Summary:

- Johnson & Johnson has seen its shares drop to a 52-week low.

- The company is well-prepared to weather a potential recession.

- Shares are inexpensive and offer an above-average dividend yield.

sutthirat sutthisumdang

Article Thesis

Johnson & Johnson (NYSE:JNJ) has seen its shares drop to a new 52-week low this week. The company offers a safe and steadily growing dividend, and its business model makes it resilient versus recessions and other macro crises. Overall, I believe that JNJ stock is an attractive low-risk pick in the current environment, especially since its valuation is far from demanding right here.

What Happened?

Johnson & Johnson has seen its share price decline to the low $150s in the very recent past, which is down 7% over the last year and which is down around 20% from the 52-week high that was hit in spring 2022. This has made JNJ comparatively inexpensive, as we will see later on.

There was no immediate huge reason for the share price decline. Instead, an overall decline in equity markets, rising interest rates that make income stocks comparatively less attractive, and some adverse news about an ongoing lawsuit. But since JNJ has been battling baby powder-related lawsuits for years, that’s not really a good reason for JNJ’s market capitalization to decline by many billions of dollars, I believe.

JNJ: Well-Positioned For Any Crisis

Johnson & Johnson is a very large and diversified healthcare giant. Its operations are divided across three sectors, pharmaceuticals, medical tech, and non-cyclical consumer goods. In a recession, there is a huge advantage here, as none of these three sectors are cyclical. After all, people still require medical care when they are sick or have health problems, thus demand for pharmaceuticals and medical tech is not dependent on economic growth. Some consumer goods are cyclical, but demand for the consumer goods that JNJ sells, such as contact lenses, cremes, etc. is not really dependent on good economic times — in contrary to electronics, autos, and so on.

This resilient business model was showcased again and again in the past, including during the Great Recession. Between 2007 and 2010, Johnson & Johnson did not have a single year of negative earnings per share growth. Instead, earnings per share rose every year in that time frame, by 5% per year on average. That was a very strong showing, considering many other companies ran into major trouble during that especially harsh economic downturn. Of course, since JNJ’s earnings per share kept rising, the company did not have any problem covering its dividend and could keep its dividend growth track record in place.

The pandemic was a somewhat unusual recession, as it did have an impact on JNJ. Since healthcare resources were strained, elective surgeries were pushed into the future in many cases. This, in turn, was a headwind for JNJ’s medical tech business, while at the same time, JNJ did not really benefit from the pandemic with its pharmaceutical business, unlike peers such as Pfizer (PFE) or Merck (MRK) that benefitted from COVID medication sales.

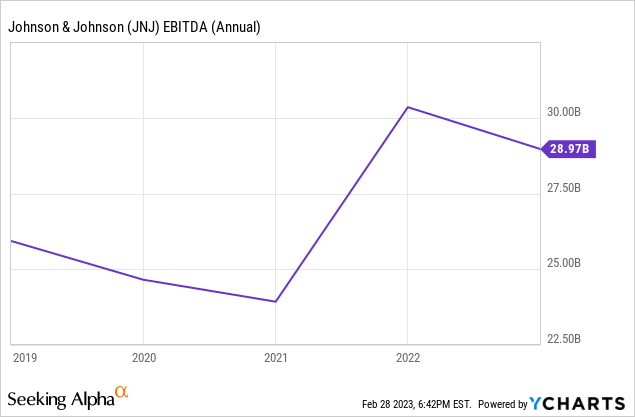

Still, despite the pandemic being more of a headwind for JNJ relative to the average recession, the company remained highly profitable:

We see that EBITDA did indeed decline in 2020, but the decline wasn’t very large on a relative basis — JNJ still did $24 billion in EBITDA in that crisis year, after all. Shortly after, JNJ started to see its EBITDA recover to new highs of more than $30 billion. While JNJ’s profits declined during the pandemic (earnings per share dropped by 9% between 2019 and 2020 before rising again in 2021), they remained high enough to cover the dividend easily, which is why JNJ continued to increase its payout over the last couple of years — in line with what JNJ has done for 60 years in a row in total.

The defensive business model is not the only factor that positions JNJ well for any crisis, however. On top of having a very defensive business model, JNJ also has one of the best balance sheets in the world. Johnson & Johnson is one of just two companies with an AAA credit rating, the other one is Microsoft (MSFT). At the end of the most recent quarter, JNJ’s net financial debt totaled $16 billion, according to YCharts. That’s equal to around 0.5x EBITDA, which is pretty strong.

JNJ Is Inexpensive Today

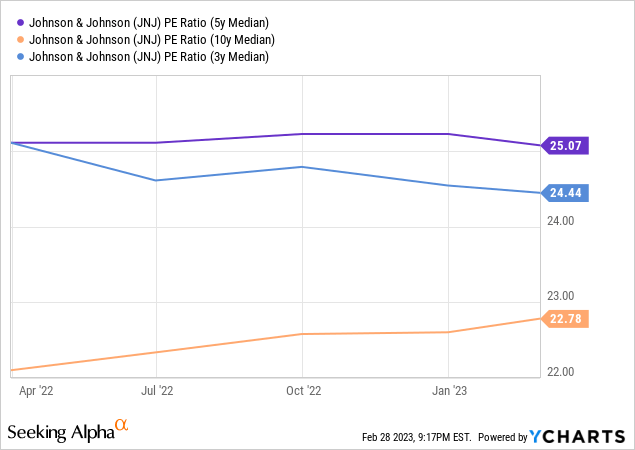

The steep share price decline we have seen in the recent past has made Johnson & Johnson quite inexpensive, both on an absolute basis and on a relative basis. The company is forecasted to earn around $10.50 this year — with shares trading for $153 right now, that makes for an earnings multiple of just 14.6. This compares very favorably versus JNJ’s historic valuation norm, as we can see in the following chart:

The median earnings multiples, according to YCharts, are in the 23-25 range when we look back at the last 3, 5, and 10 years. It is unlikely that JNJ will rise to a valuation this high in the foreseeable future, I believe, but the discount is quite substantial and indicates a good entry point nevertheless. One reason for why JNJ will likely not trade at a 20+ earnings multiple in the foreseeable future is the fact that the company has become quite large. The law of large numbers dictates that growth slows down over time, thus JNJ will likely grow somewhat slower relative to the past decade, which should result in a lower valuation in the future. On top of that, the rise in interest rates justifies some multiple compression as well.

But even if we account for these facts and say that JNJ should be valued at just 18x net profits in the future, versus 23-25x net profit, that would allow for considerable share price appreciation, as the current 14.6x earnings multiple would allow for a 23% share price increase if JNJ were to trade at 18x net profit in the future, all else equal. Even a 16.5x net earnings multiple would allow for a low-teens share price gain, before factoring in future earnings per share growth.

While future earnings per share growth will likely not be massive, it should be meaningful. Rising healthcare expenditures in the US, Europe, and also many emerging and developing countries make for market growth potential, and JNJ also can make acquisitions to boost its growth further, as it has done in the past. Last but not least, Johnson & Johnson should continue to buy back shares regularly, which will shrink the share count, thereby increasing earnings per share over time, all else equal. Historical trends suggest that JNJ should be able to reduce its share count by around 1% per year, thus giving a small boost to earnings per share growth every year.

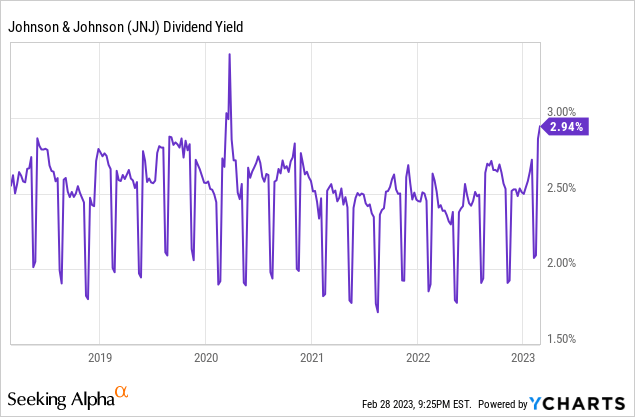

The focus of JNJ’s shareholder return program is its dividend, however. At current prices, Johnson & Johnson offers a dividend yield of exactly 3.0%. That is considerably higher than the broad market’s dividend yield of less than 2%, and JNJ’s current dividend yield also looks favorable relative to the dividend yield the company has offered in the past:

Apart from the initial sell-off during the first phase of the COVID pandemic, JNJ’s dividend yield has not breached 3% over the last five years. Most of the time, the dividend yield was in the 2%-2.5% range. On a relative basis, right now thus seems to be a better-than-average time to add or expand a position in this healthcare giant, at least from an income yield perspective. Since this aligns with the fact that JNJ also looks undervalued based on its below-average earnings multiple, there are good reasons to believe that Johnson & Johnson is an attractive investment at current prices. In the current uncertain economic environment, where many investors fear about a potential recession, JNJ’s proven resilience versus recessions and other macro crises is another argument for going with JNJ when seeking an investment opportunity today.

Takeaway

Johnson & Johnson has just dropped to a new 52-week low due to a share price decline over the last couple of months, which provides an attractive buying opportunity. Shares are historically cheap, the dividend yield is historically high, and JNJ’s proven resilience versus macro shocks could be a major advantage in case we get a recession in the coming quarters. Buying a Dividend King that has raised the dividend for 60 years in a row while the yield is 3% and while the earnings multiple is below 15 seems like a good defensive investment in the current environment.

Disclosure: I/we have a beneficial long position in the shares of JNJ either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Is This an Income Stream Which Induces Fear?

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% – 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio’s price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% – 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio’s price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!