Summary:

- Agilysys is a leading software company that provides technology solutions for the hospitality industry.

- The hospitality services giant has a strong YoY subscription growth rate of 28% and YoY revenue growth rate of 25.79%.

- The average intrinsic share value of $46.15 suggests the stock is highly overvalued compared to current price of ~$82.86.

- I rate this a hold based on valuations and marginal free cash flows.

I going to make a greatest artwork as I can, by my head, my hand and by my mind.

Agilysys (NASDAQ:AGYS) has been serving the hospitality industry via its software, helping to manage complex businesses in an industry that includes hotels, resorts, cruises, and corporate food service management for the past 40 years. Headquartered in Alpharetta, Ga., Agilysys operates in five other countries across several regions, including Europe, the Middle East, Africa, Asia-Pacific, and India.

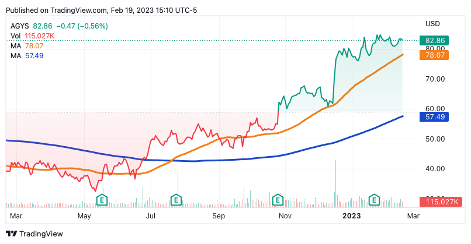

Agilysys operates in a $4.8 billion opportunity market with a subscription YoY growth rate of 28% as of March 31, 2021. Capitalizing on this industry with a strong presence worldwide, the company’s stock doubled last year, rallying from $39.77 on Feb. 17, 2022, to $83.90 as of Feb. 17, 2023. The tech company signed a deal with Marriott International (MAR) two months earlier to deliver its cloud-native property management system (PMS) software across its luxury, premium, and select service properties in the U.S. and Canada.

Revenue growth YoY has been staggering at 25.79%, which beats the sector median of 16.08%. Free cash flow per share growth rate is 3%, which is 67.8% lower than the sector median of 9.32%. Growing revenue, a rising stock price, and increased customer engagement all provide a strong basis for the company’s growth. However, lower free cash flow growth creates a point of concern for investors at the same time, making it a hold.

Financial Performance

Agilysys has a strong position in cash and cash equivalents (CCE) with $96 million in FY 2022, 2.2% less than the previous year’s value. The CCE component in FY 2021 was $99.1 million, a steep increase of 112% from the previous year’s value. A higher cash position means higher liquidity and lower interest rates for AGYS, which makes it less risky as an investment. Although a higher CCE might be good, levered free cash flow (LFCF) of $20.72 million is quite low as compared to its peers like E2open Parent Holdings (ETWO), Zeta Global Holdings Corp. (ZETA), and Q2 Holdings (QTWO), which have LFCF of $64.25 million, $147.32 million, and $62.47 million, respectively. A higher LFCF usually denotes a company’s ability to finance its investment activities through debt and generate returns, rather than burning its cash reserves.

The price/cash flow ratio of AGYS is 84.25, which beats the sector median of 20.29 by 315.2%. A high-value P/CF ratio suggests the company is highly overvalued with respect to its cash flows.

Marriott Agreement, Strong Market Rally

Agilysys is a 50-year-old tech company with a strong industry reputation and global presence. The company reported revenue of $137.1 million for FY 2021, 16% less than that of FY 2020, mainly due to the impact of COVID-19 on the hospitality sector. It grew 15.4% to $162 million in 2022 and has a current trailing 12 months (TTM) revenue of $191.7 million.

Revenue and earnings might have taken a hit in a stressed market during the pandemic, but investors and analysts trusted the stock to grow in the future, making its stock price rally 300% over the last three years from a low of $25.5 to $82.86. Apart from staggering stock growth, the TTM P/E multiple for AGYS is 202.42, which is also 3x that of the sector median. A strong TTM P/E multiple and market rallies over time suggest that investors believe in the company’s growth dynamics and strategy to capture the hospitality market.

AGYS Stock Price (TradingView)

A big positive for AGYS came in 2022 when the PMS provider announced its agreement with Marriott to provide tech solutions for managing the hospitality giant’s properties across the U.S. and Canada. On the day of the announcement, the stock rose from $62 to $77, marking one of the biggest single-day gains. Apart from this deal, the tech firm has a diversified base of software solutions to meet the needs of a more varied base of customers around the globe, not limiting itself to just resorts but also serving cruises, hotels, and other such hospitality facilities.

Weakness

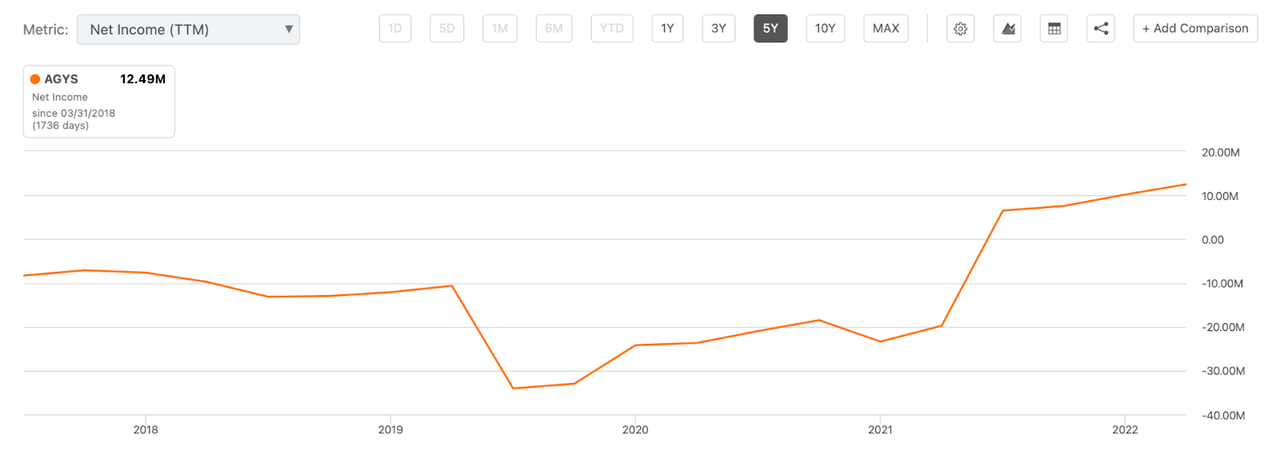

AGYS has been loss-making for the past five years and has only recently reported a positive net income of $12.49 million. A major reason for the loss during 2020-22 is the impact of the COVID-19 pandemic on the hospitality industry, the focus area for the company’s software. This also affected its gross profit margin, which was down 7% to 49% in FY 2021 from a high of 56% in FY2020.

Net Income ((TTM)) Past 5 years (Seeking Alpha)

Valuation

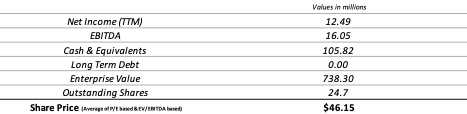

The intrinsic value of the stock is $58.13, according to a P/E multiple stock valuation method, and $34.17 as per an EV/EBITDA multiple valuation method. It averages out to be $46.15, 44.3% less than what the stock trades at right now. I considered a P/E multiple of 114.96x (average of a peer) and an EV/EBITDA multiple of 46x (average of a peer) when carrying out these valuations.

Share Price Intrinsic Value (Author)

Negative net income growth, comparatively lower levered free cash flow, and high P/E and EV/EBITDA multiples have led to a lower intrinsic stock value for AGYS.

Conclusion

AGYS is on my radar, notwithstanding my reservations about its net income and levered free cash flows, for several reasons. Among these are improvements in top-line revenue performance, outstanding profit margins, excellent online sales in the U.S. and other markets, and increased sales in the U.S. The P/E ratio, EV/EBITDA multiples, and profit margins for AGYS are rather alluring. Despite this, I rate the company a hold due to the risk of declining FCFs and net income.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.