Summary:

- Amazon’s stock is up +16% year-to-date despite losing ~12% since releasing its Q4 earnings report in early February.

- In this note, we will review Amazon’s latest quarter and try to figure out if the stock is a good buying opportunity during this pullback.

- Spoiler Alert: I rate Amazon a “Strong Buy” at $100, with a strong preference for staggered accumulation. Read on to find out why!

ipuwadol/iStock via Getty Images

Introduction

Amazon (NASDAQ:AMZN) and its big tech peers seem to have regained leadership of the market in 2023; however, Q4 results signal big trouble ahead for this pack as rich valuations face up against a massive growth slowdown and a vicious margin contraction.

Traditionally, technology companies (not stocks) have shown secular growth, i.e., less vulnerability to economic cycles. However, unlike 2007-08, technology is now ubiquitous, and big tech giants are severely exposed to economic cycles, as evidenced by the ongoing growth slowdown and earnings recession seen in their Q3 and now Q4 reports:

| Q3 Y/Y Revenue Growth (%) | Q4 Y/Y Revenue Growth (%) | Q3 Y/Y EPS Growth (%) | Q4 Y/Y EPS Growth (%) | |

| Apple (AAPL) | +8.14% | -5.48% | +4.03% | -10.48% |

| Microsoft (MSFT) | +10.60% | +1.97% | -13.28% | -9.09% |

| Amazon (AMZN) | +14.70% | +8.58% | -9.68% | -27.48% |

| Tesla (TSLA) | +55.95% | +37.24% | +97.92% | +57.92% |

| Alphabet (GOOGL) (GOOG) | +6.10% | +0.96% | -24.29% | -16.24% |

| Meta (META) | -4.47% | -4.47% | -49.07% | -52.48% |

Source: YCharts (Data as of market close on 3rd February 2023)

After showing signs of a potential growth re-acceleration in Q3, Amazon’s growth engine hit a snag once again last quarter. In this note, we will analyze Amazon’s Q4 results and determine its fair value. Furthermore, we shall look into Amazon’s technical chart to see if it is a good buy at current levels.

AMZN Stock Key Metrics

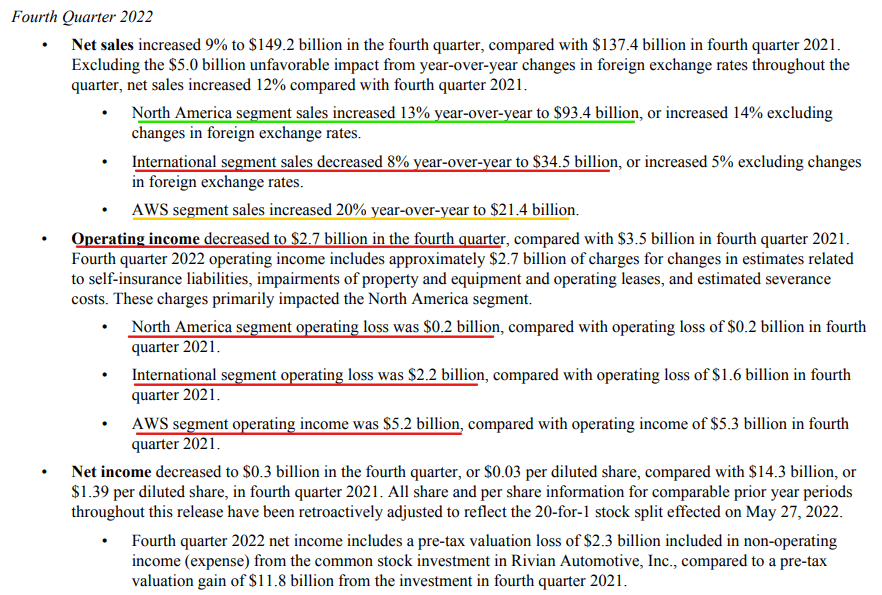

For Q4, Amazon reported revenues of $149.2B (up +9% y/y), beating street estimates by ~2.3%. While the revenue beat was solid, Amazon reported a big miss on earnings (EPS of $0.03 fell well short of expectations of $0.17) primarily due to restructuring charges and non-operating losses on its stake in Rivian.

Amazon’s Q4 2022 Earnings Press Release

Here’s what Amazon’s management had to say about this quarter:

Our relentless focus on providing the broadest selection, exceptional value, and fast delivery drove customer demand in our Stores business during the fourth quarter that exceeded our expectations—and we’re appreciative of all our customers who turned to Amazon this past holiday season. We’re also encouraged by the continued progress we’re making in reducing our cost to serve in the operations part of our Stores business.

In the short term, we face an uncertain economy, but we remain quite optimistic about the long-term opportunities for Amazon. The vast majority of total market segment share in both Global Retail and IT still reside in physical stores and on-premises datacenters; and as this equation steadily flips, we believe our leading customer experiences in these areas along with the results of our continued hard work and invention to improve every day, will lead to significant growth in the coming years. When you also factor in our investments and innovation in several other broad customer experiences (e.g. streaming entertainment, customer-first healthcare, broadband satellite connectivity for more communities globally), there’s additional reason to feel optimistic about what the future holds.”

– Andy Jassy, Amazon CEO

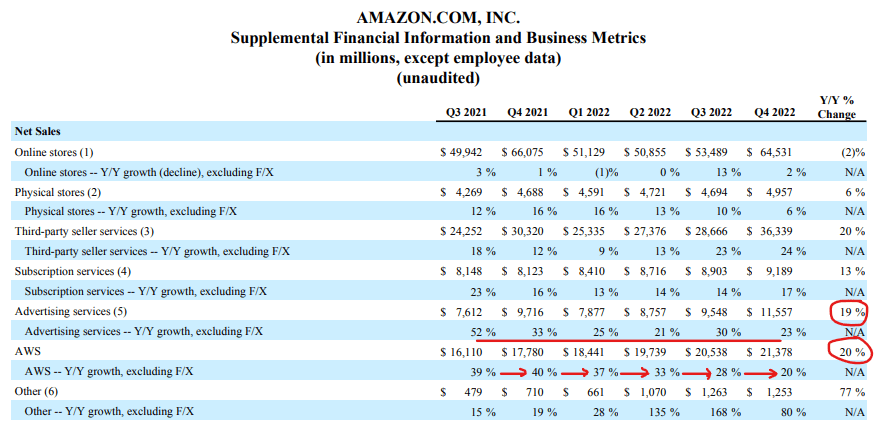

While Amazon managed to beat revenue guidance in Q4, the twin growth engine of AWS and digital ads is now hitting a snag as macro forces take a toll on these businesses. On the earnings call, Amazon’s management forecasted that AWS’s revenue growth is set to slow down to the mid-teens in Q1 2023 as enterprise demand wavers due to tough economic times. A usage-based model allows customers to scale up and scale down as required, and this dynamic could inflict a lot of pain on AWS (and other cloud infrastructure services providers like Azure and GCP) in the event of an economic contraction.

Amazon’s Q4 2022 Earnings Press Release

And as you may already know, Amazon’s e-commerce business is still normalizing after the pandemic boost. While I am not thrilled about the slowdown in Amazon’s Ads business, given the demand challenges faced by this industry right now, I think Amazon is doing quite well. With rivals such as Meta (META) and Alphabet (GOOGL) reporting shrinkage in advertising revenues, Amazon’s ads business just grew at ~19% y/y. Now, I understand that Amazon is starting from a lower revenue base; however, Amazon Ads is a $40B revenue run rate business by itself, and growing at this rate in such a dire macroeconomic environment while operating at such a scale is commendable.

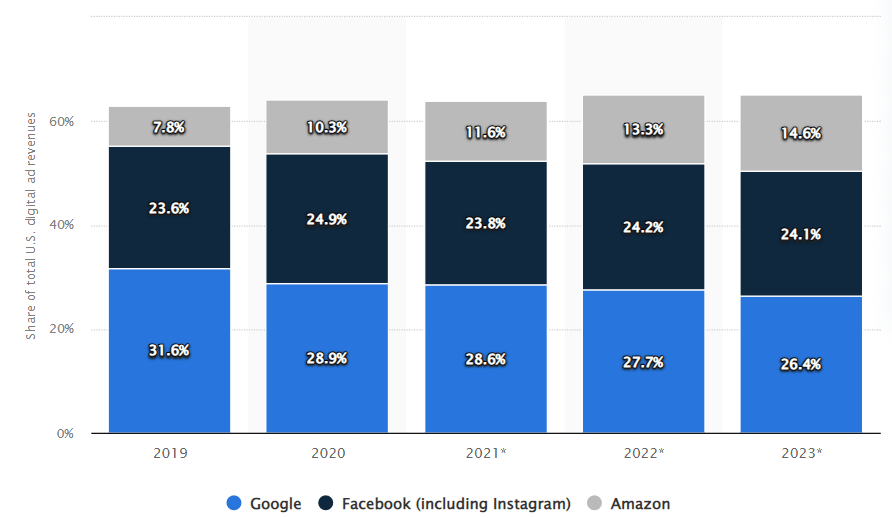

Over the last decade, Meta (Facebook + Instagram), Alphabet (Google + YouTube), and Amazon have formed a dominant triopoly in the digital advertising industry.

Oberlo & eMarketer

eMarketer

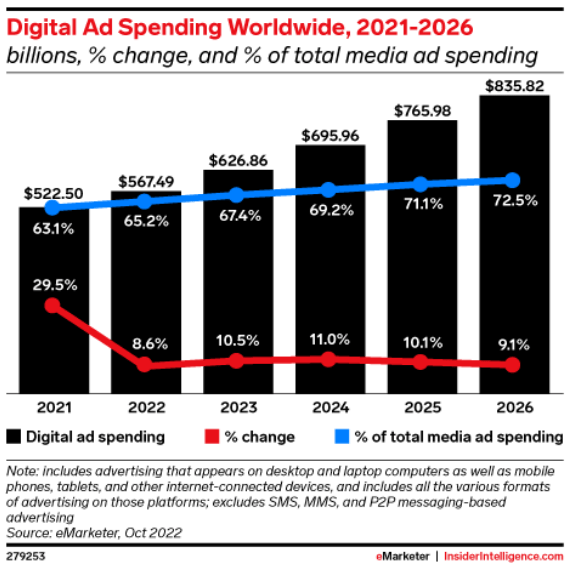

However, a weak macroeconomic environment is currently driving a drastic slowdown in digital ad spending. Concurrently, the digital ads industry is going through a sea change of disruption that ranges from Apple’s IDFA policy changes to the Internet becoming cookie-less. And now generative AI technology is threatening to change the entire landscape!

That said, from a positioning perspective, I believe Amazon Ads (and bottom-funnel advertising in general) will continue to win market share over top-funnel advertising, and thereby manage to deliver healthy compounded growth in the next few years.

Despite Amazon’s massive scale ($500B+ in annual revenue), it is barely profitable right now as the company is going through a heavy investment cycle. However, with revenue growth slowing down, investor skepticism around Amazon’s aggressive re-investments back into the business is growing, and rightly so.

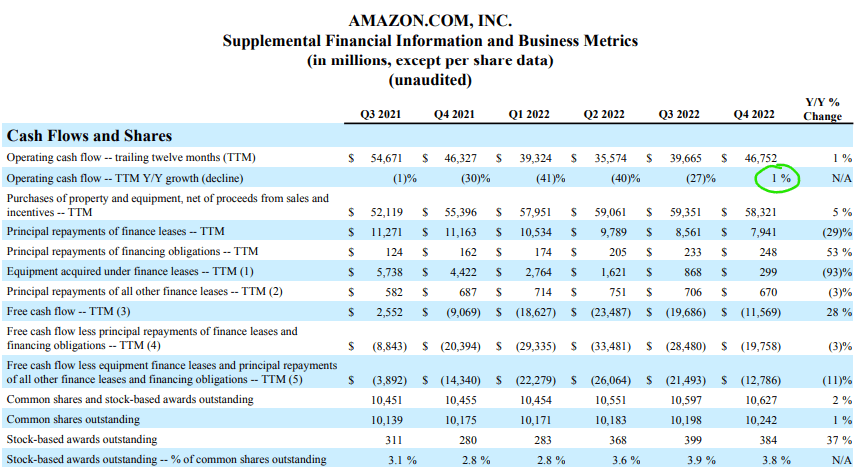

As I see it, management’s decision to reduce headcount by ~18K is a step in the right direction, but there’s still a lot more to do for Andy Jassy and his leadership team to bring investors back on Amazon’s side. The one notable positive from Amazon’s report was that the operating cash flow went up 1% y/y in Q4 2022, reversing a trend of significant declines.

Amazon’s Q4 2022 Earnings Press Release

Unlike its digital advertising rivals – Alphabet and Meta, Amazon doesn’t boast a net cash balance. However, I do not see any major cash burn issues for the retail-streaming-cloud-digital ads conglomerate, and having cash & short-term investments of ~$58B gives Amazon a comfortable liquidity cushion.

What Is The Long-Term Outlook?

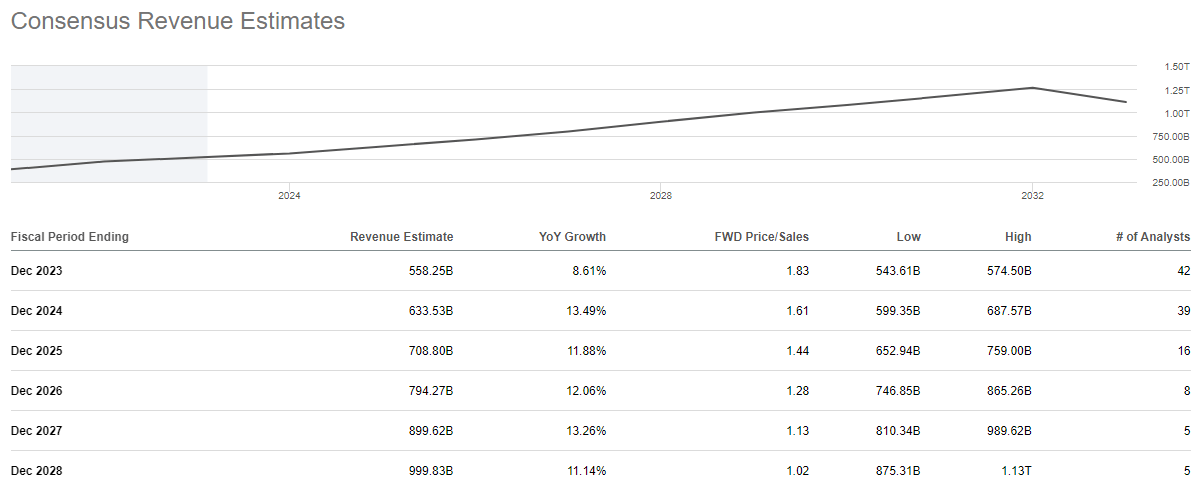

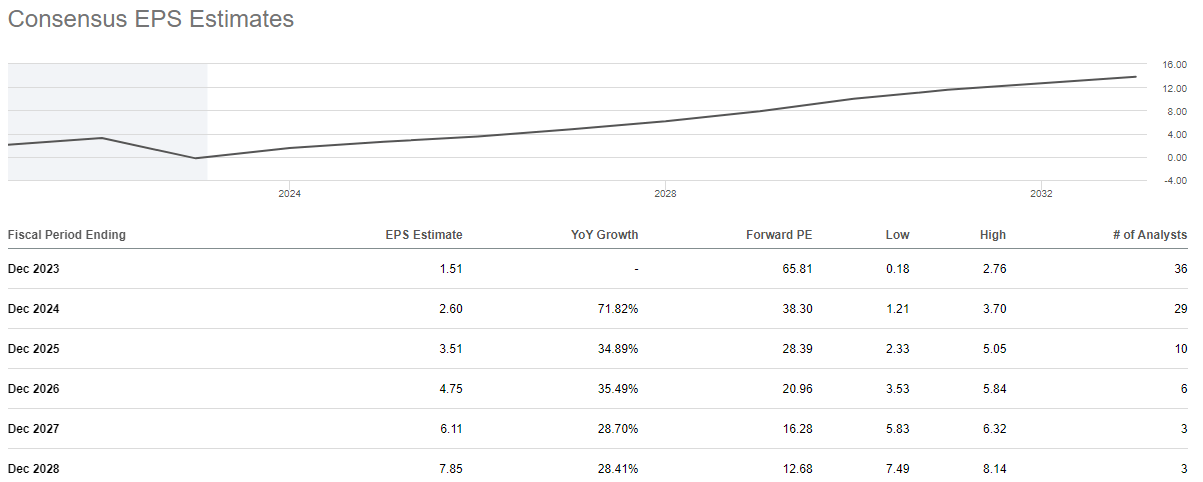

According to consensus analyst estimates, Amazon is set to deliver double-digit CAGR revenue growth over the next five years, with EPS set to turn positive [$1.51] in 2023 and then grow by ~5x in five years.

Amazon Revenue Estimates (SeekingAlpha)

Amazon Earnings Estimates (SeekingAlpha)

Clearly, Wall Street sees a bright future for Amazon, and I agree! As Amazon’s high-margin businesses (Cloud and Digital Ads) scale up further, and retail business improves operational efficiency; Amazon is set to turn into a giant free cash flow machine.

Is Amazon Stock Fairly Valued?

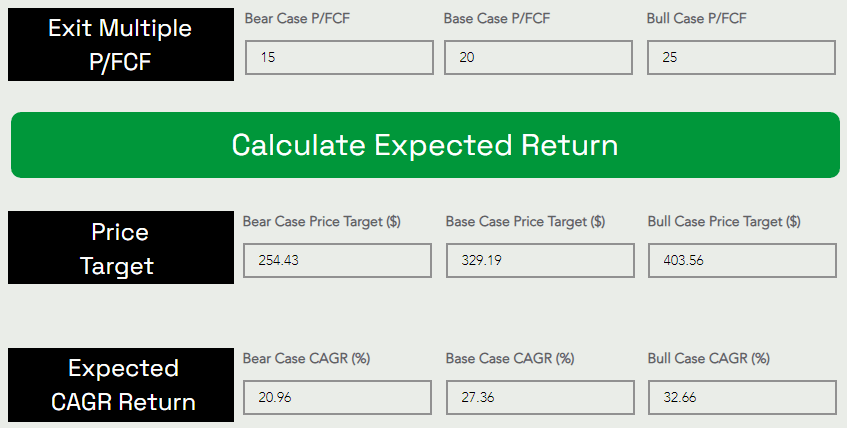

To answer this question, we shall utilize TQI’s Valuation Model with the following assumptions:

TQI Valuation Model (TQIG.org)

TQI Valuation Model (TQIG.org)

Summary of updates

- Old FV estimate: $151.36, New FV estimate: $141.28

- Old Base case PT (5-yr): $356.80, New Base case PT (5-yr): $329.19

Despite a significant cut in both fair value and 5-yr price target, Amazon remains undervalued at ~$100.

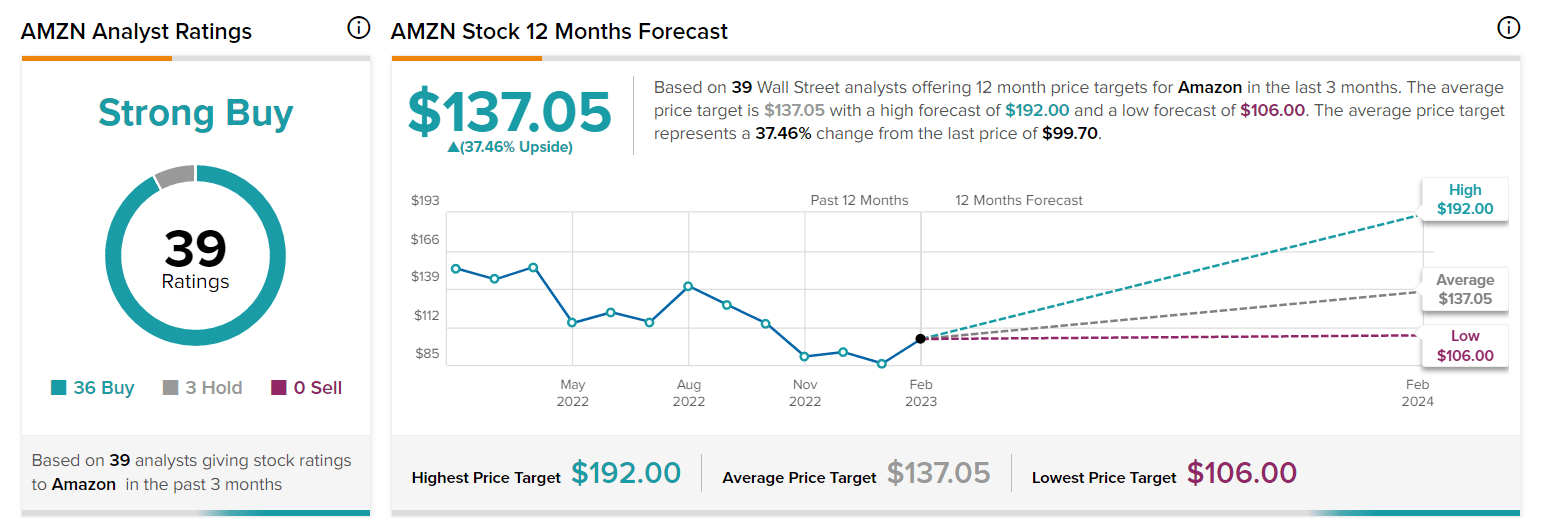

What Are Analyst Price Targets?

According to TipRanks, Amazon currently boasts 36 Buy, 3 Hold, and 0 Sell ratings from Wall Street analysts! The average 12-month price target for Amazon is $137, which if met would result in a cool gain of ~37%.

TipRanks

Even the lowest 12-month price objective on AMZN stock is $106, which is a +6% upside from current levels. Clearly, Wall Street analysts are in agreement with our bullish stance on Amazon.

Bottom Line: Is Amazon Stock A Buying Opportunity Around $100?

Amazon.com’s moat in e-commerce is virtually impregnable, and its cloud business [AWS] is still recording the highest revenue increases among cloud infrastructure providers based on absolute dollar figures. Overall, Amazon’s Q4 report was decent, and despite a macro-inflicted slowdown in AWS and Ads, I think staying the course with Amazon is the right way to go.

After getting rejected from the upper trendline of the falling downward channel (marked in dotted red), AMZN looks nailed on to re-test its recent lows in the low to mid $80s.

WeBull Desktop

Here’s what I said about Amazon in one of my recent notes –

As pointed out in my previous note, Amazon’s stock held multi-year support at $80 and bounced off this level. After a sharp 16%+ YTD bounce, Amazon looks primed to re-test the $100-$105 range in the coming weeks. If the stock fails to break this level, I would expect it to remain rangebound in the $80-$100 range.

And for now, I stick to this call for Amazon to remain rangebound in the $80-$100 range. If Amazon were to break down the multi-year support in the low $80s, then we could see the stock slide down to the next big support zone on the chart, which is in the $50s. Now, I do not expect Amazon to go this low until and unless we have a deep, deep recession!

At current levels of ~$100, I view Amazon as a solid buy. However, the technical setup is not great, and business profitability remains a concern amid slowing revenue growth. Hence, I like the idea of staggered accumulation of AMZN shares through a 6-12 month DCA plan.

Key Takeaway: I rate Amazon a “Strong Buy” at $100, with a strong preference for staggered accumulation.

As always, thank you for reading, and happy investing. Please feel free to share any questions, concerns, or thoughts in the comments section below.

Disclosure: I/we have a beneficial long position in the shares of AMZN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

At The Quantamental Investor, we make investing simple, fun, and profitable together. To learn more about our investor community –> Click Here