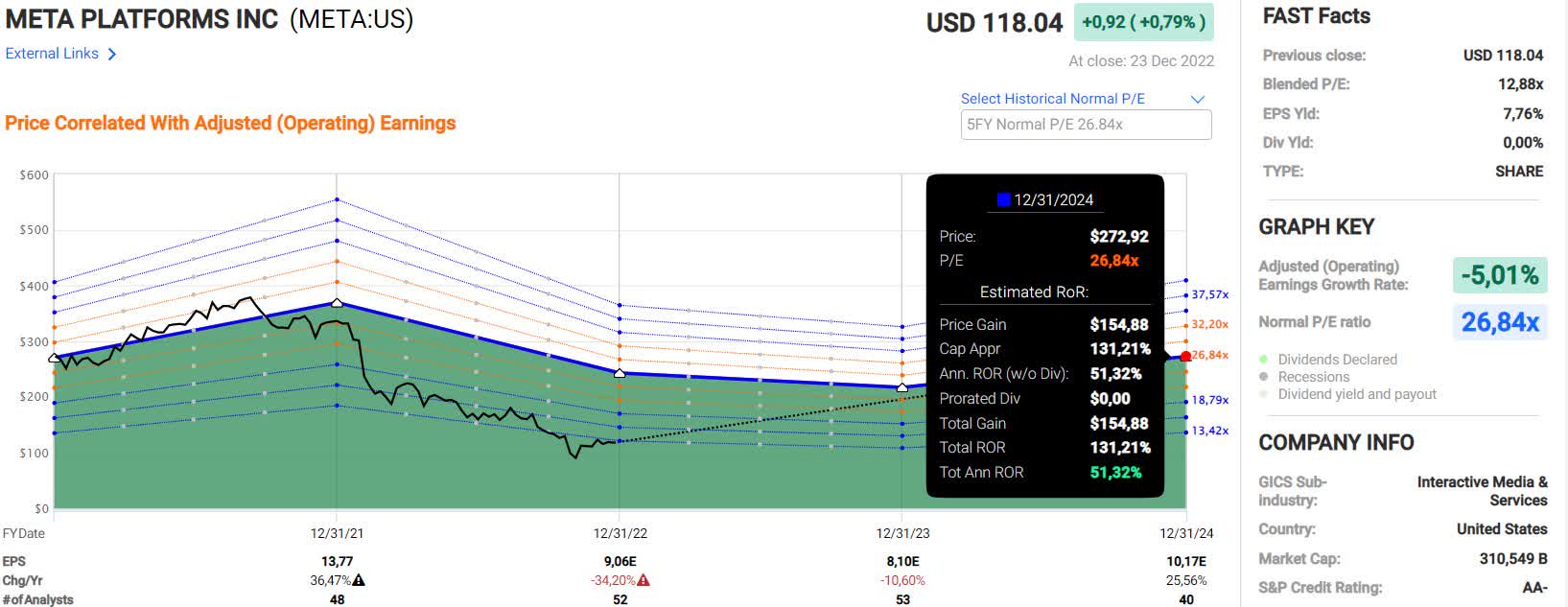

If META were to reverse back to its five-year average earnings multiple, you would get annual returns of over 50%.

FastGraphs average multiple forecast (fastgraphs.com)

I think which of these scenarios we will see depends on whether META continues with its current spending on the metaverse. If it continues as it did this year, I think a 15x multiple is reasonable. In my opinion, the 13% annual returns aren’t appealing enough for the risk you have to take on with buying now. For a reverse back to its average earnings multiple, META would probably need a complete change regarding metaverse spending and a believable plan to combat the new challenges in the social media world.

I think the first scenario is the more probable one.

Conclusion

Due to a disastrous 2022 and probably further declines in 2023, the stubborn clinging to the metaverse dream, and a management that, to me, seems like it isn’t fully aware of the changes in the economy, I have to rate META a sell. For me, it seems that the current management is clearly on the wrong path and not managing META as I wish they would. I think that is one of the worst things that can happen to a company. I don’t touch such companies, no matter how undervalued they might be. Until I don’t see changes in management staff or a complete makeover of their plans for the future, META will be a sell for me.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.