Summary:

- The current bear market presents great buying opportunities with low valuations and high dividend yields in the bank sector.

- The macro environment is ideal for diversified banks to grow their net interest income.

- Which of the 3 largest banks is the best buy at the moment?

sshepard

Investment thesis

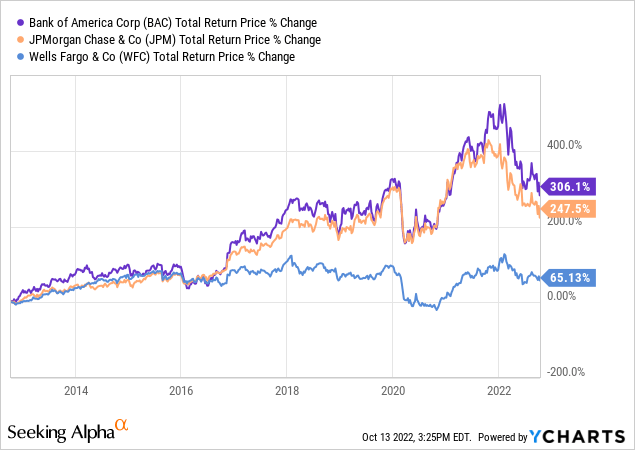

The article’s purpose is to compare the 3 biggest banks in the U.S. and give an idea for investors what to expect in the upcoming months and years. The banks are dropping their third quarterly results and I will mention the most relevant parts in the article. Diversified banks’ industry stocks have been declining just like the whole market in 2022. JPMorgan Chase & Co. (NYSE:JPM) has been declining for 13 months, Wells Fargo & Company (NYSE:WFC) has been on the decline for 8 months and Bank of America Corporation (NYSE:BAC) stock has been declining for 8 months after a short peak in February 2022. The decline pushed dividend yields to record highs with attractive company valuations. So the question is: is it time to buy diversified banking stocks despite further recession fears or better to wait for now so investors can expect better valuations in the near future?

Highlights of JPM, BAC, and WFC

JPM

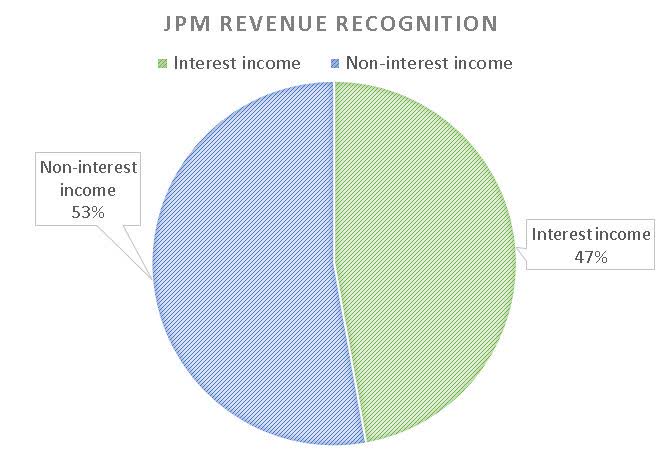

JP Morgan is the largest U.S. bank and has been for more than 10 years. Its net revenue reported grew by 1% in the second quarter year-on-year but the expense also grew by 6%. The third quarter results were much more positive, revenue growth was 6.5% compared to the second quarter and non-interest expense only grew by 2%. The provision for loan losses has been growing since the start of 2022. Investors have been looking closely at loan loss reserves and CIB revenues in the third quarter. Provision for loan losses increased by 39.6% in the third quarter compared to the second quarter but seemingly it did not have a huge impact on the bank’s net income. The lion’s share (three-quarters) of JPM’s CIB segment is coming from its markets and securities services. This segment did not perform well in the third quarter but the losses were compensated in the investment banking segment. Investment banking fees were down by 50% in the second quarter, by the end of this quarter they could grow by 25% but were still down year-on-year by 18%. Looking at the big picture investment banking segment is only responsible for a quarter of the bank’s larger Corporate & Investment Banking group. In terms of the consumer banking segment, home lending, card & auto loans are also under pressure due to dropping consumer confidence and rising interest rates. Home lending was still down in Q3 but card and auto loans could grow compared to the previous quarter. CB segment is fairly good despite the non-interest expense being significantly higher than a year ago due to interest rate hikes. On the other hand, rising interest rates have a great advantage on the bank’s NII. Its NII is up by 21% Q-o-Q and 26% Y-o-Y basis. As the external economic factors suggest that the NII will grow further in the fourth quarter. The management suspended share buybacks in Q2 so in the third quarter, there were no buybacks only dividend cash returns to investors.

The table is created by the author. All figures are from the company’s financial statements.

I think JPM is much more innovative than its peers in many ways. If we look at that despite Jamie Diamond is one of the strongest critics of digital assets, JPM was one of the first major banks to offer crypto funds to investors because there was major client demand for it. They were also one of the first major banks to launch a Bitcoin ETF. From an income investor’s point of view, they were the first ones to increase their dividend after the financial crisis of 2008 (more on that later in the dividend comparison). In addition, there is no doubt in my mind about their stability because even in the darkest days JPM was the only big US bank that did not require government assistance and the bank was also profitable even in 2008 and made the fastest recovery following the financial crisis.

BAC

BAC remains one of Warren Buffett’s top holdings with over 10% share in Berkshire’s portfolio and it is the second largest holding after Apple. The new management made a very strong commitment after the financial crisis that they want to achieve responsible growth and keep the bank’s risk profile under control. I believe they succeeded and the numbers tell the same story. While in 2009 they had a huge exposure to risky loans and generally high default loan types by 2022 the management lowered the share of home equity, construction loans, and credit card loans in the total loan portfolio. Not surprisingly, the non-performing loan ratio also dropped significantly by 2022. The average U.S. non-performing loan ratio is 1.2% and BAC has a non-performing loan ratio of approximately 0.6%.

Bank of America’s asset quality began to worsen in the second quarter as economic risks such as inflation, a more aggressive interest rate hike, and slowing economic growth occurred. The record inflation continues to put pressure on the bank’s consumer credit division and it seems this will not ease until the first half of 2023.

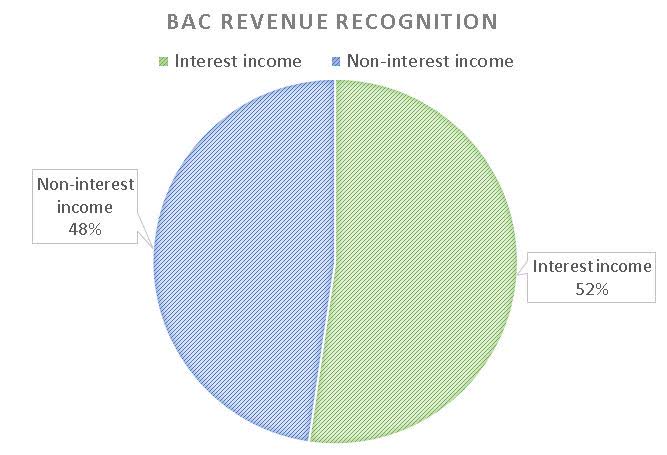

The bank has great deposit-gathering capabilities and they also have a strong corporate banking footprint. Among the banks, in the second quarter, total deposits declined but BAC’s second quarter total deposits decline was slightly less than JPM’s and WFC’s. The bank’s revenue is almost split in half into interest income and non-interest income segments. The interest income segment will deliver superior results as interest rates rise and the profit margin will widen despite the rise in interest expenses. Investors saw that as interest rates started to increase in the second quarter, BAC reported a noticeable increase in its NII. I expect the same to happen in its third and fourth quarter results. The non-interest income will suffer a bit more especially if the bear market continues for a longer period.

The table is created by the author. All figures are from the company’s financial statements.

WFC

Warren Buffett likes to have exposure to the banking sector. Since the 1990’s he always had some exposure to diversified banks, at some point, it was a quarter of his portfolio. He owned Wells Fargo for a long time until recently. Despite the financial crisis, he grew its share in Wells Fargo up until the second quarter of 2016. At that point, 24% of Berkshire Hathaway’s total portfolio was in WFC. Interestingly he switched from WFC to BAC. From 2016 until 2020 the share of WFC declined below 5%, then by the beginning of 2022, he sold all of his remaining shares, and at the same time, he gained more exposure to BAC.

What sets Wells Fargo apart from its peers is its large branch network. Just as a comparison, JPM with consolidated assets of $3.48 trillion has approximately 4800 branches and Wells Fargo with consolidated assets of $1.76 trillion has 4700 branches. This has resulted in two big advantages over the years. They are a well-established brand across the middle-market space and this large footprint also gives WFC good deposit growth potential among customers.

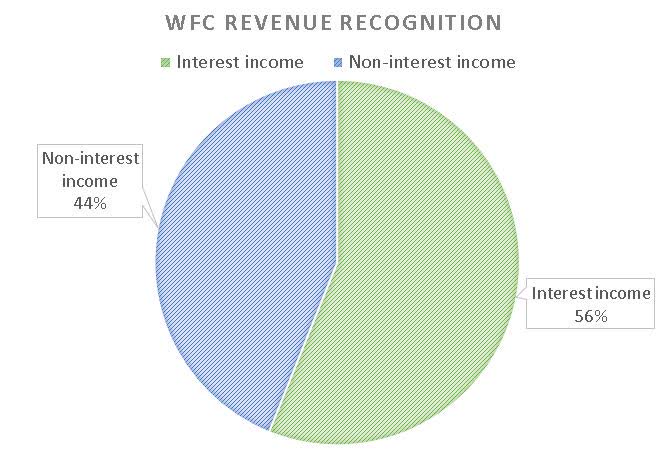

The company managed a successful rebranding in 2018 when they emphasized that WFC is an old-time bank you can trust with your money and they are on the “people’s side”. However, looking a bit deeper WFC is just like JPM or BAC. They have an interest-bearing segment and a massive non-interest income segment but they indeed have the largest share of interest income in their portfolio among the 3 banks compared to the non-interest income segment.

The table is created by the author. All figures are from the company’s financial statements.

The bank delivered mixed results in the second quarter but great results in the third quarter. The bank reported robust EPS growth and good revenue growth (18.6% Q-o-Q growth in NII) which was fueled by the high-interest rate environment. The bank is in a multi-year transformation and it seems they are in the middle of it. This is why I think among the 3 banks it would rank the weakest at the moment. However, if the transformation is successful and the management can meet its goals such as the efficiency ratio dropping below 60%, CET1 growing as expected, etc. it can be a good choice for investors. In addition, Main Street banks could outperform Wall Street banks in the short term because of the decline in capital markets and investment banking business. This is exactly what we are seeing in the third quarter earnings results. JPM, WFC, and USB outperformed the expectations, and Morgan Stanley (MS) and the other investment banks have underperformed and will underperform the previous expectations.

Quick macro outlook

Inflation was 8.2% in September, slightly worse than the expectation but the trend seems to be heading in the right direction and the peak was in June at 9.1%. Most of the market thinks that inflation will be slightly below 8% by the end of the year and it will return to normal levels by the end of 2023. If that is the case the Fed will likely go for 2 rate increases this year and possibly 1 or 2 at the beginning of 2023 then the rates will stay on those elevated levels until they see a clear sign that inflation is steadily on the decline. This will put pressure on banks due to sky-high mortgage rates and lower lending volumes. However, because of the strong job market, low unemployment rates, and good wage growth, I do not believe that loan defaults will increase significantly.

The risk factors are almost identical to all of the 3 banks. If the economy falls into a deep and long recession the banks cannot avoid credit losses and an interruption in earnings momentum. Investment banking and most of the non-interest segments are already seen some contraction in 2022 but if the inflation remains sky high and the fed needs to push interest rates above 5% that will significantly hurt not only the non-interest segments but the lending businesses as well. Some banks are preparing for the worst-case scenario like JPM and setting aside tons of money as “cash cushions” and some are just doing what needs to be done and do not worry much about cyclical banking.

Valuation comparison

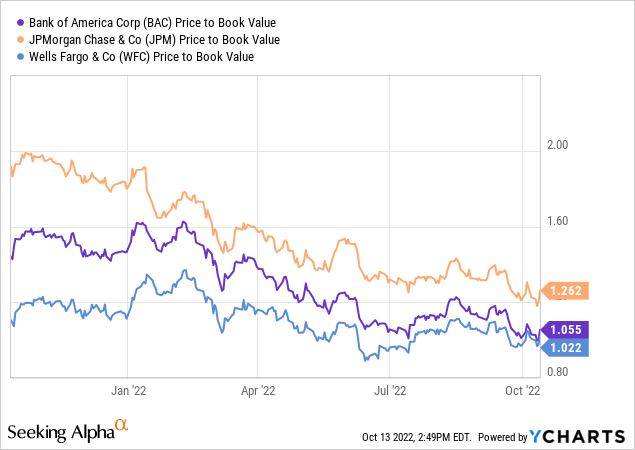

All of the banks are well-capitalized. Their CET1 ratios are above the criteria by a hefty margin. Warren Buffett has a great definition of return on assets. If a bank earns 1% on its assets it should trade at 1x its book value. If a bank earns less than 1% it should be trading below its book value and if a bank earns more than 1% on its assets it can be traded above its book value. JP Morgan has a return on assets of 0.97% and is currently trading at 1.26x its book value. Bank of America has a ROA of approximately 0.84% and it trades at 1.06x its book value. Wells Fargo has a ROA of roughly 0.85% while trading at 1.02x its book value. In this context, all three banks are trading roughly a bit over the price levels comparing their ROA and they are slightly overvalued. Based on this concept, JPM could be a fantastic buy at $83.8 or below, BAC at $25.2 or below, and WFC at $35.3 or below. These figures are 16-20% lower than their current trading prices. I do not believe we will see such great valuations only if a major recession will occur and the unemployment numbers start to rise significantly in addition, inflation starts to rise again and hits 10%+.

Let’s have a quick look at the banks’ beta. This is how I often measure the market downturn risk. The larger the beta, the worse the stock will perform during a bear market. The safest choice is JP Morgan based on a 5Y monthly beta because they stand at 1.07 while BAC is at 1.36 and WFC is at 1.13. In terms of efficiency and return on equity JPM still leads. JPM has an efficiency ratio of 60.8% while BAC is lagging with 61.65% and WFC with 70.54% as of July 2022. JP Morgan has a 3% lead on ROE (ROE: 12.87%) on Bank of America (ROE: 9.85%) and a 4% lead on Wells Fargo (ROE: 8.88%). This puts JPM in a good position to outperform its peers and continue to produce great long-term returns.

Banks and other corporations like to boost their EPS and their shareholder returns with share buybacks. However, JPM stopped its share repurchase program for now but in the last 3 years, it bought back approximately 7.7% of its shares. To put it into context, BAC reduced its shares outstanding by 12.1% and WFC by 11%. If investors look at the 3 banks’ P/E ratios JPM is the winner again but BAC is very close to first place. I like to look at the P/E ratios compared to their average because I found that I can get a clearer picture of when the stock is undervalued. JPM trades 30% below its 5-year average P/E ratio and BAC trades 28% below its 5-year average. WFC is not in the game with only 13.5% below its 5-year average P/E ratio. Looking at the price return of the last 10 years the winner is BAC but calculating the dividends JPM is just slightly behind.

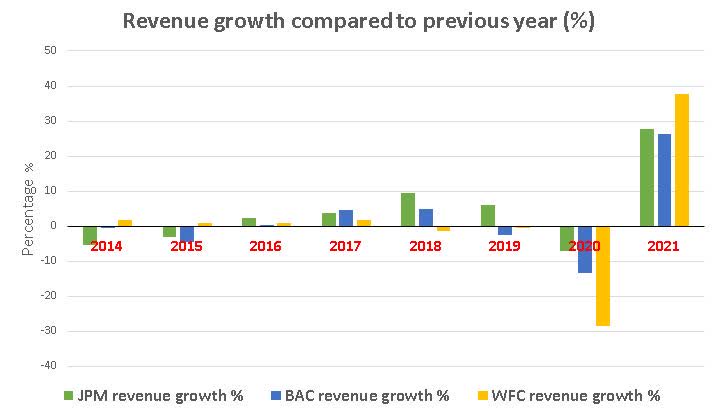

Last but not least if investors compare the bank’s revenue growth some interesting trends are unfolding. In normal market conditions, usually JPM outperforms BAC and WFC by growing more and declining less year-on-year. But in 2021 due to extremely beneficial external factors, WFC overwhelmingly outperformed both of them.

The table is created by the author. All figures are from the bank’s income statements.

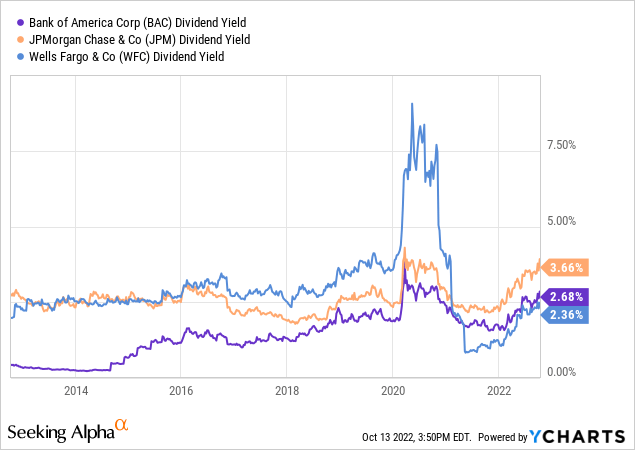

Dividend comparison

Banks have been reliable dividend payers prior to the financial crisis and now they are trying to build back that reputation. JPM had the fastest dividend recovery after the 2008 crash and its 2009 dividend cut. In Q2 2011 they raised the dividend from $0.05 to $0.25 per share. At the same time, BAC only raised its dividend in the third quarter of 2014 (5 years after the cut). However, WFC also raised its dividend in the second quarter of 2011 but it was “only” a 140% increase while JPM increased its dividend by 200%.

All of the banks highlighted during the last 2-3 months that their intention and cash return to shareholders have not changed. JPMorgan’s CFO said: “if you drop into the regulatory buffer zone, you’re subject to a 60% restriction, which based on our recent historical net income generation still gives us like ample, ample capacity to pay the dividend”. Bank of America’s management is also dedicated to returning cash to investors. Its CEO said: “Along the way, we believe our expected earnings generation over the next 18 months will provide an ample amount of capital, which allows us to support customer growth, and pay dividends”. Wells Fargo has almost the same opinion about dividends: “But as Charlie highlighted, the recent stress test results confirmed our capacity to return excess capital to shareholders through dividends”.

All of the 3 banks’ dividends are well covered for the upcoming years even in a case of earnings decline, WFC has the lowest payout ratio of 21.5% and JPM has the highest, 32.5%. In addition, in the next 1-3 years, dividend growth will likely be strong, especially for WFC with an expectation of over 14% dividend increase per year. (This large figure is due to their 2020 dividend cut and they have a lot of room for improvement.) But JPM’s 4.1% expected growth per year and BAC’s 6.7% growth are still good especially because they already have a higher dividend and did not make cuts since 2008.

Investor takeaway

In my opinion, the next months will be challenging for investors, and banking stock can easily see an 8-10% decline. But when central banks switch to new money-printing, stop raising interest rates and bank liquidity appears, the banking sector will be a massive winner, especially during the early stages of the next bull market. This is a great time for investors to get exposure to the banking sector on low valuation with great yields and for those who already have positions to add further positions at discounted prices. But to give you a final order for the three biggest banks I would give JP Morgan first place, Bank of America second place, and Wells Fargo third place on the “top banks to invest in right now” list. What are your 1st 2nd and 3rd place and why?

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in JPM over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.