Summary:

- Salesforce comes out with impressive GAAP EPS guidance.

- Salesforce demonstrates that it has listened to investors’ concerns.

- Altogether, the stock is priced at 73x forward GAAP EPS. But here’s why this is a compelling valuation.

Justin Sullivan

Investment Thesis

Salesforce (NYSE:CRM) positively delighted investors with its very strong fiscal Q4 2023 non-GAAP EPS figure. But what truly got investors excited was Salesforce’s GAAP guidance. Yes, actual “real” GAAP guidance, which points to $2.61 EPS at the high end.

One could argue that paying 73x forward EPS isn’t that impressive. But I believe that’s too simplistic a way to consider this business.

This is a business that has a long history of having substantial adjustments to its GAAP EPS figures, either through management’s stock-based compensation or the persistent impairments on the multitude of acquisitions that Salesforce has.

Let’s delve further.

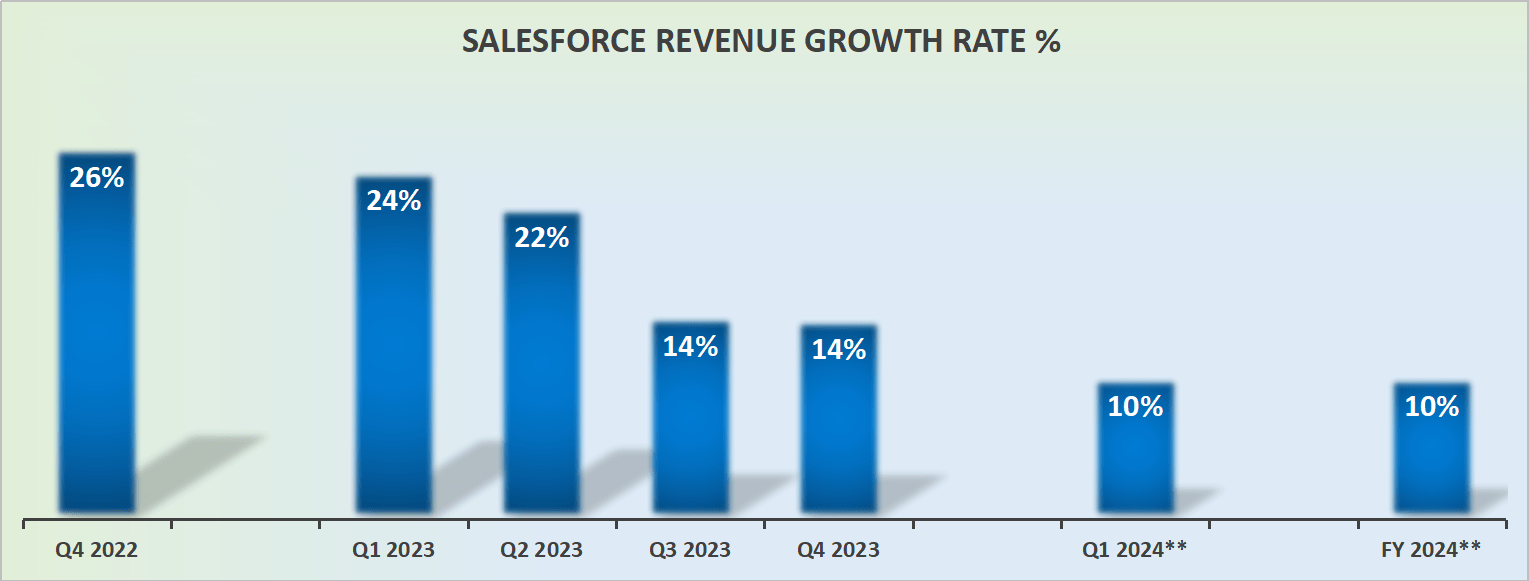

Revenue Growth Rates Are Slowing Down

CRM revenue growth rates

The revenue growth rates shown above are GAAP figures. Nonetheless, fiscal 2024 isn’t expected to have a meaningful drag from FX. Consequently, we can surmise that Salesforce is now done and dusted as a fast-growing business.

On the other hand, investing is all about expectations. In fact, middle-of-the-road guidance can make a company look alluring if expectations are low enough.

SA Premium

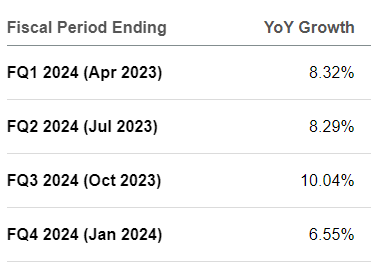

What we see here is that analysts going into the call were expecting Salesforce’s full-year CAGR to drop to 9%. That Salesforce has already risen the bar on its outlook this early in its fiscal year is giving investors’ confidence that Salesforce can with ease clear a 10% CAGR in the year ahead.

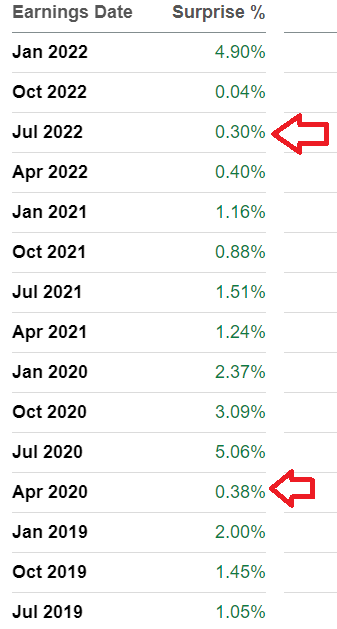

Further, consider that Salesforce has a history of consistently beating revenue expectations.

SA Premium

Even when things get difficult, Salesforce somehow manages to find some way of not missing estimates. This applies to both its revenue line and its EPS line (not shown).

This takes us to discuss Salesforce’s profitability.

What Truly Excited Investors

Salesforce guides to be GAAP profitable for the year ahead. And not just GAAP profitable, but substantially GAAP profitable.

For investors that closely follow the stock, they’ll know that this has been the overarching bear case against Salesforce. That Salesforce’s EPS was essentially made up of stock-based compensation.

And that Salesforce would have to use significant share repurchases simply to minimize the dilution of its stock-based compensation, rather than significantly reduce the total number of shares outstanding.

This statement can best be supported by the fact that Salesforce deployed $4 billion towards buying back stock in fiscal 2023, and the total number of shares outstanding was left practically unchanged from earlier in its fiscal year.

Will All of This Action Improve Salesforce’s Multiple?

As we headed into yesterday’s earnings results, Salesforce’s stock had gone nowhere meaningfully in 3 years. Indeed, for all intents and purposes, unless an investor was extremely nimble or bought at the December lows, most investors would likely be holding a loss on this stock.

For all the excitement of the “‘Benioff” label, shareholders would have been less than satisfied with their investment.

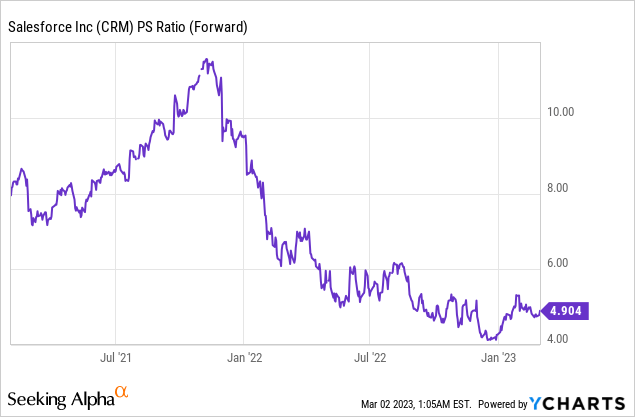

Moreover, as you can see above, for years, Salesforce’s multiple had been contracting. And that’s the problem when a growth company moves to an ex-growth part of its business cycle. There’s a change in how investors appraise a company.

Investors are less willing to pay high multiples to sales. Instead, they become much more interested in paying multiples to earnings.

And in Salesforce’s case, those earnings were getting eaten up by stock-based compensation packages. Leaving little for the “other” owners of the business.

The Bottom Line

This is an inflection quarter for Salesforce. As the stock has for years been plagued by consistent fears that shareholders would never really be rewarded for holding the stock, this quarter, that changes.

Echoing this insight, this is what Salesforce’s CEO Marc Benioff said on the call,

Improving profitability is our highest priority, and that really showed up this quarter. Our goal is to make Salesforce the largest and most profitable software company in the world, and that is what we are doing.

In short, Salesforce is determined to reach at least 30% non-GAAP operating margins by fiscal Q1 2025 (essentially within 12 months). For investors, this news is very welcome.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Strong Investment Potential

My Marketplace highlights a portfolio of undervalued investment opportunities – stocks with rapid growth potential, driven by top quality management, while these stocks are cheaply valued.

I follow countless companies and select for you the most attractive investments. I do all the work of picking the most attractive stocks.

Investing Made EASY

As an experienced professional, I highlight the best stocks to grow your savings: stocks that deliver strong gains.

-

- Deep Value Returns’ Marketplace continues to rapidly grow.

- Check out members’ reviews.

- High-quality, actionable insightful stock picks.

- The place where value is everything.