Summary:

- HD is a solid company that has been riding a strong repair and remodel market.

- The R&R market should remain solid, but growth is expected to start to decelerate.

- Meanwhile, the company faces inflationary wage pressures and deflationary lumber price headwinds.

Justin Sullivan/Getty Images News

While Home Depot (NYSE:HD) is a great company, the stock appears overvalued in a higher interest rate world. Meanwhile, it is facing both inflationary and deflationary pressures with labor and lumber, respectively.

Company Profile

HD is the world’s largest home improvement retailer by sales. The company sells a variety of items including home improvement products, tools, building materials, lawn & garden items, repair & maintenance, and home décor. Its big box stores typically stock between 30,000 to 40,000 items in a year.

HD sells to both do-it-yourself and professional customers. It also offers installation services in a number of categories such as flooring, windows, cabinets, countertops, water heaters, sheds, and furnaces & central air.

At the end of fiscal, 2022, the company had 2,322 stores throughout the U.S., Canada, and Mexico. The company also sells its good through its e-commerce website. Approximately half of its online orders are fulfilled through a store.

Q4 Overview

For Fiscal Q4, HD saw revenue rise 0.3% to $35.8 billion. Same-store sales fell -0.3% both in the U.S. and overall. Transactions fell -6% in the quarter, while average ticket increased 5.8%.

The company said inflation increased the average ticket price by 15 basis points. However, lumber prices fell -50% year over year, hurting comps by -70 basis points.

HD’s strongest categories in the quarter were building materials, plumbing, millwork, hardware, tools, outdoor garden, and paint. Big ticket comp transactions were up 3.8%, showing strength in the high-spend Pro segment of its business.

Gross margins were 33.3%, up 7 basis points. OpEx was 20.0% of sales, up 32 basis points, hurt by litigation in California and a store fire.

Earnings were flat at $3.4 billion, while EPS rose 2.8% to $3.30.

FY2024 Guidance

Looking ahead, HD guided for flat revenue and same-store sales in fiscal year 2024 ending January. It’s looking for an operating margin of 14.5%, hurt by 60 basis points from wage inflation. EPS is projected to fall by mid-single-digits.

Discussing FY24 guidance on its Q4 earnings call, CFO Richard McPhail said:

“As we set targets for 2023, the context of the past 3 years led us to consider 3 factors that will likely influence our performance this year. First, the starting point for our target setting this year is our assumption regarding consumer spending. We’ve assumed, like many economists, that we will see flat real economic growth and consumer spending in 2023. Second, over the last 7 quarters, we have seen our transactions gradually normalize as consumer spending has shifted from goods to services. We believe that if this shift continues at its current pace, the home improvement market would be down low single digits. And third, as an offset to this pressure, we plan to continue to capture market share. Our competitive advantages, the investments we have made over many years and the unique advantage that our orange-blooded associates give us over our competition position us to take share in any environment.”

Opportunities and Risks

The state of the economy and subsequently the repair and remodel market are two big areas that are likely to impact HD in the coming years. On the economic side, consumers are obviously dealing with increased inflation and rising interest rates that can eat into buying power. This can hurt sales in more discretionary categories such as home décor, seasonal items, and law & garden.

At the same time, with higher interest rates and slowing home sales, the repair and remodel market can actually remain strong. Higher mortgage rates is likely to keep people in their homes longer, and can incentivize them to remodel. So if the economy can walk that fine line of not falling into a serious recession, the repair and remodel market could actually be pretty strong over the next few years. I’ve talked to several local contractors who’ve all indicated that their backlogs are pretty strong. For its part, the Remodeling Futures Program at the Joint Center for Housing Studies of Harvard University predicts repair and remodel growth in 2023, although for the pace to decelerate throughout the year.

Remodeling Futures Program at the Joint Center for Housing Studies of Harvard University

Inflation is another are that can impact HD. On the one end, it can drive up sales. However, the company is seeing some pretty intense wage inflation. As a result, HD will increase the wages of its front-line hourly workers by $1 billion in 2023 to retain and attract new workers. It said it will have no market with a starting wage under $15 and that the average wage will be well above $15.

One of the biggest areas of commodity prices that can affect the company is lumber prices. HD isn’t as exposed to lumber prices as a company like Builders FirstSource (BLDR), but it can still have a pretty meaningful impact on its numbers.

On its Q4 earnings call, HD exec said:

“Our guidance assumes that we’ll comp slightly lower in the first half than the second half. The lumber pressure we called out is sort of outside of guidance. There’s so much volatility in that, that we would not want to put that in guidance. There is 100 basis points of pressure to the year. If lumber remains at current prices, that pressure exists predominantly in the first half.

“It’s been a very turbulent couple of years in the lumber market. To give you an example of what we faced, in the fourth quarter on the framing side, lumber was $420 per thousand on average compared to $886 on average in 2021. To put that in retail dollar sense for everyone, a 2×4 stud, which is one of our top unit movers in the business, retail on average for $3.40 in the fourth quarter of this year. Last year, it was over $5. Now we did make some ground back on units. So you could say that when you see a lumber market depressed or normalized, you see good unit productivity and you see good overall project business. As you look forward into the front half, that same 2×4 stud was over $10. It’s now $3.50. So we’ll see good unit productivity and certainly an opportunity to drive more project-related business.”

Valuation

HD stock currently trades around 13x the FY2024 (ending January) consensus EBITDA of $25.8 billion and 12.7x the FY2025 consensus of $26.4 billion.

It trades at a forward PE of nearly 18x the FY24 consensus of $15.87.

Revenue growth is expected to be flat this year, and then grow around 3-4% a year over the next few years.

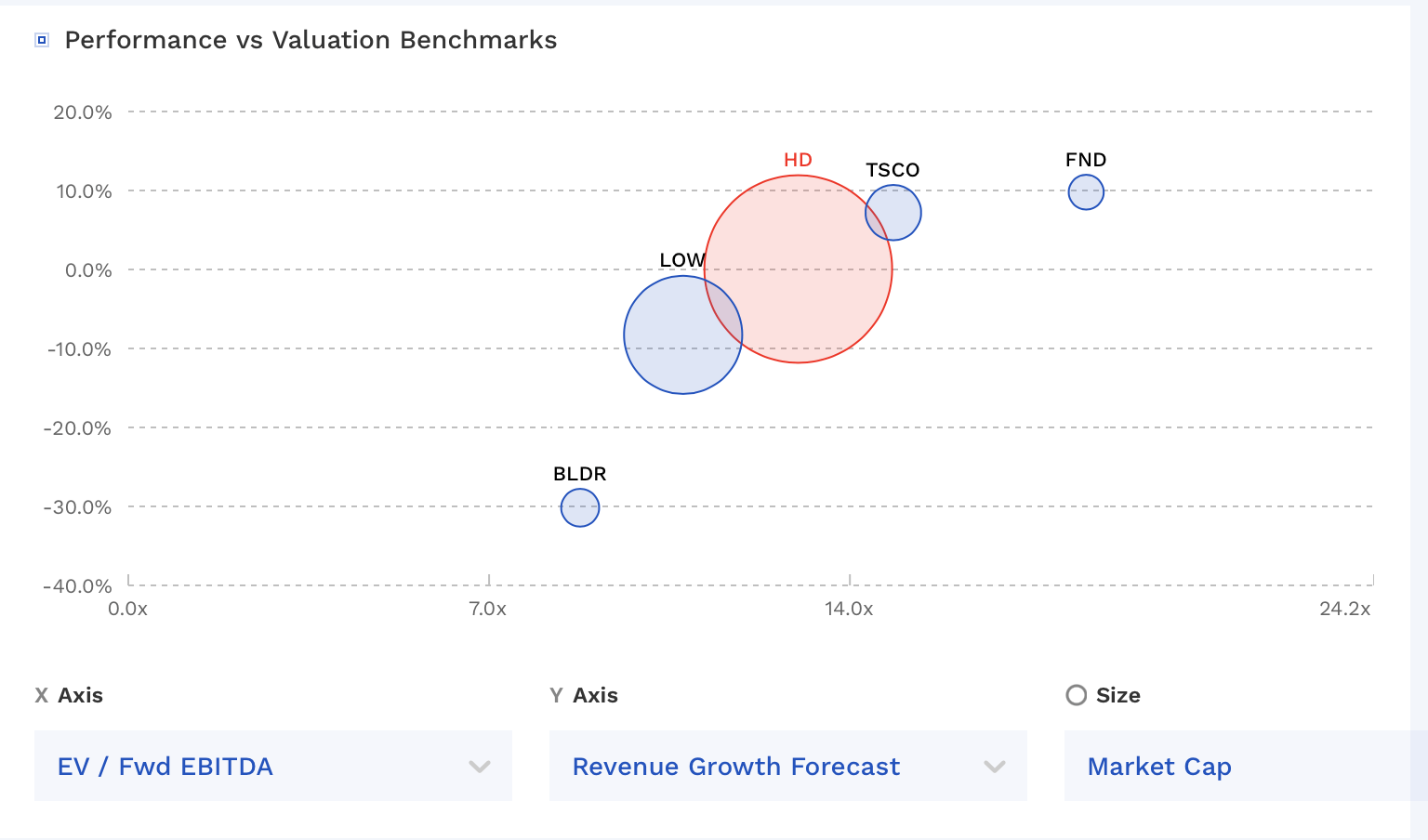

HD trades in the middle of its peer group and at a moderate premium to its closest rival Lowe’s (LOW). The company has generally traded at a premium due to its better historical performance and stronger ties to the Pro market.

HD Valuation Vs Peers (FinBox)

From a trailing EV/EBITDA standpoint, the stock is trading at a premium to where it has historically traded prior to the great recession.

HD Historical Valuation (FinBox)

Conclusion

HD has proven to be a great company over the years. During the past few years it’s ridden a nice remodeling trend, as people began to spend more time at home because of Covid and more remote work options. The trend could continue as more people stay in their homes due to high mortgage rates and a softening housing market, but economic softness is likely to cause this growth to decelerate.

That said, HD is a mature company that should grow at a pretty modest pace going forward. It’s trading at a premium valuation to where it traded pre-Covid, despite being in a high interest rate environment, which should make slower-growth companies less attractive given a higher weighted cost of capital (WACC).

As such, while I think HD is a solid company, I currently think the stock is overvalued.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.