Summary:

- Adobe is a diversified technology company that owns a variety of digital media, data, and experience applications.

- The company reported strong financial results for Q1,FY23 as it beat both revenue and earnings line growth expectations.

- Adobe is poised to benefit from a series of intersecting growth trends from the growth in digital “creators” to the Metaverse with its Substance 3D.

- Over two-thirds of movies at the Sundance film festival as well as many Oscar-winning movies (Star Wars, Spiderman, etc.), used Adobe products in their creation.

- The company bought back 5 million shares in Q1,FY23, and has ~$5.2 billion remaining of its $15 billion authorization.

I going to make a greatest artwork as I can, by my head, my hand and by my mind.

Adobe (NASDAQ:ADBE) is one of the world’s most highly regarded technology companies. The business created the PDF file format back in 1993 and has since become an industry-renowned leader in its creative products namely photoshop, premiere pro, etc. However, Adobe is not just a one-trick pony, the company is highly diversified and has gradually expanded its product range through acquisitions and development. I believe the company is now at the intersection of various growth trends from the rise of the creator economy to “big data”, digital signatures, and even digital customer journeys. So far, Adobe has been executing well and the company reported strong results for Q1,FY23, beating both top and bottom-line growth estimates. In this post, I’m going to break down its financials and growth trends, before revealing my valuation model and forecasts for the company. Let’s dive in.

Solid Financials and Leadership

Adobe reported solid financials for the first quarter of the fiscal year 2023. Its revenue was $4.66 billion, which beat analyst estimates by $30.2 million and increased by a solid 9.22% year over year or 13% on a constant currency basis. Its Digital Media segment contributed to 73% of total revenue or $3.4 billion and increased by a solid 14% YoY on a constant currency basis, while $307 million in net new ARR was added in the quarter to reach a solid $13.67 billion. This highlights the large pipeline of revenue, that is driven by Adobe’s subscription model, which is one of my favorite types of payment models, due to its relative consistency. Its earnings per share [EPS] was $2.71, which beat analyst forecasts by $0.06, which was positive.

Adobe financials (Q1,23)

Adobe’s Digital Media segment can be further divided into two sub-sections. This includes its Creative Cloud and Document Cloud. The Creative Cloud is what Adobe is most known for. This includes its industry-renowned applications such as Photoshop (images), Illustrator (graphics), Premiere Pro (video), etc. Various review websites online indicate Adobe Premiere Pro as the “best software” for professional video editing. In addition, Adobe’s own website says that “over 90%” of creative professionals use Photoshop, which would not surprise me.

The beautiful thing about Adobe is they were a pioneer in the industry and its software is deeply embedded into the education system, which I believe is a competitive advantage. As students are taught the software, they build skills that are then in line with the industry. This creates a virtuous cycle of Adobe-focused students and industry professionals who don’t want to learn how to use a new tool. Now, of course, Adobe is facing 10X more competition than in prior years from free tools such as Da Vinci Resolve (which I use myself for video editing) as well as freemium graphic design tools such as Canva, but I will discuss more about those in the “Risks” section.

Back to the financials, Adobe reported solid growth in its stock photo service as well as its stock 3D model service called “Substance” & Augmented Reality [AR] service. I believe these parts of the business are poised to benefit from the forecasted growth in the Metaverse, which is expected to grow at a rapid 47.2% CAGR and reach a value of $426.9 billion by 2027. The “Metaverse” is really an extension of 3D modeling/graphics, combined with AR and VR. Therefore, Adobe is poised to help enable this service.

Adobe 3D assets (Adobe Author Research)

Adobe’s Substance 3D is already used by major brands such as Burberry (OTCPK:BURBY, OTCPK:BBRYF), Louis Vuitton (OTCPK:LVMHF, OTCPK:LVMUY), and Amazon (AMZN). In addition, the platform was used in the development of major movies such as Spider-Man, Star Wars, and Blade Runner 2049. In fact, the head of texturing at Warner Bros. (WBD) even details exactly how he used Adobe’s software to create a cyberpunk-style view of Las Vegas and a Solar Farm used in the Blade Runner 2049 movie. In my mind, this is a testament to Adobe’s industry-renowned leadership.

Blade Runner 2049 flying car over solar farm (Adobe Substance 3D)

Adobe also reported strong growth in Frame, which is a collaborative video editing platform acquired for $1.1 billion in August 2021. I believe this was a solid acquisition as video collaboration is a challenging task. As a Digital Marketing Director, I used to manage a team of videographers who would often struggle to track and record video edit changes with the client, Frame solves the issue. In fact, a study by Adobe (cited) by HubSpot (HUBS) stated the creator economy added over 165 million people between 2020 and 2022, which was a huge 119% increase. More creators mean more video and thus Adobe is poised to benefit. Of course, a large portion of videos are recorded via the smartphone, but for professional videos or YouTube, often professional software is required. In addition, Adobe developed the Lightroom Mobile application, which is the default “high-end” photo editor for Samsung Galaxy S23 series.

On the audio front, I particularly like the Adobe Podcast feature, which effectively used “AI” to make any recording sound like yours in a podcast studio, which is incredible. Often, if you record a podcast or video in a standard room, it will sound “tiny” or have “echo”. Usually, this would require an editor to do post-production editing, which can be time-consuming.

Podcasts have become an immensely popular medium and the industry is forecast to continue its growth at a rapid 18.4% CAGR, up until 2030. Adobe is poised to benefit from this trend, and in Q1,FY23, it won major customers such as Disney (DIS), IBM (IBM), Accenture (ACN), BBC, and Nintendo (OTCPK:NTDOY, OTCPK:NTDOF).

Document Cloud Growth with e-Signature Tailwinds

The Document Cloud is the second part of Adobe’s Digital Media segment. This includes its famous PDF file format and various signature solutions. In Q4,22, its Document Cloud generated revenue of $634 million, which increased by 13% year over year. This was driven by the strength of its signature solution Acrobat Sign, which was popular among both SMBs and the enterprise. This doesn’t surprise me given digital signatures are a growing industry and I personally get offended when asked to print, pen sign, scan, upload, and send a traditional document. It just feels barbaric (first world problems). Either way, competitor DocuSign (DOCU) has an $11 billion market cap, which gives you an indication of the scale of the opportunities. In Q1,F23, Adobe won major customers such as Samsung (OTCPK:SSNLF), Verizon (VZ), JPMorgan Chase (JPM), etc.

Digital Experiences Growth

Adobe second major segment is its Digital Experiences, which generated $1.18 billion or 25% of total revenue in Q1,FY23. This was driven by Adobe’s real time customer data platform [CDP], as well as its Journey Optimizer. Given the rise of “big data”, companies are looking to break down data silos and unlock new insights about their customers. Adobe’s CDP basically solves this issue. In addition, its overall Experience platform was rated as the number one leader by Gartner Peer reviews. In Q1,FY23, the platform scored major customer wins such as Costco (COST), Paramount (PARA, PARAA), S&P Global (SPGI), IBM (IBM), and many more. I believe Adobe also has a strong cross-selling opportunity across all its platforms. For example, a company can use its Creative Cloud to create digital content and then utilize the CDP and Journey Optimizer to tailor personalized content to users no matter where they are in the buying cycle. This is a marketer’s dream as “hyper-personalization” is the holy grail.

Valuation and Forecasts

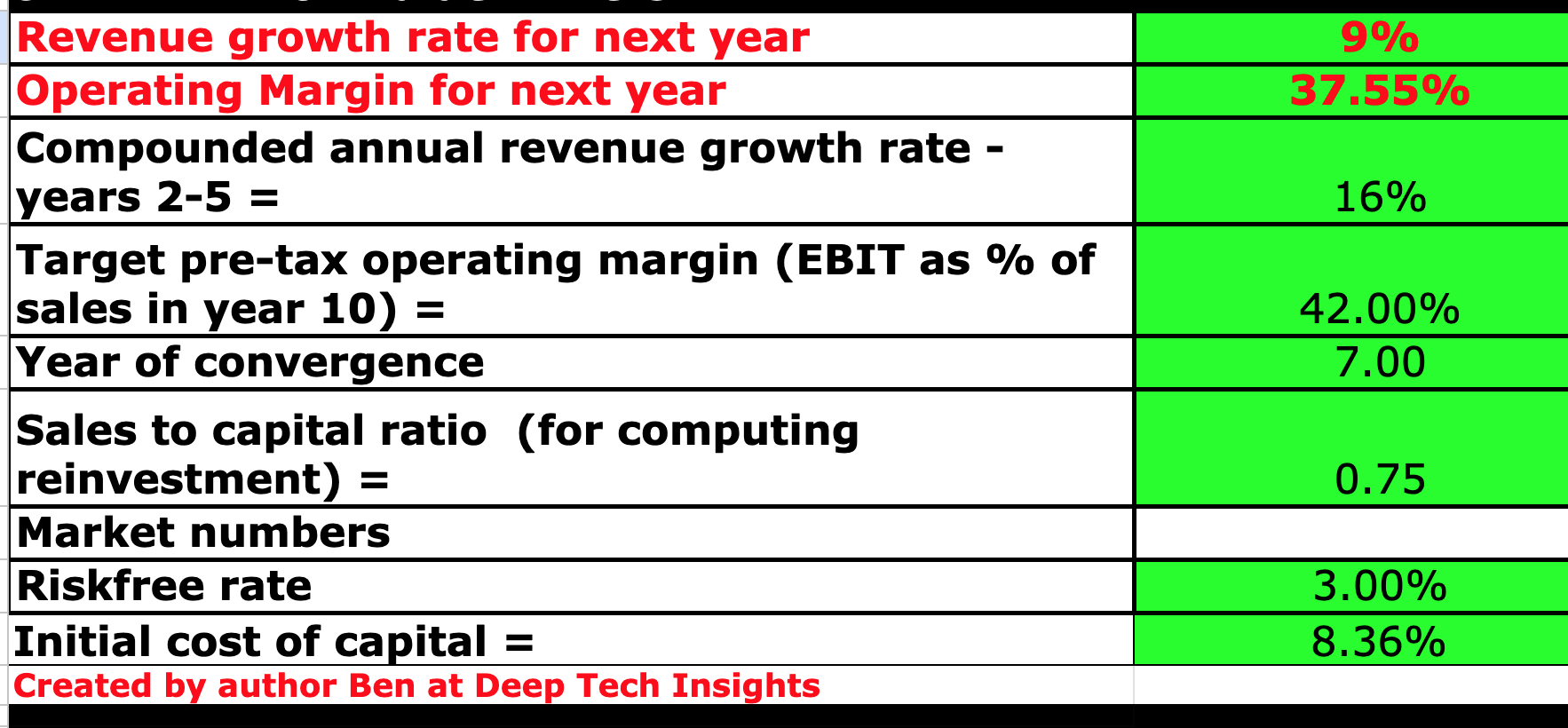

In order to value Adobe, I have plugged its latest financial data into my discounted cash flow valuation model. I have forecast 9% revenue growth for “next year” or the next fourth quarters in my model. This is based upon the $4.75 billion to $4.78 billion guidance for Q2,FY23, which I have extrapolated out for the next four quarters. It should be noted this is a similar growth rate to the 9.22% reported in Q1,FY23 and thus seems fairly logical, if the current growth trends continue. In years 2 to 5, I have forecast a faster 16% revenue growth, which may seem optimistic but is still below the 22% growth rate achieved in 2021 and thus I deem this to be achievable. I expect this to be driven by improving economic conditions, and continuing growth trends across digital media, documents, and the creator economy.

Adobe stock valuation 1 (created by author Ben at Deep Tech Insights)

To increase the accuracy of my model, I have capitalized R&D expenses, which has boosted net income. I have forecast a pretax operating margin of 42% over the next 7 years. This is fairly optimistic but I expect this to be driven by increased operating leverage from its products, as well as increased multi-platform purchases across the enterprise customer base.

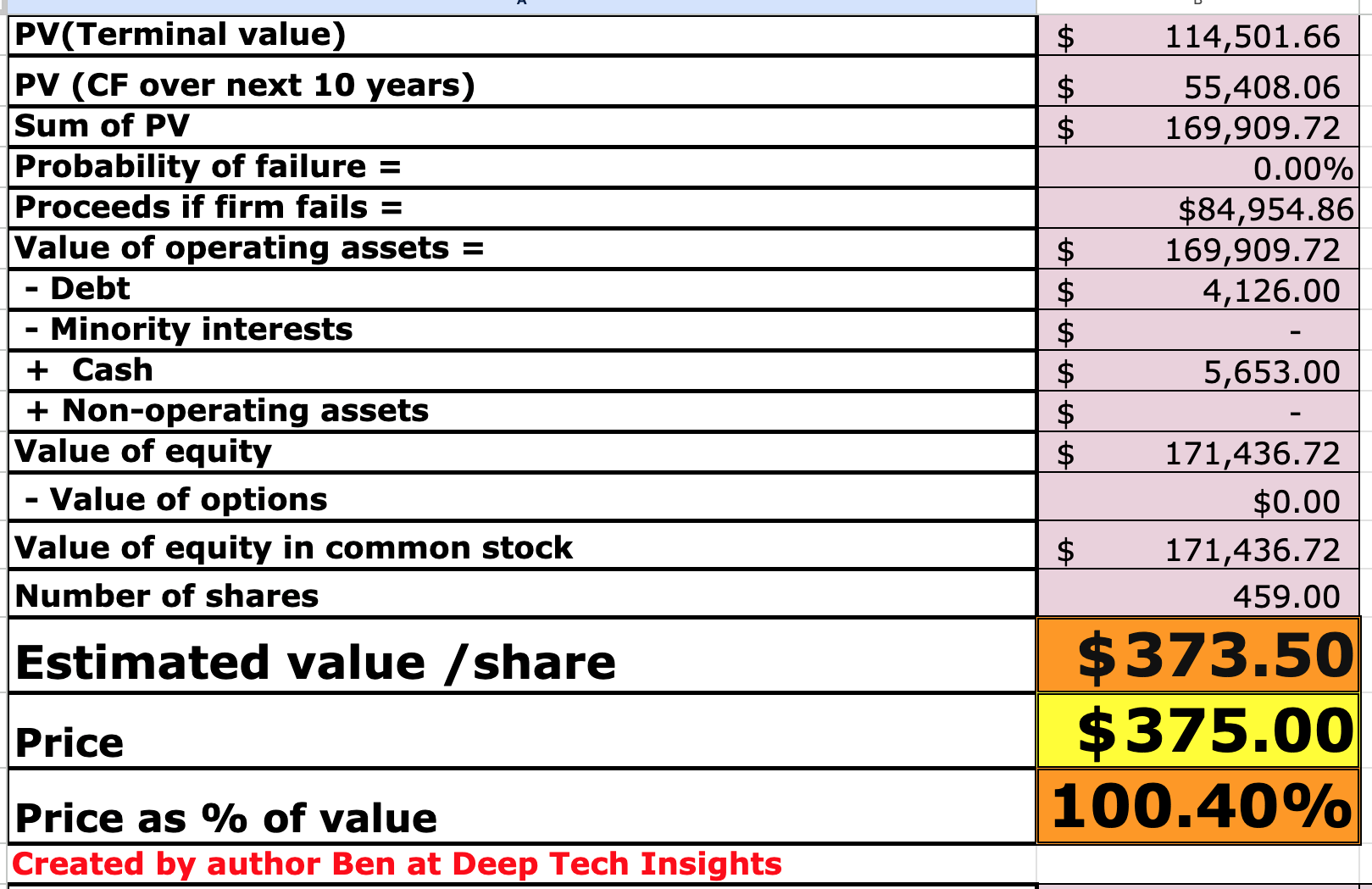

Adobe also has a strong balance sheet to continually invest with cash and short-term investments of $5.65 billion. The company does have total debt of $4.1 billion, but the vast majority of this ($3.6 billion) is long-term debt and thus manageable.

Adobe stock valuation 2 (Created by author Deep Tech Insights)

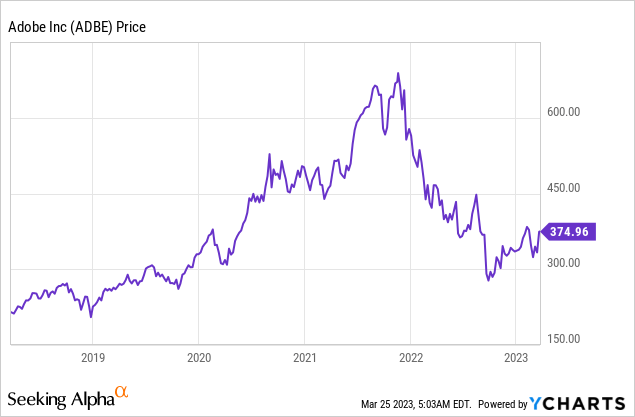

Given these factors, I get a fair value of $373 per share, which is close to where the stock is trading at the time of writing. Therefore, I will deem ADBE stock to be “fair value” due to the high quality of the company and its strong leadership position.

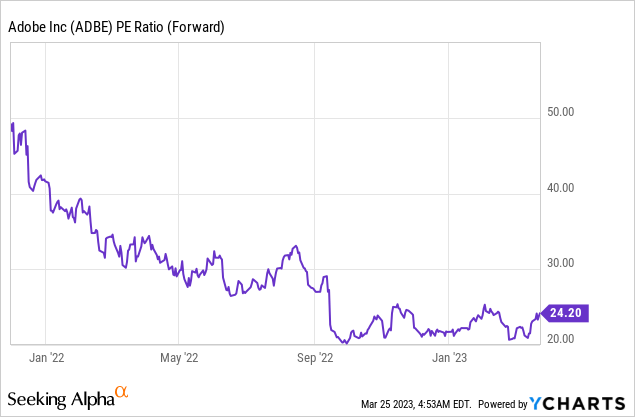

Adobe also trades at a forward P/E ratio = 34, which is ~28% cheaper than its 5-year average.

Risks

Competition

As mentioned prior, Adobe faces more competition than ever. On the photo editing side, there are various free mobile apps and online applications (Canva, etc.). In video editing, the company faces competition from Apple’s (AAPL) Final Cut Pro, as well as free platforms such as Da Vinci Resolve, which I personally find to be valuable. On the digital marketing front, its Marketo automation tool competes with the Salesforce marketing suite (CRM), HubSpot, and many more. The only silver lining is the market has expanded (as cited by my previous industry report links) and thus the pie has gotten larger for everyone.

Final Thoughts

Adobe is a tremendous company and a true leader across the digital media industry. The company is in a prime position to benefit from a series of intersecting trends and has been executing exceptionally so far. The company will face challenges as it aims to balance providing a “gold standard” service with a reasonable price point for the average consumer, as competition is more fierce than ever. Given my valuation model and forecasts indicate ADBE stock is “fair value” at the time of writing but not exactly “cheap”, I will label it as a hold as prudent investors may wish for a pullback before entry.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.